When Chinese president Xi Jinping attended the annual Apec meeting of Asia-Pacific nations in 2013, held that year in Bali, he surprised delegates by proposing to build a new multilateral development bank.

There had been no true new regional international financial institution since the European Bank for Reconstruction and Development was unveiled in 1991 to instil free markets in former Soviet bloc states.

Many observers questioned the need for another development bank and openly wondered what role this new institution would play.

Nearly five years on from its incorporation, the Covid-19 crisis is giving the Asian Infrastructure Investment Bank a chance to prove its place in the world.

“This is a litmus test of our ability to deal with a crisis and emergency,” AIIB’s president, Jin Liqun, tells Euromoney via video-link from his office in Beijing. “This is the time for us to demonstrate our adaptability, resilience, responsiveness and readiness.”

What does this mean? In the short term, the AIIB said on April 17, it will double the size of its Covid-19 Crisis Recovery Facility, set up to help member states battling the pandemic, to $10 billion.

It will focus on providing budgetary support and improving health infrastructure.

We will be, in the not too distant future, a bank doing $20 billion in lending each year - Jin Liqun, AIIB

So far, it has pledged $500 million, co-financed with the World Bank, to purchase medical equipment in India; a $500 million credit line to two Turkish development banks to tackle capital shortages; and $250 million to Indonesia to speed up testing and make hospitals pandemic-ready.

Coronavirus is a complex problem for development banks as well as epidemiologists. The AIIB is busy stress testing to figure out how to lend to troubled member states while keeping enough cash on its books.

“We will be affected in our liquidity portfolio with US dollar interest rates having dropped to zero,” says Martin Kimmig, the AIIB’s head of risk. He adds that a “worsening of credit conditions both of sovereigns as well as private-sector companies will increase impairment charges on our credit portfolio.”

He believes the flow of capital into new projects will slow as clients “reprioritize funds to support ongoing activities”.

He says that human resources and travel constraints might mean “working with other multilaterals with reach and boots on the ground” – again highlighting how hard it is to work in markets without a field presence.

Showing its worth

In a sense Covid-19 happened at a good time for the AIIB. While it is busy channelling aid to member states, its youth and lean structure means it isn’t yet seen as a frontline multilateral. It can use the crisis period to learn key lessons about, for example, the state of health infrastructure in the region.

Is this the moment that the AIIB begins to show its worth?

Jin says the grand idea of China's president was to "create a multilateral development bank focused on infrastructure and connectivity”.

There is a lot in those words and they are worth examining.

China’s first interaction with a Bretton Woods institution was in April 1980, when then-president of the World Bank Bob McNamara met Chinese premier Deng Xiaoping in Beijing.

AIIB’s president Jin Liqun

Jin, a member of the finance ministry, was an onlooker that day. A few months later, he was posted to work at the World Bank in Washington, rising through the ranks to serve on its board and, later, as vice-president of the Asian Development Bank (ADB).

China meanwhile began its meteoric ascent. When McNamara and Deng met in Beijing, the country’s GDP “was a paltry $280 billion and we had no basic infrastructure to speak of,” says Jin. But by the early 2000s it was the coming power in Asia and was a net contributor to the World Bank and the IMF.

Higher national income begged a question, Jin says. Should the country “just sit there waiting for MDBs to help us” or could it contribute – and if so, how? After the global financial crisis, China started to ask itself how to interact with developing countries.

The first inkling that a new MDB was on its way came in 2009 at the Boao forum, a talking shop modelled on Davos and located on the southern island of Hainan.

Policymakers keen to make better use of China’s vast foreign currency reserves worked on the concept of a new multilateral behind the scenes.

But it wasn’t until Xi’s speech in Bali that wheels began to turn. In January 2014, Jin got the nod.

“I very quickly relinquished responsibility as president of CICC [China International Capital Corp, a leading investment bank] and devoted myself fully to this project,” he says.

We aim to be seen as a predictable borrower for investors – I would like to be in the [US dollar] benchmark market twice a year, completing chunky transactions - Martine Mills Hagen, AIIB

The idea of building a new pure-play development bank to serve Asia’s needs was soon swatted aside. Jin says a question that sprang constantly to mind was whether or not anyone really needed another cookie-cutter multilateral. Wasn’t it more cost-effective to put money to work in existing institutions rather than building a new one?

