European Council president Donald Tusk (second from right) meets the prime ministers of the Visegrad Group: (from left) Poland’s Mateusz Morawiecki, Hungary’s Viktor Orbán, Slovakia’s Peter Pellegrini and Czech Republic’s Andrej Babis

|

| ECR SPECIAL |

Hungary’s Fidesz government has attracted plenty of negative headlines in its nine years in power, but looking at recent macro numbers it is tempting to conclude that its populist and unorthodox policies have had little impact on the country’s economy and its appeal for investors.

Annual GDP growth has averaged 3.8% since 2014. Last year it reached 4.9%, making Hungary the fourth-best performer in the European Union. Wage growth is running at over 10%, while net foreign direct investment has averaged 1.8% of GDP over the last five years, according to Standard & Poor’s.

On all these metrics, Hungary is level with, or even ahead of, fellow Visegrad Group members the Czech Republic, Poland and Slovakia. On five-year FDI, it is the region’s star performer, beating even Poland by a percentage point.

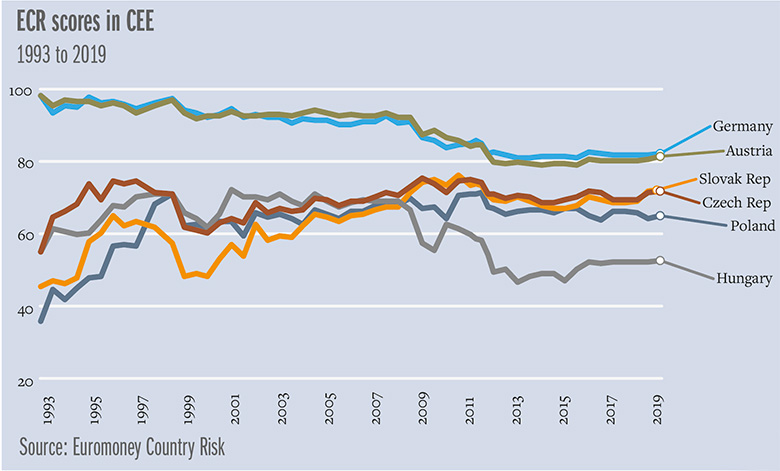

The Euromoney Country Risk scores tell a very different story, however. Here, Hungary decoupled from rest of the Visegrad countries after the financial crisis and has failed to close the gap to any meaningful extent.

As of March, Hungary’s ECR score stood at just 52.7, 24% below the pre-crisis high of 69.3 and 14.1% lower than in September 2010, just before the election that brought Fidesz to power.

By contrast, the Czech Republic and Poland have seen their scores decline by 1.6% and 7.3% respectively since September 2008. Slovakia’s score has risen by 1.1%.

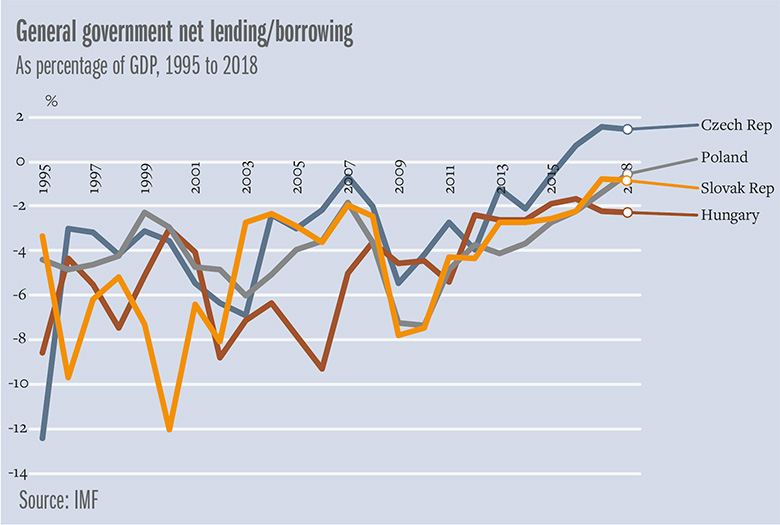

What explains this divergence? Zsolt Darvas, senior fellow at think tank Bruegel, points to the irresponsible fiscal policies adopted by Hungary’s Socialist government in the mid 2000s. Between 2002 and 2006, general government net borrowing averaged 7.9% of GDP a year, according to the IMF.

“As a result, the economic shock of the financial crisis had a much more negative impact on Hungary than the other Visegrad countries,” says Darvas.

Zoltan Arokszallasi, chief macroeconomic analyst for central and eastern Europe at Erste Bank Hungary, agrees.

“Hungary approached the crisis in a fragile situation,” he says, “with very large external indebtedness, huge government debt and relatively poor GDP growth, thanks to a previous economic policy that fuelled growth via consumption and increasing fiscal deficits funded with foreign borrowing.”

Certainly, Hungary’s underperformance in GDP terms relative to its Visegrad peers between 2006 and 2012 cost it dear. At the end of 2018, Hungary’s economy was just 35% larger in dollar terms than at the start of 2007, according to IMF data. Over the same period, Slovakia’s economy grew by 85.7%, Poland’s by 70% and Czech Republic’s by 55.7%.

