Illustration: Doug John Miller

|

IN FOCUS |

|

|

|

It looks, from one perspective, like another desperate measure to distract attention from their inability to make money from their core businesses.

European banks are finally waking up to the need to pay more attention to their asset management arms. Many have already sold out or have rapidly lost the market share they enjoyed there before the 2008 crisis.

Now, as persistently low rates in Europe have pushed down interest margins and pushed up asset values, the rare value some banks enjoy in these businesses is ever-harder to ignore. Asset management has become the best-performing part – a crown jewel of their equity story – at big banks, such as Crédit Agricole, Intesa Sanpaolo and Nordea, that are struggling in other parts of their business.

Indeed, France’s Natixis has begun to see itself not as a bank that owns an asset manager but almost as an asset manager that owns a bank.

Deutsche Bank’s asset manager – recently partly listed and rebranded DWS – is one of the few areas in which Germany’s biggest bank enjoys a dominant market share at home.

You need to be small and nimble or very large and global – Campbell Fleming, Aberdeen Standard Investments

But it faces challenges in asset management both there and abroad, as the removal of its former chief executive Nicolas Moreau after third quarter results shows. In Germany, this is one of the few sectors in which the sprawling savings and mutual bank groups are effectively harnessing their strengths, through DekaBank and Union Investment, respectively. These two have roughly doubled fund volumes since 2010, to around €300 billion each.

Thanks to listings of the cooperative central organs in the previous decade, the French equivalents to Union and Deka – Amundi and Natixis – have had the greatest appetite for international acquisitions.

Above all, Amundi has changed almost beyond recognition from the asset manager of the Crédit Agricole mutual network from which it grew 10 years ago. It is the world’s biggest asset manager outside the US, largely thanks to a joint venture with Société Générale in 2009 and the purchase of UniCredit’s Pioneer, along with a valuable long-term distribution agreement covering Italy and Germany.

Amundi makes a compelling model, as other bank-owned asset managers in Europe seek to grow, diversify and improve their efficiency. Who will follow?

Chop

Asset management was one of the first areas to get the chop as European banks raised capital and sold non-core businesses after the 2008 crisis. Barclays sold its asset manager, including its exchange-traded funds platform, to BlackRock. Royal Bank of Scotland sold to Aberdeen. Credit Suisse also sold its traditional asset management business outside Switzerland and Brazil, also to Aberdeen, while Dutch mutual group Rabobank sold a 90% stake in Robeco to Japan’s Orix in 2013. Finally, SocGen completed its long-planned exit via Amundi’s 2015 IPO.

Ten years after the crisis, banks are seeking to renew their links to asset management clients and, like Crédit Agricole with Pioneer, they are looking more closely at whether M&A could boost their distribution or product capability.

Natixis was shortlisted for the Pioneer deal, for example, after an early-2000s US acquisition gave it a relatively large stature in asset management. Today, once again, it is open to transformational deals, especially with European bank distribution agreements – if it retains control – the unit’s chief executive Jean Raby tells Euromoney.

The partial IPO this year of DWS, Europe’s fourth-biggest bank-owned asset manager, is designed to give it cash to make acquisitions. And, again, Deutsche’s board intends to retain a majority, said Moreau when he spoke to this magazine before his removal.

|

|

Despite previous rumours that they might sell out, even firms such as HSBC and UBS tell Euromoney their restructured and recently closer-integrated asset management divisions have new potential to catch up with rivals.

UBS, the world’s biggest fund manager before the 2008 crisis, stagnated during the early 2010s even as others grew rapidly with the equity market, but it could now participate in asset management M&A, according to division president Ulrich Körner.

“Two or three years ago, UBS Asset Management was not in a position to participate in any shape or form of an external growth effort,” says Körner. “With the transformation complete, we are in a position to potentially play a role in the consolidation we expect to see in the European asset management industry.”

Meanwhile, if HSBC viewed asset management as dispensable, it might have sold out already, given its raft of other divestments in Latin America and elsewhere this decade, and given asset management’s relatively high valuation.

“We are seeing asset management as a very significant growth potential that we have,” comments Sridhar Chandrasekharan, chief executive of HSBC Global Asset Management.

Santander bought back the 50% of the asset management arm it had previously sold to Generali Atlantic and Warburg Pincus, in late 2016. It now plans double-digit growth for a newly combined wealth and asset management unit.

“In a low-rates world, clients see asset management as a core part of the relationship with their bank,” says the unit’s head, Victor Matarranz.

Regulation

More than anything else, regulation – especially capital requirements for loans and trading – has heightened banks’ enthusiasm for asset management. Even at a relatively inefficient firm like UBS, for example, its asset management return on equity is still in the mid-20% range. It also offers firms such as Deutsche a way to show to investors and regulators a less volatile income stream than markets and investment banking. This is a priority for Deutsche chief executive Christian Sewing.

Even today, European banks, especially on the continent, have a crucial advantage in asset management in their home markets, as they remain bigger fund distributors to retail and private clients than in the US.

But this is not just about regulatory headwinds and the cyclical swelling of asset values. Most compellingly, asset management is a way for banks to tap rising private wealth in Asia and other emerging markets. They have a better chance of competing there than on the US asset managers’ home turf.

Although their ability to enter mainland China is limited, even smaller European asset managers such as Intesa Sanpaolo’s Eurizon have set up Chinese joint ventures with around $100 billion or more under management. Now China is handing out licences for wholly owned asset managers.

“We must not miss this opportunity,” says UBS’s Körner.

Investing in asset management is not, however, a one-way bet. Low ECB rates make higher fees a sore point, particularly given European clients’ typically large fixed income allocations. Fee and revenue growth lag the growth in assets under management.

