Illustration: Kevin February

When Goldman Sachs reported disappointing third-quarter results in October – with earnings per share down 15% from the first nine months of 2018 – executives at a firm renowned for its equities franchise had to explain some embarrassing failures in its securities and lending division.

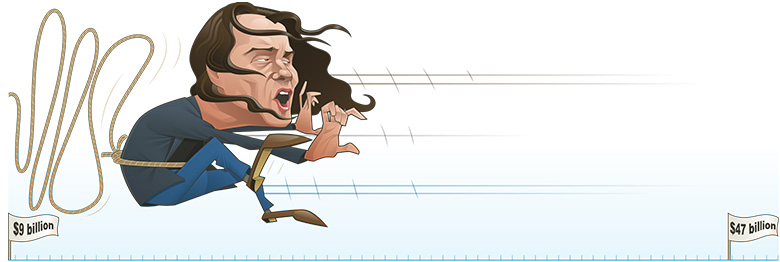

Goldman suffered losses of $267 million on retained positions in recently listed public stocks, notably Uber, Avantor and Tradeweb, which together make up 40% of its $2.3 billion public investment portfolio. It also took an $80 million markdown on its private equity investment in the We Company, the serviced office business formerly known as WeWork.

We had to pull its IPO in September when public market investors refused to provide more cash at anything close to the $47 billion valuation established in its most recent private fundraising round in January this year. The failed IPO arrangers, led by JPMorgan and Goldman, could not get a deal out of the door that valued it at even close to $20 billion.

As Euromoney went to press, news was breaking of a rescue deal. SoftBank will accelerate an earlier announced $1.5 billion investment in WeWork at $11.6 a share and swap its interests in joint ventures outside Japan into WeWork shares at the same price. It will also offer to buy up to $3 billion of stock from other investors, including founder Adam Neumann, at $19.9 per share and aim to reach an 80% ownership of economic interests in WeWork, although not with that level of voting control.

With the equity injection done and the tender complete, WeWork will then provide $4 billion of debt facilities.

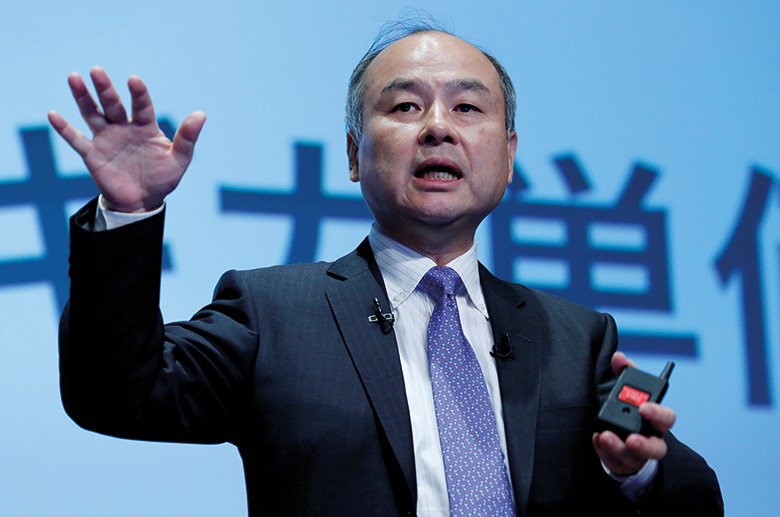

Masayoshi Son, CEO of SoftBank Group

“It is not unusual for the world’s leading technology disruptors to experience growth challenges as the one WeWork just faced,” says Masayoshi Son, chairman and chief executive of SoftBank Group. “Since the vision remains unchanged, SoftBank has decided to double down on the company by providing a significant capital infusion and operational support.”

WeWork is not a technology disruptor. It signs long-term leases for commercial real estate, spends heavily to tart offices up and then rents them short term to freelancers, startups and larger companies.

Its IPO didn’t go ahead because investors saw $47 billion of long-term lease commitments set against just $4 billion of rental income and a group of arranging banks that wouldn’t commit to providing the issuer they were supposedly sponsoring with credit lines until other people had bought equity in its IPO.

