In the medium to long term there will only be room in the multi-dealer platform (MDP) market for between three and five mega-players, along with around half a dozen mid-sized platforms that play a niche product or geographic role.

That is the conclusion drawn by Forex Datasource managing director Javier Paz, formerly a senior analyst within Aite Group’s wealth management practice, following analysis of trade activity data from 22 MDPs.

When asked to explain the reasons for his confidence that there will be further acquisitions of independent FX MDPs, he notes that liquidity demand from most client groups (tier 2 and tier 3 banks, retail FX brokers, corporations) is not what it used to be.

“It so happens that the FX buy-side — particularly real money firms — have a multitude of operational needs that FX-only, independent platforms can’t answer as well as larger, more sophisticated players such as Thomson Reuters, Bloomberg, State Street and CME Group,” says Paz. These requirements include multi-asset trading, regulatory reporting requirements and post trade services.

Javier Paz, Forex Datasource |

In these circumstances, independent platforms can either accept that they will only grow modestly at best while the average daily volume gap between them and the leaders grows much larger, or they can sell their business at a hefty premium.

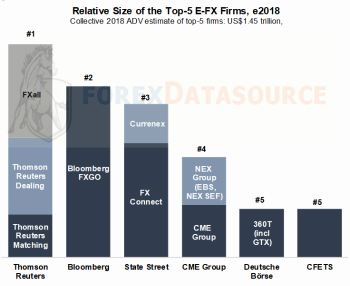

According to Paz, recent mergers and acquisitions have expanded the definition of the term MDP to include not just over-the-counter venues but also regulated exchanges, electronic broking venues, swap execution facilities, multi-lateral trading facilities and even select industry utility firms — as long as these intermediaries offer clients a trading front end/application programming interface (API) and trade matching from their liquidity pool drawn from multiple dealers.

Some of the recent M&A activity has been in response to strategic threats posed by large firms growing trading volume at double-digit rates annually, while another known goal was for major stock exchange groups to own a piece of the OTC FX marketplace. Examples of this trend include Cboe Group’s acquisition of BATS, Deutsche Borse’s purchase of 360T and Gain GTX, Euronext’s acquisition of Fastmatch and CME Group’s acquisition of NEX Group.

Having analysed the various business models in the market, Paz suggests that the most effective strategy is deep workflow integration, with multi-asset class coverage appearing to be the most attractive model for buy-side firms. “Feature-rich FX platforms charging a per-million transaction fee can still do okay with retail FX brokers and tier-2/tier-3 banks that already invest on their own workflow requirements,” he adds.

‘Remarkable’ differences

The above observations might suggest that the FX MDP market is becoming more homogenous, but the only common thread between the leading platforms appears to be the desire to achieve greater scale. In terms of what expertise each platform firm brings to the table, Paz refers to “remarkable” differences.

Source: Forex Datasource |

“For example, you have Bloomberg’s unique terminal business that tends to be fully disclosed trading in a non-latency sensitive environment competing with CME Group that post-NEX Group acquisition has a dominant share in anonymous spot FX trading, FX futures and certain fixed-income instruments,” he explains.

In today’s market, it serves FX platforms better to be a product generalist than a specialist, continues Paz. “In hindsight, and looking at how much faster firms trading in multiple FX products grew their business during their past five years relative to single product pure plays, spot FX specialists probably wish they had diversified into other FX products much earlier,” he says.

In terms of regional trends, Paz notes that fully disclosed trading appears to be strongest in North America and much less common in London, where multi-dealing platforms fare well and co-exist with well-entrenched and large voice FX activity.

“While single-dealer platforms (SDPs) gained market share from other electronic direct trading methods in 2016, they have fared differently across geographic jurisdictions,” he says. “Some of the major banks are again investing in their SDPs, so MDPs will not have an easy path to earning a greater market share.”

So to what extent will MDPs and SDPs co-exist within the same institution? “Client constraints in terms of screen real estate, trading style and ability to support integration with multiple MDPs and SDPs will dictate to what extent they work side by side to serve a common client,” concludes Paz.