Even if markets stay buoyant, the rise of cheap passive products could spur a decline in fees of about 12% over the next three years if nothing is done about it, Deutsche research estimates. On the other hand, with US interest rates rising, asset values are under pressure.

|

|

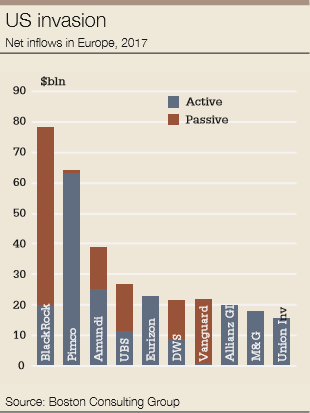

Over the last decade, independent US fund managers’ growth in assets under management has been much more rapid than those in Europe. Even in the European market, BlackRock and Pimco enjoyed the biggest net inflows in 2017, according to Boston Consulting Group. Indeed, BlackRock’s share of inflows was higher in Europe than in the US.

Posting high ROE in asset management is therefore comforting for banks’ overall returns, but this might not be sufficient for their investors.

“Banks need to demonstrate to their investors that they are the owners most capable of making a marginal gain on these businesses’ profitability over the longer term,” says BCG financial institutions principal Dean Frankle.

Compared with the independents, the larger bank and insurance-owned asset managers have seen their expenses rise more in line with their revenue growth over the last five years, according to Kinner Lakhani, head of European financials research at Deutsche. This could soon become more apparent, he says, given fixed costs and because the market underestimates asset management’s cyclicality.

“Bank-owned asset managers generate good returns, but have not generated operating leverage through the benign markets of recent years,” he says.

|

|

|

Kinner Lakhani, |

He puts the US bank-owned players in this group too.

Although they also benefit from distribution fees, critics say some captive managers remain afloat merely because the bank will still offer individuals in-house products, even if their fund managers underperform.

On the retail side, passive funds from the likes of BlackRock have grown much less rapidly in Europe than the US.

Europe’s retail market could be next in line for the growth of passives and the accompanying fee pressures as secular changes in the industry make it harder to exploit in-built distribution networks.

Some smaller bank-owned asset managers, such as Santander, have changed to an open-architecture model in retail in recent years.

“We don’t believe in imposing a product on the customers anymore,” says Matarranz. “When we provide products the customers don’t want, we see that.”

However, captive clients might no longer use their relationship bank’s asset manager, no matter how much they like the brand, if an exchange-traded fund from another firm – perhaps offering the same return at a lower price – is more readily available.

This is a trend that could accelerate after the introduction this year of the EU’s updated Markets in Financial Instruments Directive (Mifid II) and the Packaged Retail and Insurance-based Investment Products (Priips) regulation. The new rules force asset managers to do more to communicate their funds’ risks, performance and fees – with potentially the greatest impact on captive asset managers selling basic products at a premium.

“Banks need to think about what they do next in asset management,” says Giorgio Cocini, Bank of America Merrill Lynch’s co-head of financial institutions in Europe. “There may be increased scrutiny by regulators of the quality of funds sold to their retail customers. Customers themselves will become more sophisticated and there will be pricing pressures.”

Scale

As banks turn back to asset management for growth, scale is becoming more important than ever. Technology, just as in other areas of banking, is making it easier to shop around and is empowering new non-bank distributors. US independent passive house Vanguard launched a direct-to-consumer platform in the UK last year, for example.

The need for bigger IT investments and the requirement to pay for things such as research under Europe’s Mifid II rules could place a relatively greater burden on smaller asset managers. This might be particularly true if the business’s core advantage is its brand recognition. A bank’s captive network, in other words, might not be big enough to justify the costs of running an asset manager that can be competitive in future.

Globally, BlackRock is an outlier by size – almost twice as large by assets under management as the next biggest, at around $6 trillion. Amundi is a European equivalent. Both firms’ snowballing growth has meant that what constitutes sufficient scale in the industry has risen.

Independent and diversified asset managers need scale, to have the right teams, processes and IT. We are a different animal, as being part of a group can be a differentiator – Victor Matarranz, Santander

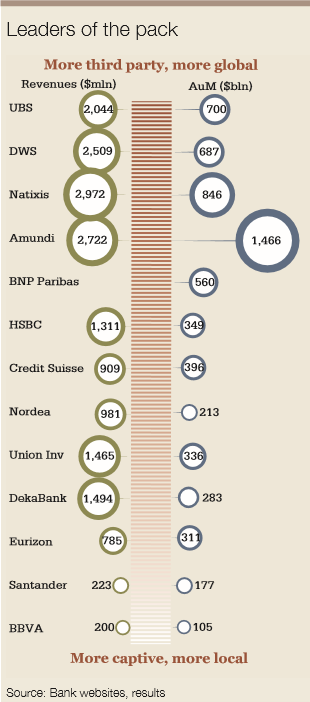

Amundi was first to reach the $1 trillion mark among the bank-owned firms in Europe. It is Europe’s only top-10 asset manager worldwide by assets, roughly equal to JPMorgan Asset Management, which is the world’s fifth biggest.

Amundi has the third biggest net flows in Europe and has a much higher proportion of inflows from active funds than BlackRock, according to BCG.

Chief executive Yves Perrier says Pioneer will allow Amundi even greater economies of scale, not just in doing away with the need for duplicate management of similar investment strategies, but also as it in-sources Pioneer’s IT systems from BlackRock.

“If we increase our volumes, it doesn’t mean that we increase the cost of IT proportionally,” he says.

