You know a currency is heavily managed when a mere 0.6% year-to-date fall against the dollar – and a plus 1% fall over three days – is sufficient to trigger global shockwaves. But for levered investors, positioned for a one-way bet on the currency, the fall – taking place in the final three trading days of last week – has proved disruptive, especially after January’s appreciation and bullish USD sentiment.

Theories – technical, macro and political – abound for the recent fall. Some reform bulls argue markets have entered a new era of a more liberalized Chinese currency.

However, others say it’s unclear whether the recent intervention in the onshore spot rate is a direct sign that a structural widening of the exchange-rate band is on the cards, as it could simply be an attempt to realign onshore and offshore rates, and reduce speculative positioning.

On the drivers for the depreciation, Credit Suisse isolates three reasons:

“[Firstly] the government tends to pause appreciation during periods of weaker growth.

“[Secondly] we believe the government is trying to create uncertainty about the direction of the fix in order to drive an unwinding of the still large speculative short USDCNY position in the market, particularly by Chinese corporates.

“What makes this effective is that the recent slowing in the Chinese economy makes credible the idea that the Chinese government might want to depreciate the CNY to support growth. An unwinding of the position in response to the change in behaviour of the fix would be similar to the experience in H1 2012, in our view.

“The benefit for the government of this would be a reduction of capital inflows and FX reserve accumulation.

“China’s stock of FX reserves grew 15% in 2013, with an estimated $140 billion FX reserves accumulated alone in Q4. Much of this was the counterpart to speculative inflows by Chinese corporates arbitraging the difference between onshore and offshore spot and interest rates.

“[Thirdly] the PBoC may also be working to create room to appreciate the CNY ahead of US president Obama’s visit in April.”

By contrast, since May, Lombard Street Research has held the contrarian position that the renminbi is, in fact, overvalued by 30% on a trade-weighted basis, citing, in part, rising unit labour costs and disinflationary pressures.

The renminbi’s over-valuation, the shop argues, has helped to trigger a looming debt crisis, contributing to the EM rout. Accordingly, the shop argues the renminbi’s likely continued fall presages disruptive rebalancing for the economy, which would trigger global market gyrations.

It’s worth quoting the outlier opinion in full:

“Current-account inflows and capital inflows were buoyant in the second half of 2013, which pushed the yuan higher. Beijing’s commitment to financial market reforms has led investors to conclude that the yuan could only rise from here. This is wrong in our view. A stronger exchange rate would crush real GDP growth, which, even assuming a 5% depreciation of the yuan this year, is likely to fall below 5% unless policymakers go back on reforms and pump up the economy again.

“The People’s Bank of China (PBoC) has now started to put the brakes on the rise in the yuan. But once the currency stops climbing and output growth clearly moderates, capital inflows could easily reverse, as happened in 2012. The current-account surplus is now much lower than a few years ago, turning capital flows into a key driver of the yuan. A large net outflow of capital, which is also the most likely outcome if the authorities ease capital controls, will push the currency down, helping export growth and widening the current-account surplus.

“But a lower yuan and higher domestic interest rates will help rebalance growth towards consumer spending. At the moment, China has the worst combination of interest rates: high real lending rates and low real deposit rates. If real deposit rates increase, Chinese households, which are large net savers, will enjoy a substantial boost to income and wealth. This in turn should also lower their savings rate.”

However, Lombard Street Research remains in the minority camp. Most Chinese growth forecast imply Beijing will engineer a balance between the short-term need to achieve growth targets with the medium-term bid to orientate the economy into a consumption-driven model.

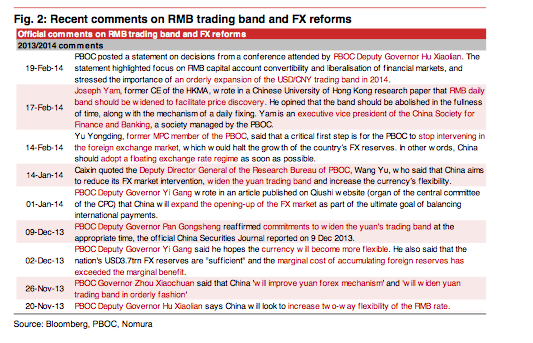

The most interesting question for many analysts, therefore, is whether the past few days herald a new currency order: greater two-way volatility. The former PBoC monetary policy committee member Yu Yongding told this reporter in May 2012 that China should allow its currency to rise or fall by as much as 10% a day against the dollar – a tenfold expansion of the typical trading band – to help liberalize the exchange rate, while capital controls and the orderly setting of the central rate would reduce domestic trade tensions.

Nomura reckons a new USD/CNH trading band has now probably arrived, given the PBoC’s avowed commitment for the policy this year, while events have forced Beijing’s hand, principally the March 5 National People’s Congress, and forthcoming political pressures in April, including the visit to China by Obama, the US Treasury report on China’s FX regime and the IMF spring meetings.

Credit Suisse, however, is not so sure. “Many in the market have argued this intervention in spot is a precursor to band widening,” it states. “We don’t rule this out, but struggle to have confidence that the intervention is a clear signal.

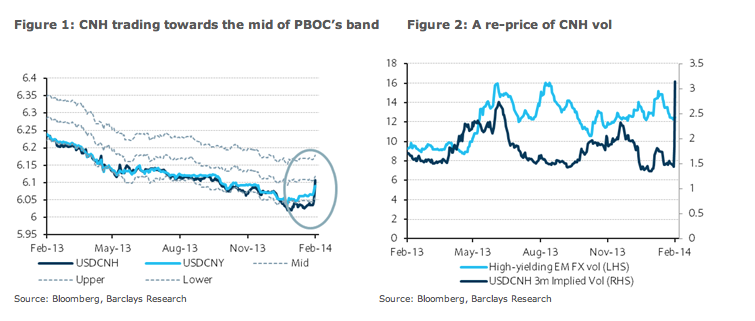

“The government pushed the spot close to the middle of the bands towards Q4 last year, but did not widen the bands as we then expected. We forecast a 1% widening of the bands this year, but have little clarity about timing even now.

“To be sure, we continue to believe that the trend in USDCNY this year is down and expect the spot rate to trade 5.95 to 5.96 or lower by year-end. We stress that we do not see the recently higher fixes as the beginning of a policy-driven depreciation of the CNY.”

On the latter point, however, as noted, Lombard remains bravely contrarian.