China had tried that approach. After the global financial crisis, it lobbied furiously to invest more in and secure greater control of the IMF and World Bank. The US, which has the highest voting share of both institutions followed by Japan, pushed back hard. So in a quieter way did Europe, which prizes its historical sway in the IMF and its ability to nominate each new managing director.

Beijing viewed that rebuff as a stinging loss of face. Its pain was amplified by the fact that China felt genuine gratitude to the help offered by both Bretton Woods bodies at a time when it was on its knees.

Jin says the importance of the MDB system has “never been so deeply appreciated” as it was by China in those dark days.

So it was that in January 2016, the freshly minted Asian Infrastructure Investment Bank opened for business. It marked the culmination of two years of frantic travel on Jin’s part. The AIIB’s newsfeed from that period shows him meeting Indian prime minister Narendra Modi, UK PM David Cameron, Indonesian president Joko Widodo and countless other political leaders.

But it worked, in large part because Jin was able to assuage fears that the bank would simply be a tool of Chinese foreign policy.

“When we were set up, a lot of people doubted whether the bank could work,” he says. “I spent a lot of time with chief negotiators, telling them... that China would be the largest shareholder but would not dominate it. And that the president and vice-presidents should be elected on a meritocratic basis by all member countries.”

Martin Kimmig, the AIIB’s head of risk

New Zealand was the first nation to enter into talks, followed by Korea, Singapore and Australia. When Britain signed up, then France and Germany, the AIIB could relax a little.

By the time it opened for business, it had 57 members including India – not a country that usually sees eye to eye with its neighbour. The US, which refused to engage in talks from the start, remains outside the tent looking in, as does Japan.

The new Beijing-based multilateral had plenty of money from the start, with $100 billion in capital, 20% paid in and 80% callable. China, which controls 26.06% of the voting shares, contributed exactly half that amount, while India, the second-largest shareholder with 7.01% of the bank’s voting rights, stumping up $8.4 billion.

Now the question shifted to what kind of institution it should seek to be. Nearly five years after the AIIB was formed (its articles of agreement were signed into force on Christmas Day 2015), this issue remains an important but shifting one.

It is almost easier to describe what the AIIB is not rather than what it actually is.

Multilateral

Let’s start with the obvious question. Given that the word ‘development’ does not appear in its name but ‘investment’ and ‘infrastructure’ do, is it a real multilateral?

“We are all three,” replies Joachim von Amsberg, vice-president in charge of policy and strategy. “We are a development bank as we have a development mandate. We are an infrastructure bank as we finance infrastructure; and we are an investment bank as we mobilize investment.”

For his part, Jin fudges his answer a little, as you might expect from a world-class politician and policymaker.

On the one hand, he describes the AIIB as a “21st century development bank”. On the other, he says it was clear from the start that the greatest need across the developing world “was in the field of infrastructure.”

He adds: “The idea was to create a bank that would help Asian countries but also boost global connectivity and trade.”

A senior official at another regional MDB frames the bank’s identity well.

“It was set up as a multilateral for infrastructure financing,” he says. “It is not a development bank in the strict sense of the word.”

We are entering a 10-year growth phase, at the end of which we will be lending $15 billion a year - Joachim von Amsberg, AIIB

From the start, the bank was keen to learn from its peers, building on the classic model that has served the development community well since 1944, and to blaze its own trail.

In its early days, AIIB officials visited the EBRD in London to glean insights about governance, take part in workshops and see how it was structured. The first project it committed to in June 2016, a $27.5 million road improvement loan in Tajikistan, was led by the European multilateral, with the AIIB, then still developing its risk function, acting as an observer and co-financer.