However, not all the bank-owned asset managers agree with the often-repeated rule that, given the limited shelf space of the big distributors, those with less than $1 trillion will struggle.

“If you’re a passive manager, I’m not sure that even $1 trillion is good enough,” says Nordea’s asset management head Nils Bolmstrand. “It’s a question of products, the outlook for those products and what alpha you can generate.”

As in investment banking, the common view in asset management is that firms that try to do everything will struggle if they are not among the biggest players.

|

|

|

Campbell Fleming, |

“You need to be small and nimble or very large and global,” says Campbell Fleming, head of distribution at Aberdeen Standard Investments in London, the £560 billion product of a merger last year.

One problem is what ‘large’ means in this context. Even firms with around €300 billion under management – such as the Spanish, Scandinavians and Intesa Sanpaolo’s Eurizon – might be considered niche players, as most have a majority of in-house and domestic clients.

By contrast, the profit margins of European bank-owned asset managers with between €500 billion and €1 trillion are more challenged. They might now occupy the squeezed middle. BNP Paribas, DWS and UBS are firmly in this size bracket. HSBC is closest to the bottom end. Natixis, with €846 billion, has the best chance of breaking out of the top end and is aiming for €1 trillion by 2020.

|

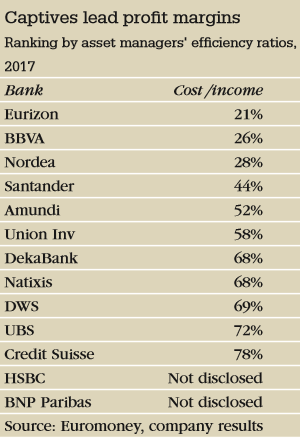

All these middling firms, including Natixis, have cost-to-income ratios around 70% (BNP Paribas’ figure includes its wealth division). This is about 10 percentage points worse than the big US independents and Amundi, according to research from Deutsche. Equivalent divisions in the US, such as at Goldman Sachs and JPMorgan, are similarly inefficient.

Middling bank-owned asset managers are struggling partly because of their focus – or lack of it. For example, although UBS is the world’s biggest wealth manager with over $2 trillion under management, only a minority of its own products are sold through the private bank, which uses hundreds of other asset managers. BNP Paribas and DWS have even smaller proportions of captive assets, although larger proportions of domestic ones.

Compared with banks with smaller fund arms, the asset-management mid-tier tends to have wealthier clients, bigger private banks and bigger corporate and institutional banks. Yet DWS and UBS have far higher inflows of passive products than Amundi, according to BCG. All this could make it harder for them to replicate Amundi’s route from a mega-captive to a more efficient global player offering mainly active funds.

Deutsche Bank, nevertheless, has followed Crédit Agricole by awarding more independence to its asset management division: with a rebranding last year to DWS and then listing it this year, partly to create money for acquisitions.

Independent firms can enjoy greater freedom to compensate fund managers according to their performance and therefore to attract the best people – each one costing perhaps several million euros a year for high-end funds. Asset managers that are fully owned by banks have bonus caps reflecting the EU’s Capital Requirements Directive IV. And bank shares are an unattractive bonus currency, particularly at a firm like Deutsche Bank.

Compensation was a large part of the rationale for the IPO of DWS, although not of Amundi, according to Moreau and Perrier.

“We now have better ability to have our own remuneration structure that’s consistent with the remuneration structure of asset management,” Moreau told Euromoney.

This is especially beneficial for alternative investments, he noted.

Greater distance from a parent bank might also be suitable for a firm like Deutsche, given the starkly different personalities of those on the trading floor and those charged with stewarding third-party money. The problem is it then raises the question, again, of whether the bank should own it at all.

The question of focus is also relevant for firms such as BNP Paribas, UBS and especially HSBC, as their asset management arms are such small parts of the banks’ overall businesses, and so can struggle for attention at the top.

Chandrasekharan says the idea that HSBC punches below its weight in asset management is a fair comment. However, he denies any neglect of the division.

“The support for this business has remained throughout,” he says. “The fact that John Flint is group chief executive is clearly something we are proud of.”

In fact, like others, HSBC is aiming to work more, not less, closely with the parent, its clients and brand.

“We have access to a global footprint and client franchise,” says Chandrasekharan.

BNP Paribas and UBS, similarly, have moved away from a multi-boutique model in asset management in recent years, mainly to cross-sell better and reap operational and marketing synergies from the parent. UBS’s Körner says he gains valuable revenue synergies in product development, credibility and cross-selling opportunities with UBS’s private and corporate and investment bank.

BNP Paribas Asset Management’s chief executive Frédéric Janbon reveals a similar attitude.

“Being part of BNP Paribas gives us a brand associated with stability, a solid risk-management skill set, good ethics and access to a wide network of potential corporate and institutional clients,” he says. “That fits well with what institutional clients look for in their asset management partners.”

Death

The asset management industry has been predicting the death of the captive fund manager for several years now. But regulation does not require banks to have an open architecture model, while more captive players are more efficient. Often, the ability to get closer or stay close to the bank is their best chance for growth.

The Spanish bank-owned asset managers are in a smaller category of largely captive managers. They have less than €200 billion under management, but excellent cost-to-income ratios: below 50% at Santander and even below 30% at BBVA.

“Independent and diversified asset managers need scale, to have the right teams, processes and IT,” says Santander’s Matarranz. “We are a different animal, as being part of a group can be a differentiator.”

In Italy, Eurizon has a cost-to-income ratio of just 21%. It has seen inflows even as domestic politics have pushed down local markets over the last year.

