(Left to right): Greg Fleming, Michael Baer, Sallie Krawcheck, Jürg Zeltner and Marc Syz

Illustration: Neil Edwards

|

IN ADDITION |

|

|

|

Make no mistake, the familiar landscape of the wealth management industry is about to undergo a seismic shift. And when the revolution comes, it will be led by some familiar faces.

In New York, former Morgan Stanley wealth management head Greg Fleming, now chief executive and co-owner of Rockefeller Capital Management, has a new brokerage licence and is also building strategic advisory.

In Switzerland, Michael Baer, scion of a family synonymous with private banking, is getting ready to open the doors at his new merchant bank.

Marc Syz, son of the founder of one of the most successful private banks launched in the past 25 years, is on his way to Asia to make the first deal for his new private market investment and advisory business, Syz Capital.

Jürg Zeltner, the man behind UBS’s stranglehold on global wealth management in the decade since the financial crisis, is starting a new venture – rumoured to be a boutique.

Sallie Krawcheck, who ran both Smith Barney and Bank of America’s wealth management operations, is making waves and attracting assets at Ellevest, which she set up five years ago.

Alongside these new focused and nimble entities, family offices are increasing, multifamily offices are expanding and specialist wealth managers are emerging to serve specific segments such as impact investors, women, or even clients that want the autonomy and low fees of a digital adviser.

Industry executives are quick to draw a comparison with other financial services sectors. Over the last decade, a slew of senior investment banking executives has bid farewell to their respective houses to launch their own boutique advisories and fintech businesses. Before them, hedge fund managers had spun out of asset management firms and investment banks.

It is now the turn of the wealth management industry to have its reinvention, insiders say. For a decade, there have been predictions of a barbell industry of large scale players offering breadth and global reach, and specialized firms at the other end that go deeper for fewer clients. Now that a perfect storm of cost and revenue pressures, technology, transparency and client demographics has occurred in the wealth management industry, those predictions look like they are finally coming to pass.

‘Different world’

“We grew up as bankers in a different world of banking,” says Baer, speaking for many of his peers. As the great-grandson of Julius Baer and former head of the bank Julius Baer started, he has earned the ability to make such a claim.

It was simple, he continues, the job of a banker was to listen to a client, solve their problems and express that solution in financial terms.

“If you go all the way back to the Warburgs and Rothschilds, or look at the history of JPMorgan or Credit Suisse, you’ll find banks were set up to serve one entrepreneur and then added relatively few clients. They focused on helping them build their wealth and manage the business finances in addition to their personal finances. It’s the definition of a merchant bank.”

|

|

|

Michael Baer, MBaer Merchant Bank |

Baer is now going to join them with the launch of MBaer Merchant Bank in April. In a world of increased regulatory costs for banks, it could be seen as a bold move. Indeed, it is the first merchant bank to be opened in Switzerland in some 30 years.

But Baer sees the need for an alternative proposition.

“Banking hasn’t been great since the early 1990s,” he says, pointing the finger somewhat at the influence of consultants. “Their talk of scale and mass and bigger balance sheets and higher returns and segmenting clients… It put banks into overdrive to where, pre-crash, we saw UBS, Deutsche Bank and Credit Suisse chief executives trying to trump each other on return on equity. It was such a deviation from the basic definition of banking.”

The outcome for wealth management clients of these large universal bank models, says Baer, is that they now find themselves having endless relationships within a bank, which lowers the level of service.

“Personal loans are dealt with by one division that isn’t familiar with your entire wealth profile, so you might wait months for approval,” he says. “Meanwhile, your business is handled in another division, and family wealth in yet another again.”

Baer points out that at the same time the constant redefining of client wealth segments has meant clients have seen long-standing relationships with advisers severed and service levels altered more than they can tolerate.

“The merchant bank model on the other hand was and is to have fewer clients and know them well, whether they have $1 million or $100 million,” he says. “It’s about understanding their business, so that you can offer them advice be it on a next-gen issue or advice about the business and trade finance.”

Greg Fleming has also thrown his hat – together with his experience and some considerable financial firepower – into the ring. He is another banker highly familiar with the inner workings of large wealth managers, having been the president of both Morgan Stanley Wealth Management and Merrill Lynch.