When that money didn’t come in, WeWork looked set to run out of cash worryingly fast.

The company may now survive. SoftBank will lower the average price of its enlarged stake. But bankers not working directly on the rescue deal suggest it values WeWork at well below $10 billion, probably closer to $8.5 billion on a pre-money basis.

That’s a stunning fall.

Public market investors see a great deal of market capitalization being created before the IPO and realize that waiting to try and establish a position might not be the best option – Keith Canton, JPMorgan

On its earnings call, Goldman said that it is still in the money on its $70 million equity position in We, having averaged in early enough to obtain a sensible valuation – a low basis, in the parlance. But investors were left wondering what happens should the SoftBank rescue deal stumble and WeWork runs out of cash, and asking what the mark down says about the rest of Goldman’s $20 billion portfolio of private equity investments.

Presumably Goldman was claiming the We stake was worth $150 million a few weeks ago. The failed IPO may well mark a sharp and sudden turning point for the flow of both public and private capital into maturing but still unprofitable growth companies. Could the same sudden and dramatic losses hit other positions?

These marks will come out, even if companies stay private. Lots of new buyers have been allocating to private equity capital, some more renowned for investing in listed stocks. So-called ’40 Act funds must disclose valuations in their pooled investment vehicles, including some run by mutual fund managers that have used these structures to hold unlisted equity. Most do so on an aggregate basis, but some may periodically update valuations down to the level of individual securities.

And Goldman has a double exposure. Not only does it hold large illiquid equity stakes in private companies on its balance sheet it also sources earnings from the process of private capital raising, which in recent years has quietly developed an infrastructure, largely hidden from public view, comparable to that of the public equity capital markets.

Large investment banks traditionally coin it from arranging IPOs for fees of between 3% and 7% of gross proceeds. IPOs typically make up half their ECM revenues. Secondary equity follow-ons and convertibles account for the rest.

Large private capital placements have grown a lot in recent years, not always with lead banks. Sources say that in a US primary equity market raising roughly $200 billion a year, close to 50% of that is being raised in private rounds today, up from just 25% five years ago.

Keith Canton, managing director and head of private capital markets at JPMorgan, says: “What has changed in recent years is that companies have decided to stay private for longer, and companies who are much bigger, more mature and have grown far beyond the venture stage – and have products, services and technology that are clearly proven – can now raise private equity capital to execute their growth plans.

“Public market investors see a great deal of market capitalization being created before the IPO and realize that waiting to try and establish a position might not be the best option.”

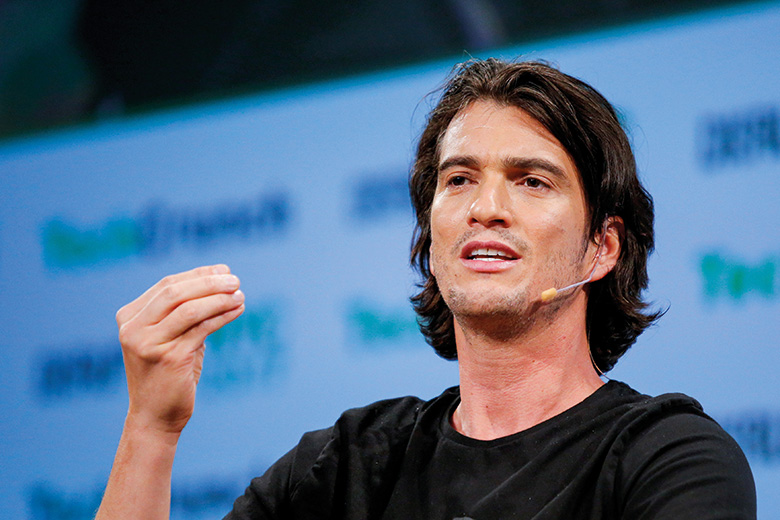

WeWork founder Adam Neumann

Late-stage deals

PitchBook counts 572 late-stage venture deals in the third quarter of 2019 alone raising over $17 billion, with 83 of these deals worth more than $50 million each. For the year to date, $41 billion has been invested in these large, late-stage deals, the second highest total ever, if slightly down on the same period in 2018.

