|

Is the world heading towards a ‘New Normal’? Many believe that we face a future norm of low growth, interest rates and investment returns. This, it is argued, stems from the global financial crisis, which is compounding previously underestimated structural changes in the global economy.

Yet even as progress continues to be made in addressing the crisis aftermath, talk of a gradual return to normality, albeit of a new, gloomier, variety, is misplaced. The situation is far from ‘normal’. In fact, it is probably more instructive to think of a ‘New Abnormal’. This may lead to fresh surprises which force policymakers and financial markets further into uncharted territory.

Dictionaries typically define ‘normal’ as regular, usual, healthy, natural, orderly, ordinary, rational. It is hard to use such words to describe the current performance of the world economy and financial markets. Just think of the unprecedented and unconventional monetary measures that are being applied to the main developed economies in an effort to revive economic growth.

Despite zero, or even negative, interest rates and massive infusions of liquidity into the money markets and bond purchases by central banks, growth in the developed world varies from the mediocre to the barely positive. Meanwhile, while markets are partying like it’s 1999 and corporate profits remain close to all-time highs, businesses are reluctant to invest, and pay, for most workers, is, at best, growing sluggishly.

Unconventional The situation in Europe is particularly abnormal. The Eurozone’s periphery continues to struggle with mass unemployment, popular discontent and rising government debt. Despite this, their governments’ bond yields, which only two years ago were shooting skywards, have plunged, in some cases into negative territory.

Meanwhile, the euro’s exchange rate, which was bizarrely strong at the height of the Eurozone’s economic woes, is finally falling as the European Central Bank (ECB) continues on its tortuous and improvised journey of unconventional monetary easing.

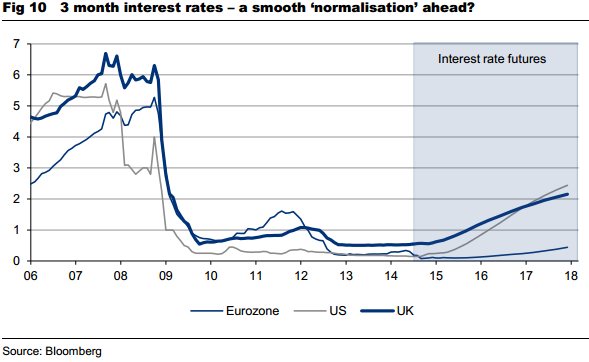

The euro’s decline is also partly due to more hopeful signs across the Atlantic. The US economy is growing moderately and unemployment is falling faster than expected. The US dollar is being boosted by talk of a ‘normalisation’ in interest rates starting next year. The consensus is that the Federal Reserve will raise interest rates gracefully and gradually to a ‘new normal’ level of 3% or 4% over the next three years.

|

Unfortunately, it is hard to be confident that the ‘normalisation’ of interest rates, starting with the US, will proceed so smoothly. We have no historical experience to guide us as to the reaction to the onset of the reversal of seven years’ worth of dramatic and unprecedented policies. Asset markets could be especially vulnerable, given that the policy tightening is coming at a point where interest rates are ultra-low and the yield premium for riskier assets is slim.

Moreover, the reaction to higher US rates is further complicated by the current policy divergence with the Eurozone, where the ECB is still in easing mode.

Severe test A sharp fall in asset prices would provide a severe test of the resilience of the financial system, which is still recuperating from the global financial crisis. Regulators have moved to strengthen financial institutions by stiffening rules on risk-taking and increasing capital and liquidity buffers. But they have been reluctant to acknowledge that such moves have restrained bank lending, responding to suggestions that tougher regulation may be curbing economic growth by saying that ‘it’s a price worth paying’.

But it is hard to escape the conclusion that the abnormal loosening of monetary policy has been partly to compensate for the effects of tougher regulation.

The good news is that many leading financial institutions have made good progress in improving the health of their balance sheets, and would be in a better position to withstand another shock. But doubts must remain about the resilience of the financial system as a whole, which has been rather overlooked by the growing tower of regulation.

Indeed, the political imperative to avoid burdening taxpayers again is transferring risks back to the markets, including less lightly regulated institutions.

Positive path

Two examples serve to illustrate the potential systemic vulnerability inspired by new regulations. One is the ‘bail-in’-able debt which the regulators are encouraging the banks to issue to boost their capital bases. While investors are now snapping them up eagerly for their extra yield, they may rush for the exit at the first sign of trouble, thereby exacerbating any future setback.

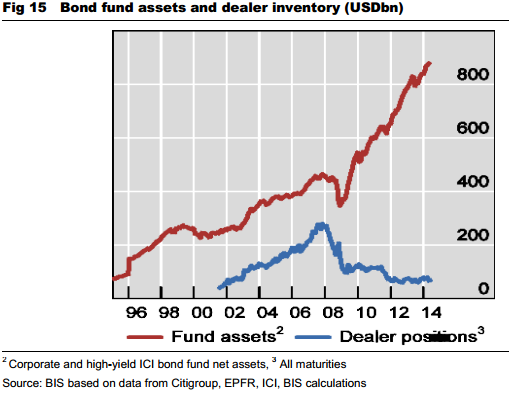

Another is the substantial reduction in dealers’ inventories of bonds, partly due to higher capital requirements on riskier bonds, which would make them harder to sell in the event of a crisis, forcing an even bigger drop in their prices.

|

This is not to say that a fresh crisis is imminent or even probable. Hopefully future setbacks in the global economy and financial markets will be minor wobbles, from which policymakers will learn and then deliver pragmatic responses that put us on a more positive path.

But it is too early to predict confidently that we are on a graceful path to a ‘New Normal’. We may have to live with a ‘New Abnormal’ for a few more years.

Click here to read the full report.

About Mark Cliffe

|