Fleming teamed up with the Rockefeller family and the private equity arm of Viking Global Investors to buy Rock & Co multifamily office last year. Now with a broker-dealer licence, he is building the newly rebranded Rockefeller Capital Management, not just as a multifamily office but also a high-end advisory brokerage business and a strategic adviser – essentially a merchant bank.

The opportunity, he says, in addition to the brand quality of Rockefeller, is that “it’s harder for large firms to efficiently connect their high-end clients across both strategic advisory and wealth management, or to bring intellectual capital to bear. At a smaller firm, we can have the focus to do that.”

Through the acquisition of financial advisory teams, a family office or two, and a boat-load of intellectual capital, Fleming thinks he will increase assets under management (AuM) from $18 billion to $30 billion this year, with a soft, five-year target of $100 billion.

“AuM is not the key here though,” he says, “it’s about bringing the best service and products to high-end clients.”

Typically those with assets above $25 million, he clarifies.

Wealth management is a scale business, so to survive boutiques will need to have a premium pricing model, and the good ones will do that through exceptional service and leading with lending products – James Gorman, Morgan Stanley

Syz also believes that as wealth management has trended towards fewer and larger service providers, an opportunity has arisen for specialist wealth management firms to emerge. He is co-running the newly created Syz Capital, which brings entrepreneurial clients and families together to access private market investments and solutions for their own businesses.

“Wealthy families and individuals can gain access to the largest private equity and hedge funds through feeder funds at the large wealth managers,” he says. “Or if they want to go into a deal directly with the likes of Carlyle or Blackstone, they will need $10 million to $25 million minimum investments. But in both cases, they’re investing in large investments with institutional-type risks and returns.

“Gone are the opportunities to invest directly in a business venture with a few other entrepreneurs and families with complimentary expertise to really create value.”

And this is precisely what Syz Capital intends to provide.

In essence, clients are on the hunt for a new type of service. That explains the 10% rise in assets at multifamily offices last year and the growth in single family offices.

At the same time, after waves of consolidation in the mid to late 2000s, the largest wealth managers are becoming bigger still. The top 10 wealth managers by AuM oversaw $12.38 trillion at the end of 2017, according to Scorpio Partnership.

The top three – UBS, Morgan Stanley and Bank of America Merrill Lynch – held more than half of that, some $6.8 trillion between them. That makes them enormous.

BAML has around 17,500 advisers, Morgan Stanley more than 15,500 and UBS just under 10,700.

And there is room to grow. The latest world wealth report from Capgemini showed high net-worth wealth (above $1 million in investable assets) to have surpassed $70 trillion globally in 2017. That number is on course to exceed $100 trillion by 2025, making the $6.8 trillion at the top three managers seem just a drop in the ocean.

The largest wealth managers argue that there are factors that mean a successful future for those with scale. Size affords a global footprint, for example.

Tom Naratil, co-head of UBS Wealth Management, points to the data.

“Over 65% of those with $5 million and above have lived or worked in another country for at least three years, or have owned real estate or a stake in a business in another country,” he says. “And the trend towards wealth becoming more global is just increasing. Some 80% of wealthy business owners aged 21 to 34 have global businesses, versus 35% of the over 65-year-old business owners of today. With wealth creation growing at twice GDP, there will be new entrants poking around the edges, but the demographics point to global footprint being crucial – and that requires scale.”

The global nature of markets, he adds, also requires firms with global expertise.

Tom Naratil, co-head of UBS Wealth Management

“The next decade is going to be more complex and clients will require more advice,” he says. “Global trade economics, the political environment and pace of change is cause for concern for clients, and they need guidance. It highlights the necessity of having a global footprint and reinforces the need not to be international – which a lot of firms are – but actually to be global, onshore in every region.”

The boutiques and specialists cannot claim to be plugged in globally to the same extent, but they can counter that they can go deeper into one segment, whether that is a specific geography, style or client sector.

Lending also seems an obvious possibility for boutiques, says James Gorman, chief executive of Morgan Stanley, although he is clear that scale is the only game in wealth.

“Wealth management is a scale business, so to survive boutiques will need to have a premium pricing model, and the good ones will do that through exceptional service and leading with lending products,” he says.

Clients are only going to be willing to pay for quality advice and they won’t be willing to pay for transactions at all. The transparency is now there for them to make those value judgments – Iqbal Khan, Credit Suisse

Exceptional service requires talent, however, and larger banks will argue that scale attracts talent – that the best advisers want to know they are working for a bank that has access to any product or service their client desires.