“The battle will be played not only on the quality of the products but also the quality of service to the distributors, and this is a battle in which we have an edge,” argues Eurizon’s chief executive Tommaso Corcos. He says this advantage will only grow under Mifid II.

Yet bankers and analysts insist primarily captive players will, in future, need better products.

“Some of the asset managers owned by banks in Europe work predominantly with the bank’s client base and are mostly concentrated in individual countries; for these reasons they generally have more limited manufacturing skills versus leading independent asset managers,” says Cocini at BAML.

Intesa Sanpaolo’s chief executive Carlo Messina seems to agree and has sought greater manufacturing scale for Eurizon. He mooted a partnership with a global firm earlier this year – potential candidates were rumoured to include BlackRock – as a possible way to achieve it. Berenberg thought the idea suggested fee income growth and Eurizon’s penetration in Italy is peaking if Intesa Sanpaolo was willing to sell a stake in what is perceived to be its prime asset.

“We expect there will be more consolidation,” Cocini continues. “In five years’ time, banks will be much less likely to own undifferentiated fund providers. Either they will own a stake in larger and independent firms – with best-in-class investment expertise and more diversified by geography and client type – or they will have exited.”

You have a number of smaller asset managers that have a strong investment process but are finding it difficult to get access to distribution – Nils Bolmstrand, Nordea

Bank-owned asset managers might now have a choice between aiming for the top in terms of their funds’ outperformance or just taking a good enough product and, like Amundi, investing in distribution, which is often their key differentiator anyway.

The ideal is to do both at the same time, but in practice that is hard, says BCG’s Frankle.

One way of mimicking Amundi’s successful meshing of smaller bank-owned asset managers could be to do a three- or even four-way merger: perhaps between Eurizon, Santander, BBVA and Nordea.

Mergers could also be with the asset management arms of insurers.

Axa Investment Managers was rumoured to be in talks over a merger with its equivalents at Natixis and BNP Paribas late last year, according to Reuters. Italy’s Generali is pushing to extend its asset management activities and could gain better revenues from the unit-linked policies it outsources today if it were part of a more formal partnership.

Partnerships between those with good distribution and so-so products, or between firms with good products and less distribution, seem like logical ways of solving the challenges at either end of the industry.

Buying a boutique asset manager is one method of doing this, such as Nordea’s acquisition of 40% in Swedish hedge fund Madrague Capital Partners this summer.

“You have a number of smaller asset managers that have a strong investment process but are finding it difficult to get access to distribution,” says Bolmstrand.

It is a model Natixis has long pursued. Raby gives the example of the benefits that European private debt firm MV Credit gained from being acquired by Natixis this year.

“They immediately gained more fame among clients,” he says. “We have enhanced their profile and allowed them to reach a broader set of clients, while not diluting their focus on fund management.”

But bigger mergers could also do something similar. Aside from the mooted BlackRock-Eurizon tie-up, for example, DWS could merge with the asset management arms of a bank like Santander or BBVA.

Similar partnerships have already taken place between more dedicated asset managers and the financial arms of the French and Italian post offices.

Last year, Italy’s Poste spun off its life insurance portfolio management to Anima, an asset management company previously owned by Banca Monte dei Paschi di Siena. That followed the 2015 purchase of a 25% stake in La Banque Postale Asset Management by Dutch insurer Aegon.

Less ambitiously, outsourcing platforms set up by larger firms, like Amundi Services, could be different steps in the same direction. UBS Partner, for example, launched in March with a white-labelled advisory offering, including asset allocation and risk management, so wholesale clients such as retail banks can more easily comply with new disclosure requirements. Banca Generali, the insurer’s private bank, is one of its first clients.

“Strategic partnerships can be on different levels,” says UBS’ Körner. “It could be in product development. I could also imagine that distribution partnerships could become more important for the industry as a whole.”

Amundi: Moving beyond a mega-captive

With his ruffled hair and sceptical air, Yves Perrier cuts a very different figure to the all-American chief executives at the world’s other top asset managers.

Over the last 10 years, the veteran French banker has turned Amundi into a European BlackRock – much larger and more efficient than its peers – although the journey to get there has been very different and much more European in character.

|

|

|

Yves Perrier |

“There are two ways to define a strategy: try to be what you would like to be, or to try to be what you can be successfully,” Perrier tells Euromoney.

One implication of that is that Amundi would struggle to compete head-on with the big US players in their home market, for example, but it can grow in Asia. In the past, such realism has characterized Perrier’s investment in bank distribution in Europe.

The firm’s route to almost €1.5 trillion in assets under management lies in the pragmatic 2009 merger of what one analyst describes a sub-scale asset manager at Crédit Agricole with an even more sub-scale asset manager at Société Générale. That created Amundi – the name is deliberately Latin rather than French-sounding.

The union was the basis to gain greater scale in distribution and to manufacture products more efficiently. A distributor like Deutsche Bank might now offer its clients Amundi products, for example, and about two thirds of its assets under management now come from institutions.

Amundi’s growth continued after its 2015 IPO (when SocGen sold out), first with the acquisition of the asset management arm of Austrian bank Bawag PSK and then of Pioneer, UniCredit’s equivalent.

The latter deal made it the second biggest asset manager in Italy, with €170 billion in assets under management. Perrier says the €3.5 billion Pioneer deal was “an initiative of Amundi, in line with the global strategy of Crédit Agricole,” in which Italy is its second domestic market after France.

Years of experience in the risk and finance departments of SocGen and then Crédit Agricole helped Perrier achieve all this. He also oversaw the merger of Crédit Lyonnais with Crédit Agricole in 2003.