The industry has come to call them private IPO rounds.

Private capital raising hasn’t killed the IPO market just yet, however. Banks are keen to keep the IPO machine running, especially as more follow-on deals are done as block trades with leveraged-buyout sponsors that still own the majority of stocks in many newly listed companies putting banks in competition against each other to take these down as balance-sheet risk at thin margins.

At the start of the second quarter of 2019, excitement began building over a splurge of unicorn IPOs from the likes of Uber, Lyft and We. Positioning themselves as disruptors in transport and real estate, these companies had all grown dramatically under prolonged private ownership and somehow came to be valued as technology companies. And they had – on paper – delivered eye-watering value to a small club of early backers, including venture capitalists, private equity funds, sovereign wealth funds, a few pension plans and family offices capable of deploying vast pools of capital and eager to establish large stakes in emerging growth companies before public investors get a look in.

The truth is that JPMorgan and Goldman Sachs had no chance with We. They couldn’t file an IPO valuation much below the last private round. They just had to try it on – Banker

Helping private companies access these investors is the new private equity capital markets business. Bankers count seven such deals worth $1 billion or more last year, a record for private capital raising, up from four in 2017.

Some banks have established dedicated teams to handle these placements; a few still run them off integrated ECM desks.

But while companies stay private for longer, banks have maintained their IPO businesses as well and hoped their turn to shine had come after the government and SEC shutdown at the start of the year.

Uber’s IPO in May failed to live up to expectations

By the time the fourth quarter had begun, however, capital markets participants were worrying about the impact of the We debacle, the poor debuts of Uber, Lyft, exercise bike maker Peloton and others on both the IPO pipeline and on private capital raising.

Peloton priced its IPO at the top of the range in September, establishing a valuation that was double its last private funding round. Less than three weeks later the stock was down 17%.

It appears that investment banks have lost their ability to price IPOs. The question now becomes: were the elevated paper valuations of private companies also fake news, a fantasy of wealth creation that could never be realized and turned into cash?

Is the new private equity capital market that emerged in the years after the financial crisis and seemed to be maturing into institutional-grade infrastructure over the last 18 months, broken?

There won’t be seven $1 billion or bigger private equity placements this year. There may barely be a couple.

David Solomon, CEO of Goldman Sachs

David Solomon, chairman and chief executive of Goldman Sachs, told listeners to the firm’s third-quarter earnings call: “I do think that we are going to see a rebalancing of this process of private capital formation, the size and the magnitude of that private capital formation and the period of time with respect to which people get [to] the public markets.”

Visitors to JPMorgan’s offices on Madison Avenue in October found meetings suddenly cancelled as bankers gave up whole days and weekends to devising a new funding solution for The We Company, their one-time darling now problem child.

“We will be using it to pitch against them, but the truth is that JPMorgan and Goldman Sachs had no chance with We,” says a banker at another firm. “They couldn’t file an IPO valuation much below the last private round. They just had to try it on.”

Similarly, once SoftBank had set such a high bar for valuing WeWork, other private buyers couldn’t get away from that. If they wanted exposure in late private rounds, they just had to accept it. But public market investors can figure out very quickly when a private company has been built on an inflated valuation.

“It’s not that public investors are smarter than private investors, but they are pricing based on what the next investor will pay in a liquid market,” says one ECM banker. “And when there are thousands of them seeking to establish valuation, their median calculation will be closer to being right than that of one or two big private investors who have essentially lost all discipline.”

How did we get here and what happens next?

Due diligence

No investment banker will go on the record to criticize SoftBank. Its Vision Fund is a honey pot of fees for advice and capital raising, and every firm wants its business. But the urban legend of chairman and chief executive Masayoshi Son committing billions of dollars to investing in WeWork after a meeting of minds over lunch with founder Adam Neumann is the exact opposite of how bankers say most large private capital deals come together.

The bankers all talk about due diligence.

Ernesto Cruz, managing director and chairman of equity capital markets and head of private equity solutions at Credit Suisse, tells Euromoney: “Most private equity capital raisings that we do go for consideration to investment committees at potential institutional buyers who will tear the investment thesis apart, a small handful of whom may then form a view on potential price and terms until one or two eventually come back with a deal that may just get across the line. It is absolutely a disciplined process.”

