There was a time when the full extent of the Abu Dhabi Investment Authority’s disclosure was arguably the world’s least revealing website. Its front page was a picture of the gleaming Corniche tower, with an address and a phone number beneath it. The viewer would look to see where to click through to find any more information before realizing that there wasn’t any more information to click through to. That was it: a tower, an address and a phone number.

|

| Adia 2013 review |

These days, comparatively speaking, Adia is the most open sovereign wealth fund in the Gulf. In July, it published its fifth annual review, in stark contrast to the stoic silence of, for example, the Qatar Investment Authority, Kuwait Investment Authority, or any of the Saudi Arabian institutions with sovereign wealth elements to them. The latest review is the usual combination of welcome insight and tantalizing absence: there is still no magic number for total assets under management, nor any gauge of year-to-year performance beyond the annualized 20- and 30-year returns. The ranges within which the portfolio can operate, both in geographical and asset class terms, are always expressed, but never the position of the portfolio today.

It is, though, now possible to discern patterns beneath the numbers. There have been two modest shifts over the years, which the fund management industry would do well to pay attention to. At first glance, they seem absurdly minor: a drop from 80% to 75% of Adia’s assets being managed by external fund managers; and a drop from 60% to 55% of Adia’s assets being invested in index-replicating strategies. But they could prove to be highly significant.

The first thing to realize is that a five percentage point drop is, in dollar terms, a mighty amount of money. Only a handful of people know how much money Adia really manages, though educated guesses tend to fall between $700 billion and $800 billion. Taking the latter figure, then a five point drop in the proportion going to external managers is $40 billion, though that’s clearly an inexact equation since the overall volume of assets will presumably have been going up.

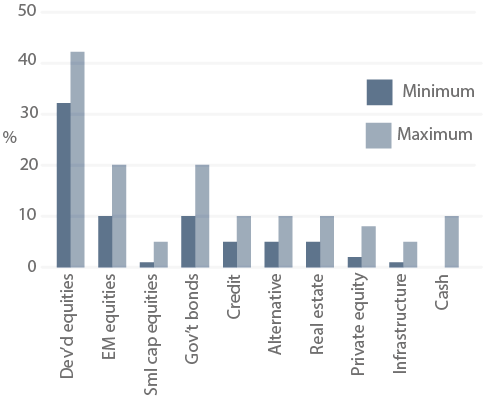

| Portfolio overview: by asset class |

|

| Source: Adia |

The more subtle and important point is that all over the world sovereign wealth funds are tending to bolster their in-house capabilities and reduce the amount that goes to external managers, and it appears Adia, from a very high base, is gradually doing the same thing too. From the Korea Investment Corporation to the China Investment Corporation, the Government of Singapore Investment Corporation to the Kuwait Investment Authority, the model is to build sufficient competence in-house to do the simple things well, then take that off external managers and ask them to earn their fees by doing more distinctive and difficult things instead.

A look at Adia’s hiring trends in recent years supports the sense that Adia wants to be smarter in-house. For some time, it has had an internal equities department alongside its external equities division; in 2013, the year under review, it recruited its first ever global head of internal equities, AllianceBernstein veteran Gregory Eckersley, with responsibility for overseeing all internally managed active equity portfolios. A new head of Asia ex-Japan, Suresh Sadasivan, from Legal & General Investment Management, was recruited to the internal equities team, while analysts and portfolio managers were added for Latin America, regional investment holdings (that is, in the Gulf) and what Adia calls ‘equity opportunities’. In fixed income, while it’s all one department, there is a growing team dedicated to internal management – a new head of internal fixed income was hired – and in alternatives, where Adia has long been considered a pioneer, a new global head of infrastructure joined: John McCarthy from Deutsche Bank, who was global head of RREEF Infrastructure there.

Passivity

The slight move away from passive management is also important. Adia has stood out from other SWFs (or at least those that disclose allocations) in this regard, in putting the majority of its money out to passive investment; the fact that a large part of this is done by external managers is also unusual, since sovereign funds tend to do the passive work themselves as it is relatively easy to do. If both the proportion of external management and the proportion of passive management are coming down simultaneously, this suggests fund managers are being asked to work harder and to perform more active roles.

There has been one other shift since Adia started publishing its review in 2009: a modest shift in the minimum and maximum allocations to certain asset classes. Where once Adia could put 45% of the fund into developed equities, now the ceiling is 42%, and it can go as low as 32%. It’s a small change, but it shows the importance Adia places on emerging markets (up to 20% of the fund can go into emerging equities) and alternatives (between them, hedge funds, managed futures, real estate, private equity and infrastructure can theoretically top out at 33% of the fund). These are perceived to be where the opportunities lie for fund-management professionals.

Adia is very clear that there will always be a role for external managers – they still run three-quarters of the fund, after all – and it continues to be the first name on the appointment list for any fund manager visiting the Gulf. There is no cause for alarm for externals, since the asset pool is so enormous. But every recent hire suggests that the fund wants to be at least as capable in-house as the external portfolio managers that serve it.

Fund managers will need to stay sharp.