Today, less than a third of Amundi’s fund volumes are captive. When Perrier took over the French bank’s asset management arm in 2007, by contrast, it was the other way around, with almost three quarters of funds coming from the parent. However, despite its leading size, Amundi is still something of a half-way house between the global firms like DWS and UBS Asset Management and local captives like Eurizon and the Spanish.

We bring the savior faire and they bring the distribution – Yves Perrier

France still accounts for the majority of Amundi’s business and, despite its acquisitive growth, Perrier still regards Crédit Agricole’s French regional banks as Amundi’s first clients. He sees that link as a great advantage.

SocGen accounts for a further 8% of assets under management, and distribution agreements with Bawag and UniCredit were also key elements of those acquisitions. Italy is now its second-biggest distribution market after France.

“The acquisition of more assets under management was not so important as the chance to reinforce the business model in distribution capacity, especially in Italy, Germany and Austria, and to gain US expertise and talent,” Perrier says of the Pioneer acquisition.

Pioneer could give it a particularly useful leg up in Germany. Low rates are forcing German savers into higher-risk products and Perrier hopes to double the approximately €40 billion in assets under management in the country in the next two years. Amundi is vying with BlackRock to be Germany’s biggest foreign-owned asset manager.

Joint ventures set up shortly after Amundi’s creation with Agricultural Bank of China, State Bank of India and Korea’s NH hold about €100 billion – and further strengthen its bank distribution model.

“We bring the savior faire and they bring the distribution,” Perrier explains.

He hopes those agreements will help him reach €300 billion in assets under management in Asia by 2020. Fully controlled operations in Hong Kong, Taiwan, Malaysia and Japan constitute another €100 billion in Amundi’s Asian business today.

Now in his mid 60s, Perrier says he has five years before Amundi’s policies would oblige him to retire. And he is still looking to the future. One initiative is the recent launch of Amundi Services, allowing smaller asset managers to outsource their operations to Amundi. This should both boost revenues and encourage Amundi to improve the quality of its own operational set up.

“Technology is often underestimated in our industry,” he says. “That’s a mistake. Of course, you have the talent of the active asset manager, but good risk management and reporting also needs a very efficient IT platform.”

Natixis IM: Building the LVMH of money

Natixis is perhaps the most likely of all Europe’s big bank-owned asset managers to stay with its parent group.

After the 2008 crisis, under former insurance executive Laurent Mignon, Natixis dramatically cut risk-weighted assets in its corporate and investment bank. Meanwhile, in asset management it has made a string of bolt-on acquisitions: most recently European private debt firm MV Credit and a 25% stake in US equity manager WCM this year.

It has grown steadily from around €500 billion assets under management at the beginning of the decade to approximately €850 billion today.

|

|

|

Jean Raby |

With Mignon becoming chief executive of the parent BPCE group earlier this year, Natixis is now targeting double the revenue growth in wealth and asset management versus the investment bank (6% and 3% respectively) and the two divisions are already almost equal in terms of revenue contribution.

It is also seeking to do more to transfer expertise it has gained in the US to Europe and Asia Pacific; building up sales coverage, trying to build stronger relationships with distributors in continental Europe outside France and buying a majority in Australia’s Investors Mutual Limited last year. Future acquisitions are most likely to be in alternative investments and Asia.

Natixis occupies an odd position. Despite being owned (like Amundi) by a large French retail-focused mutual group, it does not see its primary advantage in gaining scale to make competitively priced products.

We are not going into passives or exchange-traded funds, as that’s where the fee pressure is biggest – Jean Raby

It generates slightly more revenue than Amundi, despite much lower assets under management, but has a higher cost-to-income ratio and has no intention to move in line with Amundi’s level of efficiency; it also has less of its business in France than Amundi. Overall, the aim is to be the LVMH of asset management, with a range of luxury brands.

“We are not going into passives or exchange-traded funds, as that’s where the fee pressure is biggest,” says Jean Raby, the divisional head, whose exuberant character contrasts with the quietly spoken and more considered new Natixis group chief executive, François Riahi.

Natixis has a much bigger US business than Amundi, thanks to the purchase of an American multi-boutique asset manager in the early 2000s. Unlike its peers, it has hung onto that structure and sought to develop it by acquiring and launching other boutiques in the US and Europe – even as the multi-boutique model has gone out of fashion elsewhere due to the desire to achieve better synergies from acquisitions.

Raby says this multi-boutique model allows for a more entrepreneurial approach. In the firm’s vision, it is a kind of federation: 26 neat compartments within a clearly contrived pattern. The affiliates benefit from common distribution, seed money, as well as some operational support, although the structure sometimes inhibits its ability to centralize and gain economies of scale, including in IT.

Most recently, Natixis even changed the name of its France-focused division (now Ostrum, previously Natixis Asset Management) to make what is still its biggest unit look more like another boutique in the overarching asset management company (Natixis Investment Managers, previously Natixis Global Asset Management).

“From the perspective of our business model, it has been kind of a reverse takeover, with the multi-boutique model rolled out over time in Europe,” says Raby describing the legacy of the US acquisition.

UBS AM: The pain before Chinese gain

Asia offers huge promise for UBS Asset Management – perhaps more so than for any other bank-owned asset manager in Europe.

China’s onshore fund management industry is forecast to grow by almost six times to $12 trillion in the next 10 years, according to China-focused Z-Ben Advisors. The same firm ranks UBS as China’s top foreign asset manager, bank-owned or otherwise, according to the scope of its capability in the country. The only other Europeans in the top 10 are HSBC (eighth) and DWS (10th).

|

|

|

Ulrich Körner |

For now, however, Asia only makes up about 20% of UBS’ assets under management, making Europe including Switzerland still by far the biggest region for the firm. And China does not even dominate the 20% in Asia.