It’s important to remember that while private capital rounds have grown hefty in recent years, with large investors willing to write individual tickets worth hundreds of millions of dollars – much bigger than the average IPO – they are typically buying preferred stock with restricted or no voting control. They may have exposure to the upside and the chance to convert to common equity in an IPO, but their ability to oust founders and replace management is limited. So, due diligence is vital.

|

|

|

Holcombe Green, |

Holcombe Green, managing director and head of private capital advisory at Lazard, expands on this.

“The biggest thing that private investors want before putting money into a private company is access to substantive information,” he says.

“If you are going to back a management team, especially if you are underwriting an innovative growth play, you want clarity around strategy, the drivers of future business activity and information memoranda with substantial information about current and forecast financials.

“Very large investors will want to do more than meet the chief executive and CFO in a conference room. They will then want to diligence what they hear with site visits to data centres, warehouses, stores to verify the nuts and bolts.”

This is not so different from marketing an IPO, except that information is restricted to a small club of very large investors. Private companies can do this. Public companies cannot grant preferential access to information to select investors in the same way.

Euphoria has crept into all financial markets in a zero-interest rate world where defaults are rare and investors are desperate to find returns. Investors have stretched the limits of prudence in bond markets, loan markets, commodities, public equity and collateralized loan obligations.

While many still shrink from the complexity of leveraged structure risk they took before the great financial crisis, some have chosen to take on liquidity risk instead to earn a premium.

Leaders of the tech unicorns are good at two things: building businesses and raising money. They have their own capital raising teams and may have felt little need to use investment banks when investors were knocking on their doors begging them to take their money.

“For us, private capital raising is about sourcing investors to bring creative solutions to the regular needs of a different class of companies to the tech unicorns that grab all the headlines and already know the potential investors,” says Cruz.

For example, Credit Suisse arranged a deal for waste management company Advanced Disposal Services in 2016. The company had been targeting a $400 million to $500 million IPO, but it was highly leveraged at 5.2 times ebitda with Ontario’s OPTrust holding preferred shares that would not convert to common stock in the flotation but rather had to be redeemed.

Pre-IPO capital raises present an interesting and exciting opportunity for investors and companies that differ from IPOs in that there is no research involvement or near-term liquidity – Douglas Adams, Citi

As markets became volatile during a risk-off phase, ADS pulled its IPO. In August 2016, Canada Pension Plan Investment Board (CPPIB) invested $280 million in convertible preferreds; these redeemed the OPTrust securities while converting to common at the IPO. It thus delevered the company.

In October 2016, ADS got its $347 million float away. CPPIB paved the way for the IPO and came out of it owning 20% of the listed company.

Specialist private equity capital groups are working away on lots of these medium-size and intricate transactions.

|

|

|

Douglas Adams, |

“Pre-IPO capital raises present an interesting and exciting opportunity for investors and companies that differ from IPOs in that there is no research involvement or near-term liquidity,” says Douglas Adams, global co-head of equity capital markets at Citi. However, he points out “the outcomes can be uncertain.”

Of course, IPOs are also a long process, but there are recognized checkpoints along the way. On a private deal, bankers can do a lot of work and then, for whatever reason, it doesn’t happen. Bank arrangers also have to be wary of negative selection.

“There are both formal and informal engagements for private company capital raises, but we have to be disciplined on which ones we take on,” says Adams. “Many deals are done without advisers, so you have to be careful where companies have tried to raise money on their own and struggled.”

Behind the scenes

A lot is going on behind the scenes. In the last 18 months, banks have increasingly been working on series D, E and F rounds, preparing the way for an IPO and debating with companies how best to control widening private share registers in the run up to flotation. But it’s still the likes of Uber raising over $1 billion at a time from SoftBank and driving its private valuation up towards $68 billion early in 2018 that grab all the attention.