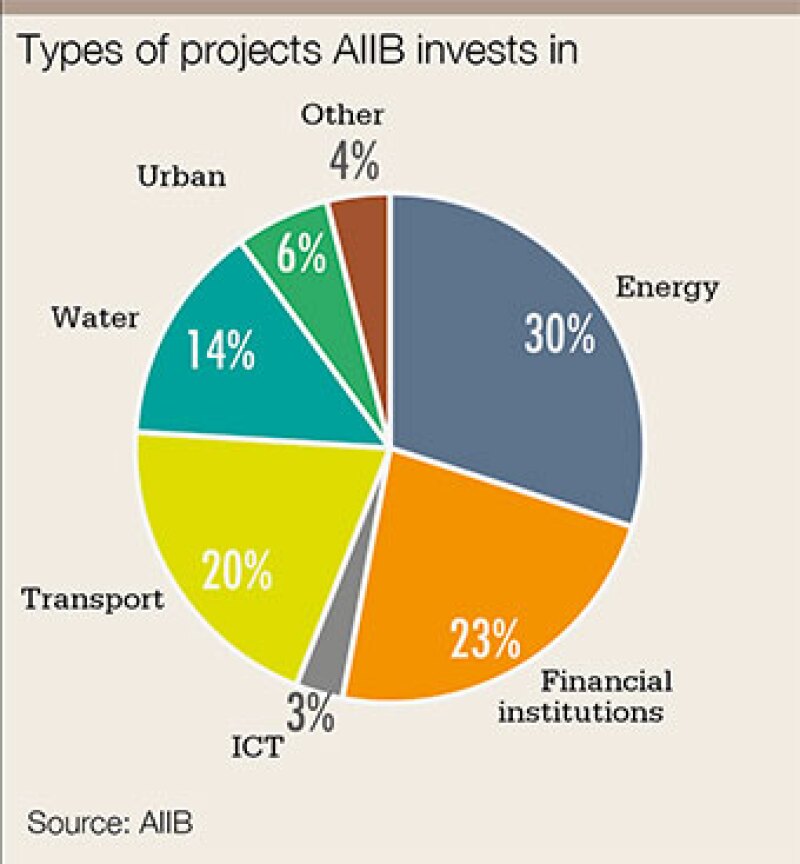

As of April 17, 2020, it had approved 70 projects with a total value of $13.8 billion, with 43 more in the pipeline or under consideration, and together valued at $24.9 billion.

It also learned at the feet of Asia’s other multilateral. Jin knows the Asian Development Bank from his time in Manila; in the AIIB’s early days, he hired it to carry out a $400,000 technical assistance report, which included $120,000 worth of seminars and training sessions.

Casting around for talent in its early days, the AIIB turned to the best and obvious sources. In came von Amsberg and chief risk officer Kimmig, both World Bank veterans, and later on, chief financial officer Andrew Cross, a former deputy treasurer at the IFC.

Danny Alexander, vice-president and corporate secretary, AIIB

Danny Alexander, a former chief secretary to the UK treasury, speaks to shareholders, mediates with the boards of directors and governors, and oversees the admission of new member states.

Jin says the aim was to learn lessons from others, but not to emulate their actions wholesale: “We learned from international institutions with 70-plus years of operating ability, but from the start we set out to be a new type of institution that learned from others while innovating and creating our own products and services.”

And by ‘new’, he means it. The AIIB’s board meets not in person but virtually, keeping in touch over WeChat, Zoom and Microsoft Teams – particularly useful at a time when coronavirus has put so many countries on lockdown.

While the EBRD has 23 directors based in London, all of whom physically attend fortnightly board meetings, the AIIB has 12, none of whom need to travel to offer their input.

“We have minimized – at least so far – bureaucracy and redundancy, thereby controlling the overhead cost of the bank,” says Jin.

He describes the operating structure as “flat, lean and agile”, adding that a desire to be sustainable from the outset makes it an institution geared to being “lean, clean and green.” The three-pronged aim is: no needless bureaucracy; zero tolerance to corruption; and a refusal to allow projects to harm the environment.

That focus hasn’t gone unnoticed elsewhere.

“To give them credit, their rules make them a bit more efficient than us,” says a senior official at a rival MDB. “They have hired well and grown in a smart way. We can be slow in processing matters due to the governance requirements we face in each country.

“When they make a decision, they move fast. That’s a clear difference between them and other IFIs.”

Jin says the aim is to be “more productive” – squeezing extra output from less input. Von

[The AIIB is] not equipped to bring the private sector in. They have their own dynamics, their own objectives. They are different from multilaterals with public facing initiatives - Development expert

Amsberg wants the bank to stay lean, with headcount rising from 300 now to 1,000 by the end of the 2020s. Compare that with the EBRD or ADB, both of whom employee 3,000 people, and the World Bank, with its headcount of 10,000.

Jin is painfully aware of the danger of becoming “filled with redundant staff and positions” as the AIIB grows.

“This is a commonplace problem of lots of institutions after years of development,” he says. “A challenge is how to prepare the budget each year; how to control the urge to expand your staff in every department.”