Indeed, Naratil says that size can even reduce recruitment costs.

“[Breadth] is part of advisers’ compensation considerations. If they know they can do more for their clients with your platform, they know they will make more money even if the percentage compensation is less than at a competitor.”

|

|

|

Peter Charrington, Citi Private Bank |

It is an important point because as Citi Private Bank’s global chief executive, Peter Charrington, points out: “What hasn’t changed in 30 years is that talent doesn’t grow on trees.”

Recruitment costs may have eased off a little, but good advisers can command high salaries, say banking executives.

But specialist advisers with good brands, or those started by highly regarded industry veterans have always been able to attract strong talent. Women are lining up to work for Krawcheck’s boutique, Ellevest, for example, say industry insiders.

And it is hard to imagine anyone not wanting to work for Fleming as part of a brand like Rockefeller. He has Paul Myners, Jack Brennan, the former chief executive of Vanguard, and Andrea Jung, president of Grameen America and a former president of Avon, on his board, alongside Rockefeller family members.

Indeed, he has already hired two teams out of UBS in Atlanta that managed a combined $2.2 billion for their former employer, and persuaded Chris Randazzo to leave his role as the chief information officer for Morgan Stanley’s global wealth and investment management business to run Rockefeller Capital Management’s technology.

Syz makes the point that working closely alongside other families brings an expertise that larger firms even with specialist teams cannot replicate.

“When it comes to investing, it’s beneficial to have people working with you that bring generations of experience with them” he says.

The case for brand being key to success can also swing both ways.

As Gorman points out, for the scale players: “If clients see a physical presence, they know it’s a brand that has been around a long time and it gives them comfort if markets become choppy.”

One banker argues that brand can get you through reputational blows that small firms just would not be able to handle. However, the specialists counter that their high-touch model, deep relationships and less risk of reputational blows, offers the comfort clients want.

Drive

What is driving the arrival of the specialists? Revenue pressure and a need to decrease costs are putting larger managers at risk of becoming commoditized offerings and creating potential employee and client dissatisfaction.

Wealth management revenues at the largest firms by AuM have been trending upwards over the last five years, and the share of revenues that wealth management divisions contribute to their overall banking group are higher, but pressure is mounting.

|

|

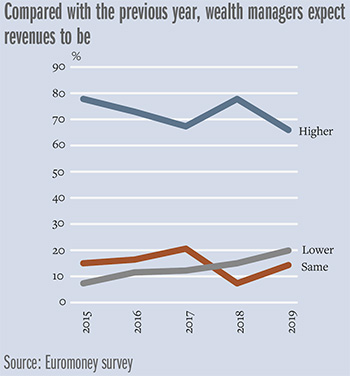

Euromoney asked private bankers for their revenue expectations for 2019 compared with 2018. While 66% of more than 1,500 respondents say they expect this year’s revenues to be higher, that expectation is considerably less bullish than last year, when 78% of respondents anticipated higher revenues. At the same time, 20% of respondents say they are expecting lower revenues this year – the largest proportion of respondents in five years.

“The whole industry is under spread compression,” says Citi’s Charrington.

The transformation of private banks into wealth management firms in this century means the industry is subject to the same pressures pure asset managers face: greater transparency through regulation and the introduction of low-cost digital offerings have forced fees downwards.

A report from PwC last October, for example, showed global mutual fund fees in both active and passive funds dropped 14.3%, from 0.52% in 2012 to 0.44% in 2017. By 2025, the consultancy group predicts a further 19.4% fall. Global alternative management fees are also predicted to continue their decline, dropping between 13.1% and 16.4% by 2025.

Revenues as a percentage of AuM also declined by 10.4% between 2012 and 2017 and are expected to decrease by 22.4% by 2025. That means wealth managers need to increase their AuM at a faster rate than they have been doing in order to keep revenues growing. As the bull market comes to an end, an AuM boost from market gains cannot be relied upon, which leaves acquisitions as the only option left. The problem is no one is selling – yet.

Ray Soudah is chief executive and founder of MilleniumAssociates in Switzerland, which advises on M&A in the global wealth management sector. In his firm’s survey of wealth managers at the end of last year, he says none said they wanted to be sold: “The appetite to acquire is there, but the targets just aren’t right now.”