“We get issuers telling us they have in-bound queries from investors from China to Singapore to Canada, and sometimes they are raising money without using investment banks,” says a senior capital markets banker. “I’ve had issuers tell me they’ve taken money from a couple of investors that gives them a valuation of $3 billion and that they are really happy because a year ago they were valued at $500 million. They sometimes don’t seem to see that that comes at a cost. How do they then generate a return for those investors when that new capital already values them at 30 times revenue?”

Financial markets are always more about supply and demand than fundamentals. There’s been an awful lot of money hoping to take big stakes early on in the next Facebook or Amazon. Recent failed deals raise fears over a new tech bubble burst, reminiscent of the internet bubble that popped 20 years ago. But late-stage venture investors continue to put money to work. Like private equity sponsors, they have a lot of dry powder to use.

I don’t think recent problems with valuations will impact the willingness of large institutional investors to invest directly in private companies, unless those problems become widespread – Holcombe Green, Lazard

In late October, Databricks, provider of a cloud and machine-learning based platform for large-scale data engineering, raised $400 million in a series-F round led by Andreessen Horowitz’s Late Stage Venture Fund and supported by new investors, including funds managed by BlackRock, T. Rowe Price and Tiger Global Management. It values Databricks at $6.2 billion.

This is a company that has grown from no revenue to a $200 million annual run rate in less than four years. Back in February 2019, Ben Horowitz, co-founder and general partner at Andreessen Horowitz, announced: “Databricks is the clear winner in the big data platform race.”

The company had just raised $250 million in a series-E round, also led by Andreessen Horowitz, which then valued it at $2.75 billion.

Almost more impressive than its revenue growth has been the more than doubling of the unicorn’s valuation in just over eight months.

Bankers recount conversations with venture capitalists ready to write $100 million cheques for series-B funding rounds and $500 million for later rounds, as long as they can get in before companies go public. No wonder some unicorn founders have grown drunk on optimism while still managing to sound persuasive.

“There may have been situations where private companies have raised large amounts of capital quite quickly almost on the basis of reputation, with very little information delivered to investors,” says Green at Lazard. “But these tend to be the kinds of deals done without advisers. And the potential losses we are now seeing will result in it being much harder to do that kind of thing.

“I don’t think recent problems with valuations will impact the willingness of large institutional investors to invest directly in private companies, unless those problems become widespread. There has been a substantial illiquidity premium on offer, and institutions seeking returns will continue to let long-term capital run in private hands.”

But what if struggles to maintain the credibility of private-market valuations do become widespread?

Misvaluation

The problem with the argument that WeWork and a few others are isolated examples of misvaluation is that the marginal investor that seems to have lost discipline, the SoftBank Vision Fund, is also the biggest investor in the private capital market.

And the knock-on effect of other private investors submitting to a misvaluation in order to secure a big position in what they hope will be a winning company, is that misvaluation plays out across a still small club of very large buyers.

It seems to be blessed by the entire investing community.

“The private investor ecosystem is evolving rapidly, but it is still small relative to the public market,” says Adams. “To an extent, that ecosystem feeds on itself. Investors may seek co-investors and introduce each other to companies, which is very different to the book-building process of an IPO.”

There have been maybe a couple of dozen large private investors driving this.

The establishment of a new high valuation through a late-stage round becomes an event on which earlier investors, like SoftBank, mark up the value of their previous investments. There may be no liquidity to cash these positions in, but they sure look good on paper, making executives eager to sign off on more such stakes and investors desperate to throw cash at minority positions in unlisted companies.

Delusion sets in.

“This private capital market is fast evolving,” says one banker. “And if you see your valuation go from $17 billion, to $27 billion, to $37 billion, to $47 billion with each passing round, it’s easy to lose sight of the fact that you cannot simply take those private valuations and apply them to the public market. It probably never even occurred to Adam Neumann that he wouldn’t be able to go public at well above $47 billion.”

The WeWork example is clearly a case study of hubris and perhaps even abuse of process. But is it a sign of just one or two high-profile private investors losing price and value discipline, or of the whole market taking leave of its senses?

|

|

|

John Collmer, |

John Collmer, head of private capital markets Americas at BofA Securities, says that most private equity capital investments proceed after detailed due diligence and it would be a mistake to assume otherwise from a few recent problem IPOs for tech unicorns.