The bank reckons it can be done. Von Amsberg points to the amount of work it can outsource to consultancies, think tanks or engineering firms – “incredibly smart partners dotted around the world who weren’t there 60 or 70 years ago when the World Bank was formed”.

There is, he says, “a huge ecosystem of development players with incredible capacity. Rather than building a huge in-house research team, others can do it for us.”

The AIIB’s research team is made up of just “six or seven people,” says von Amsberg – most of whom spend their day unearthing useful reports and directing them to the right department head.

The World Bank, as of February 2020, had 66 full-time economists, specializing in everything from poverty to trade to human development, not to mention hundreds of researchers and analysts.

Great flaw

From the outset, the AIIB spotted the great flaw in the multilateral model. When MDBs shifted their focus in the 1980s toward poverty reduction, social programmes, education and health initiatives, it made sense. The world benefits when people are better educated, wealthier and healthier.

But when more is spent on such initiatives, there is by definition “little money left to spend on infrastructure investment,” says Jin.

And if there is one thing that all countries complain about, it is being unable to tap enough sources of capital to pay for new roads, hospitals, airports and schools.

An April 2019 report by the ADB put the deficit in infrastructure investment, just in southeast Asia, at $2.8 trillion in the 15 years to 2030. This is what the AIIB saw from day one: the chance to channel much-needed capital into infrastructure projects across Asia.

But while lean can be good, there’s a limit to what you can do with no fat on your bones. The EBRD has 39 offices in member countries, the ADB 21 and it’s hard to name a sovereign state where the World Bank is not physically represented.

Martine Mills Hagen, the AIIB’s head of funding

The AIIB by contrast operates from one physical location – its headquarters in Beijing. It has some additional office space in Hong Kong, used by Martine Mills Hagen, the AIIB’s head of funding, when meeting investors and it was called into action during the coronavirus crisis, when travel to the Chinese capital necessitated on arrival a 14-day period in quarantine in a state-mandated hotel.

So far, much of the important legwork and glad-handing has been done personally by Jin and von Amsberg. But in the long term having no one on the ground bar in two Chinese cities, in a region that accounts for 60% of the world’s population and 50% of global economic output, will take some justifying.

“We do not have boots on the ground,” says Jin. “That is a fact.”

The challenge is to find new ways to keep in touch with clients and counterparts on the ground. Technology can help of course, but it may not be possible to maintain a threadbare operation for long.

“I’m already being pushed to set up field offices in various place,” he admits. “People ask me all the time – when I am going to set up a field office here or there? My answer is that I need to do research before I decide to have a local presence or indeed what kind of presence it should be. It’s very easy to duplicate the patterns of other [MDBs], but we need to consider if we can use digital measures to set up virtual field offices.

“In due course, we may set up some form of local presence,” he adds, noting that it will only happen if he is convinced the benefits outweigh the costs.

A possible trade-off is to open a handful of offices that serve a whole region: south Asia (the focal point of most of the bank’s projects to-date) out of New Delhi, say, or central Asia from Tashkent or Nur-Sultan.

“Sooner or later, this is a question they’ll need to face,” says one senior individual at a regional MDB. “If they decide they need a bunch of new offices, that will change their business model. It means higher costs, more oversight and regulation, and suddenly they look much more like a classic development bank.”

Joachim von Amsberg, AIIB's vice-president in charge of policy and strategy

This is no small consideration – it’s a challenge that will define the AIIB as it grows. When asked how involved the bank is on its projects, von Amsberg replies: “We finance or co-finance projects. There is always someone else actually doing the project, either a private company or a government. The sponsor comes to us with the project, and our job is to decide if we are willing to invest in it.”

But nothing is ever that simple in development finance, which is why the multilateral model is so difficult to copy.

“We often have to get involved in procurement and supervise projects to ensure they are following environmental guidelines,” says a senior development official not at the AIIB.

“On every project, we ask: ‘Why do this project and not that one?’” he adds. “You have to ensure a high level of developmental impact, and that can mean seeking riskier projects and working with agencies who can offer that additional capacity. With [the AIIB’s] current model, with no field presence, with no one who speaks the local language, I’m not sure if they can do that.”

Jin knows that trust and name-recognition cannot be built in just five years. But he’s also painfully aware that the more money he spends on office space or hiring staff, means there is less available to build roads and hospitals.