Indeed, acquisitions have been relatively small. BNP Paribas Wealth Management recently bought ABN Amro’s Luxembourg business and Raiffeisen’s Polish business, points out co-chief executive of the business, Sofia Merlo.

Martin Blessing, co-head at UBS Global Wealth Management, mentions his firm’s acquisition of Nordea’s Luxembourg private banking business.

Soudah thinks that profitability challenges will eventually come to a head, resulting in some large mergers in the next decade.

“The banks are now well capitalized, but with cost-income ratios averaging around 75%, there is little revenue cushion,” he says. “I look at Julius Baer, Lombard Odier, Vontobel, Deutsche PWM, Pictet, UBP, Safra, EFG… we could see some long-standing names join forces or be bought up by the largest wealth managers.”

That is not going to happen until the prices are right.

As an industry we’ve stopped competitive hiring, and it’s clear that some of the larger firms will be reducing headcount in the next couple of years. Our goal is to grow – Andy Sieg, Merrill Lynch Wealth Management

Naratil says building partnerships to improve product distribution may be more palatable for the larger firms at the moment.

On the other side of the equation, costs have increased. It is largely the result of compliance. Some 57% of Euromoney’s survey respondents say they are investing more in compliance in 2019 than 2018. And a survey of senior staff at asset managers, brokers and banks by professional services firm Duff & Phelps in 2018 found that one fifth of firms expect to spend 10% of annual revenues on compliance in 2023. It cannot be avoided – in part because regulation requires it and in part so too does reputation.

“If you have scale and no compliance problems, or you have focus and no compliance problems, you stand a chance,” says Citi’s Charrington. “You cannot risk not being on top of your compliance and ethics because to put issues right today is very, very big money.”

Baer says he has seen the back to front office ratio at about seven to one in many large firms – it is worse for firms with legacy businesses.

“Some banks have clients who were onboarded in the 1970s and 1980s who might not meet today’s requirements, and they are having to re-document every single client. The paperwork is immense,” he says.

For new firms, compliance will be as expensive, but the complexity will be less, he argues. “We get to pick our clients and document them efficiently.”

Cracks

The cumulative effect of falling revenues and increasing costs is causing cracks to appear in wealth management firms. Baer says he has noticed an increase in fees on custody to compensate for lower investment management fees, for example. He also says some client segments have suffered.

“If you have $100 million, you’re going to be treated well because you’re highly profitable,” he says. “If you have $30 million, however, that service is not guaranteed. We hear often how clients with $30 million have to wait months to get approved for financing because their bank’s client committees only meet once a month.”

Service levels at wealth managers may suffer further as firms resort to mass layoffs as a means to cut costs, increasing the number of clients per remaining adviser.

Soudah says he anticipates the wealth management industry will “fire thousands of people” over the next few years. Yet 59% of Euromoney’s survey respondents say they intend to increase the number of advisers in 2019.

“They all say that,” says Soudah. “But if you keep an eye on the numbers in the earnings, you’ll see.”

Andy Sieg, head of Merrill Lynch Wealth Management, expects to continue to grow the advisor workforce over the next few years by leveraging Bank of America’s global training and development programmes, rather than recruiting from other firms.

“As an industry we’ve stopped competitive hiring, and it’s clear that some of the larger firms will be reducing headcount in the next couple of years,” he says. “Our goal is to grow.”

Andy Sieg, head of Merrill Lynch Wealth Management

Headcount

Sieg says Merrill is recruiting from internal employees to increase the number of its advisers.

For those considering reducing headcount, Soudah says that they would maintain better levels of service at lower cost by taking the more difficult route of cutting 30% of salaries rather than 30% of jobs.

The inevitable impact on clients of reduced headcounts and the commoditization of service is going to make them question what they are paying for, says Baer.

His counterparts at larger banks agree that value for money is going to dominate conversations over the next few years, because as Boris Collardi, the former head of Julius Baer who joined Pictet as a partner last year, says: “As the large managers got bigger, they didn’t necessarily get better.”

In 2005, it would have been hard for us to think about doing what we’re doing – to be able to compete on platforms and processes with a large firm. Now you do not need scale to be competitive on technology – Greg Fleming, Rockefeller Capital Management

Private banks are going to have to prove they add value, says Victor Matarranz, head of Santander Wealth Management. Santander is focusing on connecting its corporate customers to its wealth management platform, mimicking a merchant bank.