“These investors know the technology industry really well and have successful track records financing growth of established private companies, especially those that have a differentiated product or service unlike any available in the public markets,” says Collmer.

“They have sophisticated teams to do due diligence, which can take several weeks to conduct. In confirmatory diligence, sophisticated private investors are hiring outside consultants to conduct additional diligence around accounting, tax and market consulting.”

But here’s the thing. Private investors in growth companies, including a rising number of cross-over mutual funds, are more concerned with identifying winners and placing big bets than with valuation. They will, in the parlance, lean in on valuation.

“The price or the valuation from one financing round to the next doesn’t actually matter to these investors as long as the company succeeds in the long run,” says one banker. “Buyers are competing for these opportunities. By the time companies go public, arrangers are building big books with modest allocations to many investors. Increasingly, institutions in the private market would rather put $100 million down even at a valuation where they only make three times their money, rather than at a valuation where they can make 10 times their money but can only put $10 million or $20 million to work.

“What they talk about most is their bet sizes.”

A banker at another firm picks up the topic.

“My sense is that in some deals investors have been saying: ‘I’m not sure it’s worth the metric, but it’s a good company, so maybe I’ll buy in and wait for it to grow into its valuation,’” he says.

It is only when companies do finally go public that fine judgements on valuation come into play. This banker says: “That is when companies transition into the hands not of growth equity investors but rather the ‘growth at a reasonable price’ investors.”

Change in investing

Why has so much money been pouring into minority stakes in unlisted companies at over-optimistic valuations?

It is partly because of the belief that something much more profound than the internet tech bubble of the late 1990s is playing out.

Yes, it is a bit of a joke that companies in consumer retail, minicabs, health and fitness or serviced offices should position themselves as tech companies just because they have websites and apps to send training plans to your exercise bike or to find the nightclub you’re swaying outside.

But technology is transforming many sectors – media, energy, autos and financials.

“To change any industry in the way Amazon changed retail requires a lot of capital,” one banker points out.

Investing has changed too.

The rise of low-cost, passive exchange-traded funds and consolidation among asset managers have forced active mutual funds to search for new ways to outperform the indices. And one way to do that is to make large allocations to unlisted companies before they go public.

We used to say that to be in the IPO, you had to have been in the LBO. But today it is no longer just LBOs that drive IPO issuance – Paul Abrahimzadeh, Citi

Explaining the growth in the number of investors and volume of capital now chasing equity stakes in unlisted companies, Green also sees a link to the poor returns of many hedge funds in the aftermath of the financial crisis.

“Institutional investors have reduced allocations to liquid alternatives because on average hedge funds have underperformed,” he says. “The private company ecosystem has filled that void.”

IPOs are not separate from private capital raising; rather they are the moment when private valuations are tested. This is where the signs emerge that something has gone wrong.

Nashville-based SmileDirectClub listed at $23 at the start of September, valuing the company at close to $9 billion. One month later, shares in the teeth-straightening dentistry disruptor were 60% down, making it the worst performing unicorn IPO of the year.

“When your IPOs go down 50% or so, that’s when buyers go on strike,” says one ECM banker. “This was a company that somehow got valued with a tech multiple when it should have been at a retail multiple.”

Yes, there have been winners too. Food technology firm Beyond Meat priced its IPO at $25 in May, saw the shares rise above $230 in July, priced a secondary offer at $160 in August and was trading back at $122 in the middle of October. It’s a captivating story.

But such wild price movements are disconcerting. IPO buyers have traditionally reasoned that new stocks should be priced at a 10% to 15% discount to fair value to provide some return and compensation for the risk of buying into still young companies.

An 860% rise in two months looks less like a pop, more like a mispricing. In its own way, it’s almost as troubling as SmileDirect’s 60% fall.

In recent years, the average IPO has outperformed the S&P500 by between 300 and 500 basis points. But this year it has tracked the S&P500. And if you market-weight that analysis, the return comes down because some of the largest IPOs have been the poorest performers.

These failures have been set up by the late rounds of private capital raising.