“For a foreign asset manager’s perspective, China is a medium- to long-term option,” admits UBS Asset Management president Ulrich Körner.

In the short term, Körner – a former consultant who was UBS’ chief operating officer between 2009 and 2013 – will be hoping to show better margins closer to home. UBS had Europe’s second-biggest exchange-traded fund inflows after BlackRock in the first half of 2018, according to ETF GI. Even so, the asset management division’s cost-to-income ratio is one of the worst in its peer group, rising to 72% in 2017.

Its efficiency ratio continued to deteriorate in the first half of 2018, reaching 74%, while its revenues declined slightly on the same period last year. UBS also gains relatively little revenue as a proportion of its assets under management, compared with peers with similarly high cost-to-income ratios such as DWS.

We have been through a fundamental transformation, with the goal of reforming the business and returning to profitable growth – Ulrich Körner

Nevertheless, Körner says UBS has grown its assets under management by twice the market rate since 2016, despite not making acquisitions. Moreover, he thinks a 2014 to 2017 transformation plan has put it in good stead.

It has integrated the asset management firm’s various elements more closely, with a new core IT platform, moving away from the previous multi-boutique structure. It also sold its Alternative Fund Services business to Japan’s MUFG in 2015 and its Swiss and Luxembourg fund services business to Northern Trust in 2017.

“We have been through a fundamental transformation, with the goal of reforming the business and returning to profitable growth,” Körner concludes.

Meanwhile in China, last year UBS was one of the first foreign asset managers to gain a licence to offer fixed income, equity and multi-asset funds onshore. Previously it was one of the first to set up a minority-owned joint venture in the mid-2000s.

The new licence only allows the firm to target institutional and high net-worth clients. Körner hopes that in the coming few years it will be able to offer funds to a wider public through its wholly owned onshore entity.

“I’m convinced this market is opening up,” says Körner. “The private fund licence is a step in that direction.”

DWS: Distance from Deutsche is no cure

When Nicolas Moreau spoke to Euromoney in September, he emphasized the benefits of his company’s newfound distance from Deutsche Bank, after rebranding to DWS late last year and then a partial IPO in March.

“The brand was intended to make sure that we were perceived as an asset manager in our own right, and not just as a department of Deutsche Bank,” said Moreau, then chief executive. “Even when the bank was facing some challenges, we were still on-boarding business.”

|

|

|

Nicolas Moreau |

For Moreau, a Frenchman who previously worked at Axa, the distance from Deutsche may not have been great enough, as his bank-dominated board replaced him with immediate effect after third-quarter results were announced.

Outflows of €2.7 billion in that quarter – mainly due to the US business – ultimately spelled the end for Moreau, following outflows of €4.9 billion in the second quarter.

Although reductions in expenses have been more promising than at close peer UBS Asset Management, DWS’ inflows in the third quarter were flat, even in passive funds, which have been responsible for the bulk of them at DWS and UBS lately.

Moreau proved unable to stem the gradual slide in DWS’s share price since its IPO.

Poorly performing retail funds in Germany were an annoyance and contributed to outflows, although redemptions of institutional mandates have been a bigger problem in the US, where Deutsche’s market share and image is less robust than in Germany.

The brand was intended to make sure that we were perceived as an asset manager in our own right, and not just as a department of Deutsche Bank – Nicolas Moreau

Perhaps the choice for Moreau’s successor, Asoka Woehrmann, indicates a turn towards home. Its scope to grow in its domestic market – where it has a 25% share – is limited, although there is a gradual shift to private-sector pensions and higher-risk retail investments in Germany.

Woehrmann was previously DWS’ chief investment officer. From 2015, he ran Deutsche’s German retail bank, when Christian Sewing – Deutsche group chief executive since April – was head of Deutsche’s private and commercial division.

DWS was at pains to reaffirm its global ambitions when announcing Moreau’s removal. It also recommitted in third-quarter results to Moreau’s plan of working towards using the listing as a basis on which to act as a consolidator after 2020, once it has proven its worth in the public market.

One investment banker in Frankfurt argues that Deutsche could boost its asset management income, even if a big merger with DWS happened through a share swap that diluted the bank’s stake so much it lost control of the combined entity. The listing certainly gives a clearer value for the asset manager.

Yet even if acquisitions see Deutsche’s stake fall below the 78% it owns today, the group’s supervisory and management board intend to hang onto the majority, Moreau told Euromoney in September.

This would be a similar approach to Crédit Agricole, which dropped to a 70% holding from 76% during Amundi’s rights issue associated with its Pioneer acquisition.

Santander AM: Home advantage

Three years ago, the plan to merge the asset management units of Santander and UniCredit showed that consolidation among the bank-owned asset managers was coming – and could involve the Spanish banks.

Partly due to regulatory hurdles, the two banks called off the merger around the time Jean Pierre Mustier became chief executive of UniCredit in 2016. Santander’s repurchase of half of its asset management arm from US private equity firms General Atlantic and Warburg Pincus followed a few months later.

|

|

|

Victor Matarranz |

For Santander, the repurchase of this €177 billion asset manager is a chance to make more use of the link to the group. It merged its wealth and asset management divisions late last year under Victor Matarranz, previously head of group strategy.

“There was a misalignment between the asset manager and the retail bank,” says Matarranz. “That didn’t work and it wasn’t sustainable. Now, as part of the new structure, we need to win the trust of retail and other customers and align back, so we’re more in touch with their needs.”