“We are a corporate bank in southern Europe, the UK, Latin America and in the US – that can be a value proposition for us if we can get the connectivity right with wealth management,” he says.

More will likely follow suit. Entrepreneurs after all are seen as the segment that will offer the most growth. There is a reason merchant banks are popping up.

The trick is identifying segments where value can be added for clients and matching that with profitability. A 2018 study of advisory firms by TD Ameritrade found the median operating profit margin for target-focused firms was 18% higher than others and the median annual client growth was 35% greater.

Iqbal Khan, CEO of international wealth management at Credit Suisse, says his firm is looking to segment clients based on what they are willing to pay.

“Clients are only going to be willing to pay for quality advice and they won’t be willing to pay for transactions at all,” he says. “The transparency is now there for them to make those value judgments.”

Iqbal Khan, CEO of international wealth management at Credit Suisse

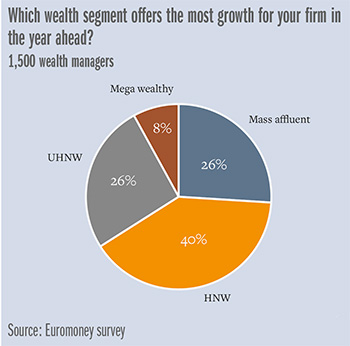

He highlights the $5 million to $30 million segment, agreeing with Baer that these clients could be served better, and adds that they could be a large revenue driver for banks that figure out how to do so efficiently.

|

|

Indeed, 40% of respondents to Euromoney’s survey noted the $5 million to $30 million segment as offering the most growth for their firm. It makes sense. The upcoming generational transfer of $30 trillion in wealth, for example, is going to create wealthy clients predominantly in this segment.

Wealth managers, however, just have not understood how to make this segment work it seems.

“Banks are going to have to find an economic model that allows them to provide a high level of service to this segment – and scale is going to help,” says Khan. The growth potential is there.

“This segment represents roughly a third of our clients’ assets,” he adds, “and last year we grew these assets by low single-digit percent, while growing the top segment by double-digit percent. It will be one of our focus points for the next three to five years.”

Khan mentions some specific initiatives the bank is working on to build revenues in this segment, ensuring that relationship managers can focus either on ultra-high net-worth clients or fully dedicate their time to this mid-tier segment, rather than having to cover both.

Credit Suisse also plans to further connect clients digitally.

“We introduced several initiatives in the $1 million to $5 million segment that worked to improve efficiencies and that we can adapt more broadly across the bank,” Khan says.

For other banks the $1 million to $5 million segment in domestic markets may be the preferred revenue route. They have left it late as digital advisory firms such as Betterment, Nutmeg and Fineco have already captured market share, but several have introduced robo-advisory platforms of their own. It will improve efficiency, freeing up advisers to target new clients and lightening the load of advisers serving the segment above.

|

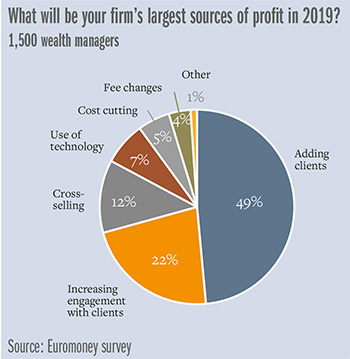

Almost half Euromoney’s survey respondents say that adding clients will be their largest driver of profits for the year ahead.

Focus

Focusing on specific areas such as corporate banking, private deals and sustainable investing could also become a value proposition for banks and enable them to compete with the specialists. UBS, for example, is regarded as a leader in sustainable investing in wealth management and is growing its offerings there. (UBS ranks first globally in ESG in this year’s survey.)

JPMorgan Private Bank has Morgan Private Ventures, says Brian Carlin, chief executive of JPMorgan Wealth Management Solutions. It serves 1,000 family offices and individuals that are qualified to be treated as quasi-institutional investors; they get exclusive direct access to deals coming out of the firm’s alternative investment partners and the investment bank.

Some large players are focusing on specific geographies. Société Générale Private Banking, for example, pulled out of Asia and has spent the last four years deepening its focus in France, where it is now in 80 cities.