Change in IPO candidates

Some private companies have been able to raise from $500 million up to $1 billion at a time in late stage private rounds, compared with a median US IPO of perhaps $120 million, or closer to $170 million if you exclude small biotech IPOs.

It is not just that private investors are a new source of demand for investment opportunities. The supply of companies that might one day IPO has also changed.

In the run up to the financial crisis and the years that followed, the vast majority of IPO candidates came from the portfolios of private equity sponsors that owned companies outright.

From the 1980s onwards sponsors had taken companies private when multiples were low, borrowing against their assets and cash flow to do so, and then floated them again during stock market booms.

Sponsors claim to reengineer companies away from the public gaze, but in reality most just attempt to time the market.

|

|

|

Paul Abrahimzadeh, |

“We used to say that to be in the IPO, you had to have been in the LBO,” recalls Paul Abrahimzadeh, co-head of equity capital markets at Citi. “But today it is no longer just LBOs that drive IPO issuance. Venture-backed companies are a prolific IPO contingency, and, as bankers, to be in the IPO you usually have to become important to these companies during their private funding rounds.”

Sponsors such as KKR, Carlyle, Blackstone and Apollo have established dedicated funds that take minority positions in private companies, usually financing their growth phase after angel investors and first-round venture capital funds have seen innovators through the process of turning a business plan into an actual company with a viable product or service.

“These dedicated funds for minority investments at the largest alternative asset managers are few in number but very significant in size,” says Cruz. “They can each write a cheque for $500 million when you bring them the right deal.”

Besides these, other institutional investors are now allocating increasing sums to direct investments in unlisted companies.

|

|

|

Joseph Cassanelli, |

“Pension funds are increasingly demanding co-investment rights and hiring to enhance their capabilities to do more direct investments,” says Joseph Cassanelli, managing director and co-head of financial institutions North America at Lazard.

Issuers like such committed long-term investors on their registers that do not have to monetize assets to return cash to limited partners in funds with a defined maturity.

“Private companies (sellers) are viewing them positively given they are, if not permanent capital, often longer-term holders when compared to private equity funds that may have to sell positions after five years,” explains Cassanelli.

Sometimes a pension plan that has committed a large sum to a buyout fund will negotiate co-investment rights to invest alongside the general partner, piggy-backing off its due diligence without paying full fees.

Increasingly, if also quietly and carefully, the investment analysts hired by these pension plans are competing with the general partners for investment opportunities.

Sovereign wealth funds (SWFs) are another big and growing pool of capital for direct investment in private companies. Saudi Arabia’s Public Investment Fund was the biggest backer of the SoftBank Vision Fund.

Asian SWFs, including GIC and Temasek from Singapore and Malaysia’s Khasana Nasional, were cornerstone investors in the largest-ever private equity capital raising of $14 billion for Ant Financial in June 2018. Abu Dhabi Investment Authority has built up an in-house team to source private equity investment opportunities.

The large family offices of ultra-high net-worth individuals represent a third new pool of capital chasing unlisted equity, although it’s hard to establish their importance to the private capital market.

“Every bank brags about their access to these famous mega family offices that can allocate $50 million to $100 million. But, in my experience, they are very cautious about being caught up in anything like the tech unicorns and they are very disciplined,” says Cruz.

“The sweet spot is bringing an investment of direct relevance to the wealth creator’s expertise. So, the person who has made billions in cruise lines will be the right person to show an opportunity to invest in a travel industry disruptor, for example, or a fashion industry billionaire might be the right person for a consumer retail company.”

Finally, the mutual fund complexes such as BlackRock, Fidelity, and T. Rowe Price, which have traditionally delivered diversified portfolios of public equity to retail buyers, are raising dedicated cross-over funds to take stakes in growth companies before they list – as long as they intend to do so eventually. They are also taking advantage of allowances in other funds to allocate low single-digit percentages to unlisted equity.

How might all these newer investors in private equity begin to think differently about deals after recent problems?

“It is my firm belief that private capital markets are here to stay and that what we have seen in recent years is a fundamental shift in capital formation,” says Canton at JPM. “How may the private market develop from here? First, good companies will always be able to raise capital. They don’t want to halt their growth plans and our pipeline has high-quality companies still working on deals. However, investors may now focus more on valuation and terms.