Spain is a mid-sized fund market in Europe. But Santander – like BBVA – has the benefit of Latin America. CaixaBank’s asset manager is much smaller, with around €45 billion. BBVA’s division has €105 billion, which includes about €30 billion in LatAm. At Santander, a large Brazilian business means that LatAm accounts for about the same as Spain within its unit.

We need to win the trust of retail and other customers and align back, so we’re more in touch with their needs – Victor Matarranz

That is not to say Latin America is an easy ride. In Brazil, locals such as Bradesco and Itaú each manage more than $100 billion, while newer firms, such as XP Investimentos, also compete with the internationals.

Santander and the other Spanish firms do not stray much from their strengths: in-house clients, eurozone equity and fixed income, and Latin America. Santander partners with bigger asset managers in US equities, although like other European bank-owned asset managers, including BBVA, it has invested in multi-asset products to move away from more commoditized single asset-class funds.

In the longer term, Santander and BBVA’s wider digital strategies – in this case robo-advisory and online distribution – might allow them to grow further. Santander’s decision to appoint Mariano Belinky as its asset management head in February might signal a step in this direction. Belinky was previously head of Santander InnoVentures, a fintech fund.

|

BNP Paribas AM: A happy medium?

The acquisition of a majority of Belgian robo-advisory platform Gambit late last year shows how keen BNP Paribas is to emerge victorious from the technology-led disruption facing Europe’s asset managers.

Nevertheless, with €560 billion under management at the end of June, asset management chief executive Frédéric Janbon betrays no desperation to reach the commonly stated $1 trillion rule for minimum scale – despite rumours last year of a potential merger with Axa Investment Managers.

|

|

|

Frédéric Janbon |

Janbon says BNP Paribas Asset Management could now do further small and medium-sized acquisitions, although probably nothing with a price tag in the €1 billion-plus range yet. That is partly as the division is, like UBS, still proving itself after a deep restructuring in the last two years, moving from a broadly multi-boutique model to a single brand and IT platform.

“Scale matters in integrated asset management companies like ours, but we can generate value for our clients and shareholders with less than $1 trillion,” insists Janbon.

It does not break out revenue figures for asset management specifically, but BNP Paribas’ combined asset and wealth management franchise also has a cost-to-income ratio of a painful 76%.

Like other mid-sized bank-owned asset managers in Europe, BNP Paribas carries a more diversified and international set-up: operating in about 30 countries, across active equity and fixed income management, multi-asset solutions, private debt and real assets. BNP Paribas Easy manages a further €20 billion in index and exchange-traded funds.

We can generate value for our clients and shareholders with less than $1 trillion – Frédéric Janbon

The proportion of assets from its home market, about 40%, is similar to Deutsche Bank’s DWS. But France’s economy is much smaller than Germany’s, and if one adds Belgium (where BNP Paribas also has a large market share thanks to Fortis) the French bank’s home-market share rises above 50%.

Perhaps BNP Paribas’s group chief executive Jean-Laurent Bonnafé just wants to make up his own mind up about how each part supports the rest. The bank’s results releases put wealth management (€373 billion) and insurance (€240 billion) together with asset management to reach more than €1 trillion under management.

By that measure – leaving aside profit margins – it has much greater scale.

Eurizon: How to save a star captive

Despite Italy’s banking and political crises, managing private wealth has allowed Intesa Sanpaolo to outperform UniCredit for years, despite the fact that it is more focused on Italy than its rival. Eurizon, Intesa Sanpaolo’s asset management company, is a crucial part of that story.

Eurizon has grown rapidly over the last five years, more than doubling its assets under management, and has continued to grow in the first half of 2018. In 2017, it saw Europe’s biggest inflow among captive asset managers, €23 billion – more than Deutsche’s far bigger DWS – according to BCG. It is also exceptionally efficient, with a cost-to-income ratio of just 21%.

|

|

|

Tommaso Corcos |

Captive retail fund houses in Europe could face the same pressure on fees that their global, institutionally focused peers have already suffered. Intesa Sanpaolo, at least, is doing something about this while its financial results remain relatively positive. In February, chief executive Carlo Messina’s new four-year business plan indicated that bulking up in product development is more of a priority than distribution.

Messina has since been vocal in discussions about M&A – even if rumours about a tie-up with BlackRock have dried up. Reducing the bank’s stake in Eurizon, in any case, could be a way to facilitate a merger to create a bigger European asset manager.

It’s important for the wealth manager to have a long-standing relationship with the portfolio manager and product provider – Tommaso Corcos

Despite its geographic position, Italy is in some ways closer to the UK than France or Germany as an asset management market, due to the role of financial advisers or promotore in offering a variety of funds. In the Italian case, this often favours the products of the bank to which the advisers belong.

But Eurizon is already diversifying away from Italy, deploying more sales people in Germany, France, Spain and Switzerland, and buying a majority stake in London hedge fund SLJ Partners in 2016.

Eurizon chief executive Tommaso Corcos says the link to the bank is vital, as it gives the asset manager an understanding of the customers’ needs, while Eurizon can help the bank better advise its customers, avoiding emotionally driven allocation decisions.

“It’s important for the wealth manager to have a long-standing relationship with the portfolio manager and product provider,” he says.

|

Credit Suisse AM: Better alternatives

Like other banks, Credit Suisse sets out asset management as a key pillar of its offering and a strategic priority. Yet its relatively small place in the market today – about €350 billion under management – is the legacy of the 2008 sale of its traditional businesses outside Switzerland to Aberdeen (now merged with Standard Life).

|

| Michel Degen |

Credit Suisse gains a much higher amount of revenues as a proportion of assets under management (38%) than predominantly retail asset managers (mostly about 20%) and UBS (29%). The latter’s fund management arm is much bigger and has better net new money flows, although in the first half of 2018 Credit Suisse saw a 5% rise in revenues, as UBS’s revenues fell slightly.