A broader and taller operation is also more bureaucratic.

“It’s very hard to decentralize while keeping decision-making centralized, just as it is very difficult to avoid duplication in decision-making processes,” notes Jin.

Where Asia’s new IFI can be a trailblazer, creating a brand and guaranteeing the support and gratitude of the MDB community is by finding novel ways to corral private-sector capital and channel it into infrastructure.

“A big project financed by a bunch of multilaterals doesn’t help with the financing gap,” says a senior US development official. “The total size of the pie isn’t that big. Multilaterals aren’t that big. What we need is to put huge pools of private-sector money to work in big projects we all work on. That’s where [the AIIB] can come in.”

Can they meet that need? Some have doubts.

“They have to find a way to identify suitable projects – and that isn’t easy,” says one development expert.

“[The AIIB is] not equipped to bring the private sector in,” adds another. “They are a bit unsophisticated for that. They have their own dynamics, their own objectives. They are different from multilaterals with public facing initiatives.”

Investment

As the new kid on the block, some disdain is inevitable. But it’s also clear that the new bank isn’t just talk.

In November 2019, it launched Bayfront Infrastructure Management (BIM), a new $2 billion debt financing platform that will buy brownfield project and infrastructure loans from financial institutions, then sell them to investors on the open market as securitized notes.

The aim is to help commercial lenders to free up capital and to create a new market in secondary infrastructure.

AIIB will invest $54 million for a 30% stake in BIM, with Clifford Capital, a project and finance specialist backed by Singapore’s government, paying $126 million for the remaining 70%. The rest of the collateral will be raised from private-sector investors.

In April 2020, with the West still in lockdown, the AIIB committed $100 million, plus a co-investment sleeve of up to $50 million, to the Keppel Asia Infrastructure Fund, a closed-end private equity fund backed by Singapore-listed Keppel Corporation.

The fund, which has a target size of $1 billion, will invest in pan-Asian infrastructure assets across telecommunications, transport and logistics, and clean energy.

Late in the second quarter, it will move from its current offices in Beijing’s Financial Street to new headquarters in the city’s central Olympic Park. Insiders said coronavirus will not delay the opening of the solar-powered building by president Xi.

In May 2019, the bank priced its inaugural bond, a five-year, $2.5 billion print priced in line with the likes of the World Bank and the European Investment Bank. Head of funding Mills Hagen says the bank aims to borrow “in the region of $10 billion a year” from the mid 2020s.

She says the AIIB hopes to “come back to the US dollar market as soon as possible” and adds: “We aim to be seen as a predictable borrower for investors – I would like to be in the [US dollar] benchmark market twice a year, completing chunky transactions.”

Also on the horizon are the sale of kangaroo and panda bonds, priced respectively in Australian dollars and Chinese renminbi.

Asked if the bank aims to issue green bonds, Mills Hagen replies: “Our belief is there isn’t a need to, as our projects all have to meet our strict environmental and social criteria – and besides, we view all of our projects as sustainable.”

She adds: “We will also look at issuing more thematic bonds – water bonds perhaps, and so on.”

This is also a political year for the AIIB. In September 2020, Jin marks his fifth anniversary as head of the bank (he spent the first four months in office as president ‘designate’). He is allowed to run for one more five-year term in office, and while he is coy about the future, noting only that he is “very much open to what will happen,” he smiles as he speaks. Most people expect him to run unopposed.

“I was dedicated to the bank from the very beginning,” he says. “I love it.”

Beyond that, the future isn’t written. The bank may continue to stick to its original course. Its president wants the AIIB to be financially sustainable, a key proponent in social development and a leading international financial institution.

“We will be, in the not too distant future, a bank doing $20 billion in lending each year,” Jin says.

Von Amsberg adds: “We have done well, but we are modest in scale, so our plan is to expand. We are entering a 10-year growth phase, at the end of which we will be lending $15 billion a year.”

The key will be to use its contacts and balance sheet to crowd more private capital into infrastructure projects, in Asia and around the world.

“Anyone can be a member of this bank so long as they are members of the World Bank and the IMF,” says the AIIB’s first president. “We can serve African, Latin American and Australasian countries, based on balance and need. From the start, this bank was positioned as an Asian infrastructure investment bank. Our work is not confined to Asia.”