“We refocused and redeployed – that was not an easy decision to make in such a growing market like Asia,” says Jean-François Mazaud, who heads the business. “But if the market isn’t delivering value to you or your clients then it’s best to leave it to a partner that will.”

The focus paid off he says, with “good profitability in the bank’s domestic market, even in a challenging year such as the last.”

Barbell

What does this mean for the competitive landscape in wealth management in the decade ahead? The long-discussed barbell that has occurred in other financial industries may come about.

“It’s going to be the largest global wealth managers at one end, and they’ll need to find the new efficiency curve to deliver their products and advice more cheaply and in a more streamlined way,” says Zeltner. “The effect of which will create room for boutiques and specialists where people will want more sophisticated advisers and deeper relationships.”

Low barriers to entry afforded by third parties will allow for their emergence.

“Large firms need their internal proprietary systems and processes, small players don’t,” adds Zeltner.

Technology costs have come down so much that boutiques are no longer at a disadvantage.

Fleming at RCM says: “In 2005, it would have been hard for us to think about doing what we’re doing – to be able to compete on platforms and processes with a large firm. Now you do not need scale to be competitive on technology.”

Will these specialists take business away from the largest firms? One banker points out that Evercore started as a specialist and is now in the top 10 in the M&A league tables. Another counters by saying there are many hedge funds that launched and failed.

However, Soudah points out that the emergence of specialists could be an opportunity for large wealth managers. If they are smart about developing business-to-consumer (B2C) offerings, they could end up being service providers of choice to some of these specialists, he says. Credit Suisse is setting up a B2C business in Asia, for example.

And in Europe, Lombard Odier has a B2C technology offering.

“We clone our own systems and can make them available to other local and international partners,” says Patrick Odier, senior managing partner at the Swiss wealth manager. “There’s a lot of innovation that happens at established firms that could become a business – such as developing reg-tech functionalities and making them available to emerging players.”

Working with family offices is the most obvious example of how banks have already managed to stay relevant to specialists. Blessing at UBS says the bank’s research shows family offices are actually increasing the number of banks they do business with as their families become increasingly global.

It is the banks in the middle that stand to lose the most. And Société Générale’s Mazaud says the middle can be defined as “not being there for any clear-cut reason.”

Santander’s Matarranz agrees: “If you’re in the middle with a plain vanilla proposition, it’s hard to see how you’ll survive.”

Citi’s Charrington offers food for thought about the future.

“I would think a lot of banks are going to fail in the next decade, particularly those in the middle who racked up high cost-to-income ratios going all in on Asia,” he says. “And with high expense ratios, it will be hard to survive if you’re neither a good boutique nor a large bank.

After all, “these costs aren’t going anywhere but up.”

The rise of the family office

In Euromoney’s 2019 annual private banking and wealth management survey, the popularity of multifamily offices (MFO) is clearly shown.

Northwood Family Office, a Canadian MFO ranks first for best private banking services in Canada, above RBC Wealth Management. In North America, it ranks sixth alongside scale players such as Morgan Stanley.

In just five years, Northwood has more than doubled its clients, staff and total client net worth, and now manages over C$4 billion ($3 billion).

“Families of wealth are increasingly looking for holistic management of their affairs, the personalized service of a boutique firm and the impartiality and objectivity of an independent adviser that doesn’t sell products,” says the firm’s chief executive, Tom McCullough.

Northwood provides global access to its client families through its membership in the Wigmore Association, an international alliance of independent family offices.

MFO appeal

New MFOs are also emerging out of the big wealth managers, like Frank Ghali, who oversaw $10 billion in client assets at Goldman Sachs before leaving to set up his multifamily office Jordan Park in 2017.

Another who knows the appeal of multifamily offices is Rob Elliott. He joined Bessemer Trust when it was managing $1 billion for the Phipps family in 1975 and was charged with opening the doors to other families. By the time as senior adviser in 2014, the firm served 2,500 clients and had $65 billion in assets under management.

“The MFO is really the best alignment you can have with your adviser: knowing that the firm is exclusively focused on handling a small number of very substantial families,” he says.

Today he sits on the board of Market Street Trust Company, a family office co-op that pools costs to keep them low, while maintaining its exclusive focus. All profits are reinvested.

Single family offices have also become more popular in recent years. According to research from UBS and Campden Research, 37% of family offices (of those 311 surveyed) have been formed since 2010.