Around €90 billion is in alternative asset classes, which are expensive to manage. Even so, Credit Suisse Asset Management’s cost-to-income ratio improved to 66.5% in the first half of the year, making it look slightly more efficient than UBS, despite its growth in passives.

Through entrepreneurs, we have access to the pension funds and cash management of mid- and large-cap companies – Michel Degen

The link to the wider bank is helpful because of the introductions it allows to institutions and corporate clients, says head of Europe and Switzerland Michel Degen.

“Through entrepreneurs, we have access to the pension funds and cash management of mid- and large-cap companies.”

Degen’s unit is the biggest part, with a combined €236 billion. He oversees product factories for equity and fixed income funds, balanced and index solutions, real estate and infrastructure. However, Eric Varvel – previously associated with the investment bank – oversees the business from New York.

The Americas grouping, under Peter Norley, is responsible for the Credit Investment Group, covering high-yield senior secured loans and collateralized loan obligations. With about €50 billion, it is one of the biggest CLO investors in the US.

Norley also oversees its commodities and insurance-linked funds and a partnership with New York hedge fund manager York Capital, in which Credit Suisse bought a 30% stake in 2010.

|

HSBC GAM: A small business sees its moment

Euromoney’s eyes invariably glaze over when bankers talk about how much they care about their clients. But it is clearly the case that cross selling offers HSBC a relatively greater opportunity to bag institutional mandates than other bank-owned asset managers.

That is because in the past it has left the low-hanging fruit on its corporate and investment banking tree to be picked by smaller competitors. It is Europe’s biggest bank by assets and capitalization, but in asset management, the continent’s other large corporate-focused firms – BNP Paribas and Deutsche Bank – are much bigger than the UK lender’s €400 billion-odd under management.

|

|

|

Sridhar |

Now, it hopes to gain much more business from HSBC’s global banking coverage of, for example, sovereign wealth funds.

“We want to be the leading asset manager for HSBC’s clients across the spectrum. That’s an aspirational goal,” says Sridhar Chandrasekharan, HSBC Global Asset Management chief executive. “I take pride in saying 100% of our business in asset management is from HSBC’s clients, in the knowledge that HSBC is a global bank.”

If Chandrasekharan succeeds, this will be partly a result of his predecessor John Flint, now group chief executive. Flint staged an initial shift towards greater integration with the parent and away from a multi-boutique model when he ran the asset manager between 2010 and 2012.

Today, although it does not break out costs, HSBC GAM’s relatively small revenue as a proportion of assets under management is in line with mainly domestic and captive bank-owned asset managers.

We want to be the leading asset manager for HSBC’s clients across the spectrum. That’s an aspirational goal

– Sridhar Chandrasekharan

Although it mostly manages institutional money, the UK remains HSBC’s biggest asset management market, particularly its private bank there. One rival UK asset manager says it provides funds for the British bank’s network on a “semi-open basis”, which is already an advance what it did 10 years ago.

HSBC GAM is growing steadily, although unspectacularly: building up its passives range and, like many European banks, it wants to grow its capacity in sustainability investing.

DWS and UBS have better capability in China than HSBC, according to Z-Ben Advisors, which is clearly something else it will try to rectify.

Nordea AM: Future proofing

European bank-owned asset managers searching for ways to build a future beyond their own captive networks – and unwilling or unable to follow Amundi’s distribution-focused acquisition strategy – could look to Nordea’s model.

The asset management arm of Scandinavia’s biggest bank has grown its assets under management by around 50% to €213 billion over the last five years. It has the efficiency and size of a typical captive asset manager, with a 28% cost-to-income ratio. It expects to continue distributing a good majority of its products (72% today) within Scandinavia, where it has a 16% share.

|

|

|

Nils Bolmstrand |

However, compared with the southern European captive players, Nordea has a larger share of funds from third-party clients. Most of its fund volumes are still distributed to in-house clients (53%) but it expects that proportion to fall, so third-party clients could soon make a majority.

Nordea retains a multi-boutique structure on the product side but centralizes the back and mid office to a greater extent than Natixis, for example. That is in large part the legacy of Christian Clausen. Nordea’s group chief executive between 2007 and 2015 was previously the long-standing head of Nordea Asset Management. He is now BlackRock’s Nordic chairman.

Compared with peers, Nordea Asset Management has invested more in wholesale distribution in continental Europe, where it has marketed covered-bond funds and other products, particularly in Germany but increasingly in Italy and Spain. It is even establishing distribution channels in Latin America.

With the right product set, you can attract assets at an attractive cost-to-income ratio – Nils Bolmstrand

“We’ve been able to stay close to the Nordea distribution and develop appropriate products for similar distribution channels, particularly other banks,” says Nils Bolmstrand, head of asset management since late 2016. “With the right product set, you can attract assets at an attractive cost-to-income ratio.”

Nordea’s blockbuster fund – one of the most successful across Europe in recent years – is its multi-asset Stable Return fund, which manages about €13.5 billion for a 1.5% fee. It is particularly popular among UK institutional investors.

The fund’s webpage markets Nordea’s “conservative culture” that is “deeply rooted in our Nordic genes”. That is despite Nordic investors generally having an unusually strong risk appetite, at least by European standards, with a greater predilection for equities, according to Bolmstrand.