“If I think of public investors in the private market, they do want to obtain more substantial allocations than they can in the IPO, as long as that also comes at a valuation that allows meaningful upside. If they do that, then they can buy at the IPO as well, establish a mark that shows the value of their earlier stage investment, and then continue to support the stock in the public secondary market and create an attractive average price across a large allocation. These are the kinds of investors companies want to attract before they IPO.”

But surely these investors will now be more focused on valuation and on deal structures?

Canton suggests that “new investors in late-stage rounds may seek seniority from a liquidation perspective. We are also hearing discussion coming up again of valuation re-sets and so-called pre-IPO convertibles, where the valuation on funds invested today can be re-set at a discount to any eventual IPO valuation.”

That sounds a bit like getting the lawyers round and signing a pre-nup before celebrating the wedding.

Canton says: “We look to avoid those features in our transactions whenever possible.”

Ultimate goal

The ultimate goal of most private company founders and certainly of their employees, who are often compensated in stock and stock options, is still to go public so as to cash out and diversify. A liquid publicly traded stock is also an acquisition currency that today’s growth companies may eventually wish to spend if they become tomorrow’s consolidators.

“We have been talking to one company that wants to do a $1 billion private equity deal, and our message to them is: ‘There are comparable listed companies trading on 20 times earnings and you are better than them. You should probably go public now because you may never see such valuations again’,” says a banker.

But public ownership comes with a certain burden of mundane reporting – investor relations teams, earnings calls and AGMs – and litigation exposure.

Some companies are staying private for longer for good reasons. A few are genuinely innovative disruptors, building new business models for their sectors and applying new technology even if they are not, at their core, technology companies.

Innovators see a competitive advantage in growing their businesses to scale in private without giving away their secrets to competitors through the full and widespread disclosure required in a public listing. Many owners also dislike the idea of subjecting themselves to quarterly public reporting that may hit the share price and so disrupt a long-term strategy to prioritize growing market position and revenue ahead of short-term profitability.

And if they can grow to scale and profitability under private ownership with committed long-term, strategic investors, many companies may simply stay private.

Some of the most creative work in private equity comes in moving ownership structures between different pools of private capital. There is a growing market in so-called secondaries, as private equity funds that mature no longer have capital to invest in their portfolio companies and wish to raise liquidity for their limited partners look to new private buyers.

Sometimes they will structure baskets of private stocks to sell on to new long-term owners, who may inject more capital into these companies before eventually looking to float them.

Cruz talks of one different example: “We have been working with a corporate services company part-owned by private equity, part by one company. The partners desire to delay taking the business public while some of the investors want liquidity, which is a challenge.

“We have taken on the challenge of searching for long duration minority capital for up to $1 billion. One year ago, I thought we might find eight-year money. We have ended up with a couple of investors willing to put up those sums as 10- to 12-year capital,” he says.

“These deals are always a challenge and can take from three to six months up to a year, but they are incredibly rewarding to work on, as the private markets become increasingly diverse and flexible.”

Potential fall-off

As WeWork limps towards its rescue equity injection, however, it remains to be seen how flexible the private and the public equity markets will be with companies that, even after they establish themselves, continue to burn money year after year with no clear path to profitability.

Some of these private companies have to go public because they have simply exhausted the supply of private capital and need a new source. Even if they appear to have built high valuations in private funding rounds, that’s not a great marketing pitch.

And the challenge becomes acute when a lot of the public-market investors that might once have bought the IPO have already crowded into the stock in private rounds.

There is now a potential fall-off in demand between the last private funding round and the IPO. Some investors may hope for an IPO pop so as to re-mark retained positions from earlier private funding rounds at higher values. But that seems to be expecting a lot. Early backers have already had their pops in subsequent private rounds.

One ECM banker asks: “Is the IPO really an IPO anymore, or is it actually a follow-on?”

Instead of being an exception, the dreaded public ‘down round’, where IPO investors put a lower value on a company than the last one or two private funding rounds, may be set to become the new normal.