The growth story in central Europe is substantially underpinned by EU funds and wage growth dynamics, which is not sustainable over the longer term – Zoltan Arokszallasi, Erste Bank Hungary

So, is this an awful warning of the dangers of government over-spending? Not quite, says Mateusz Szczurek, regional lead economist at the European Bank for Reconstruction and Development and former finance minister of Poland.

“It would be too easy to blame all Hungary’s problems on overspending in the mid 2000s – and it would be worrying news for the likes of Romania, which is going in a similar direction in terms of pro-cyclical fiscal policies,” he says. “Hungary has stalled on a number of indicators, including individual consumption, and this has been going on too long for fiscal policy to be the whole story.”

He says Hungary’s financial sector should also take some responsibility for the country’s problems in the 2008 financial crisis, in particular the excesses of the banks and the lack of supervision with regard to foreign currency lending.

At the time of the crisis, roughly two thirds of mortgages in Hungary were denominated in either Swiss francs or euros, making the economy much more vulnerable to exchange-rate shocks than other Visegrad countries.

‘Significant factor’

Hungary started the millennium with much higher government debt than many of its CEE peers because of its decision not to default on communist-era obligations. At the end of 1999, Hungary’s public debt-to-GDP ratio stood at 59.7%, compared with 47.1% for Poland and 15.3% for the Czech Republic.

“This was a much more significant factor in Hungary’s post-crisis problems than some irresponsible policies in the 2000s,” says Szczurek at the EBRD.

At the same time, analysts say it would be rash to discount the effects of Fidesz’s populist and regressive policies on assessments of Hungary’s country risk.

“Since the mid 2010s, Hungary has become more and more isolated politically because of its excessive anti-immigration and anti-EU sentiment,” says Darvas at Bruegel. “There has been a lot of confrontation with EU governments and institutions, so I’m not surprised the ECR score has remained low.”

Szczurek also points to weaknesses in governance in Hungary, including increasing links between politics and the private sector.

“This is part of the decoupling story,” he says. “It is important to look at how much competition within the country is distorted by the presence of well-connected firms that manage to win public procurement contracts.”

|

|

|

Viktor Orbán |

Even Hungary’s much-vaunted FDI figures mask wide regulatory divergence. As Darvas notes, prime minister Viktor Orbán’s government has taken a two-pronged approach to foreign investors.

“In less mobile sectors where foreigners were dominant, such as banking, telecoms and energy, they introduced special taxes,” he says. “At the same time, they heavily subsidized FDI in manufacturing.”

The question is when or, indeed, whether a decade of institutional changes will start to impact Hungary’s headline growth. So far, Fidesz has seen little fallout from its selective approach to governance and regulation, but that could change if economic headwinds build.

One potential pinch point is the labour market. As the rapid increase in wages suggests, Hungary is struggling to find enough workers to meet demand. Nine in 10 Hungarian companies cite labour shortages as an obstacle to investment and growth.

The situation is being alleviated to some extent by controlled migration – despite Orbán’s virulent anti-immigrant rhetoric, workers from countries such as Serbia have been encouraged to fill vacancies in Hungary’s manufacturing sector.

Multinational companies operating in Hungary can also afford to absorb rising wage costs.

“Wages in Hungary are still much lower than in western Europe, while in larger firms productivity is roughly the same,” says Darvas. “The question is how long small and medium-sized enterprises will be able to cope with this.”

The productivity gap between larger firms and SMEs in Hungary is notoriously wide, even by central European standards. Arokszallasi says the differential is already being felt.

“The wage increases over the past two years have put pressure on domestically owned companies to become more efficient, because if they can’t adapt to higher wages they will lose employees and even face closure,” he says.

Szczurek says this would be no bad thing.

“On a micro level, it may mean firms or even whole sectors dying, but over time it will result in countries becoming richer,” he says. “The alternative will be preserving zombie firms, which are profitable enough to survive but not to flourish or challenge the rest of the world.”

He notes, however, that this may be “politically tricky to orchestrate”.

EU funding

Another looming challenge for Hungary is a potential cut in EU funding. Since 2014, the country has received around 4% of GDP a year in cohesion funds. When the next programming round starts in 2021, however, that could fall by as much as 25%.

“A very important element in Hungary’s recent growth has been EU funds, which finance a substantial part of investment in the country and have also helped to reduce external indebtedness,” says Arokszallasi. “If these inflows slow down, against a backdrop of relatively poor institutional scores, there is a question as to how long Hungary will be able to maintain the positive trend of the past two years.”

Of course, this also applies to the rest of the Visegrad countries. Indeed, while Hungary may be the outlier in the group, many of the issues it is facing are mirrored in neighbouring states. Poland also has a populist government picking fights with the EU and weakening institutions, while labour shortages are rising across the region.

Analysts say this partly explains the lack of progress on closing the gap with the likes of Austria and Germany when it comes to risk scores.

“The Visegrad countries have increasingly expressed concerns about the EU and its policies, particularly with regard to migration,” says Darvas. “This conflict with the larger countries in the bloc has caused uncertainty, which may account for the lack of convergence over the past decade.

“There is also still a lot of work to do in areas such as governance and corruption.”

Arokszallasi also points to a regional lack of appetite for tackling complex but urgently needed structural reforms.

“To get their scores back on a convergence path with Austria and Germany, the Visegrad countries would need to resume structural reforms in areas such as healthcare, pensions and education,” he says. “At the moment, the growth story in central Europe is substantially underpinned by EU funds and wage growth dynamics, which is not sustainable over the longer term.”