By Kevin Rodgers

1970s

It is February 1979. Liverpool’s grave diggers are on strike and refusing to bury the dead; Trevor Francis, the very first £1 million footballer, is being sold on the transfer market; the elections of Margaret Thatcher and Ronald Reagan are still events in the future (admittedly the near future); and for the very first time the Euromoney FX survey is conducted.

It’s hard to imagine what it was like trading FX in 1979. The Bretton Woods system of currency rates pegged to gold had only collapsed six years previously. Indeed, the last reference to gold in the definition of the US dollar remained until 1976. To modern eyes, the global economy of 1979 seems to be emerging from an almost unrecognizably distant world.

Free-floating FX was in its infancy.

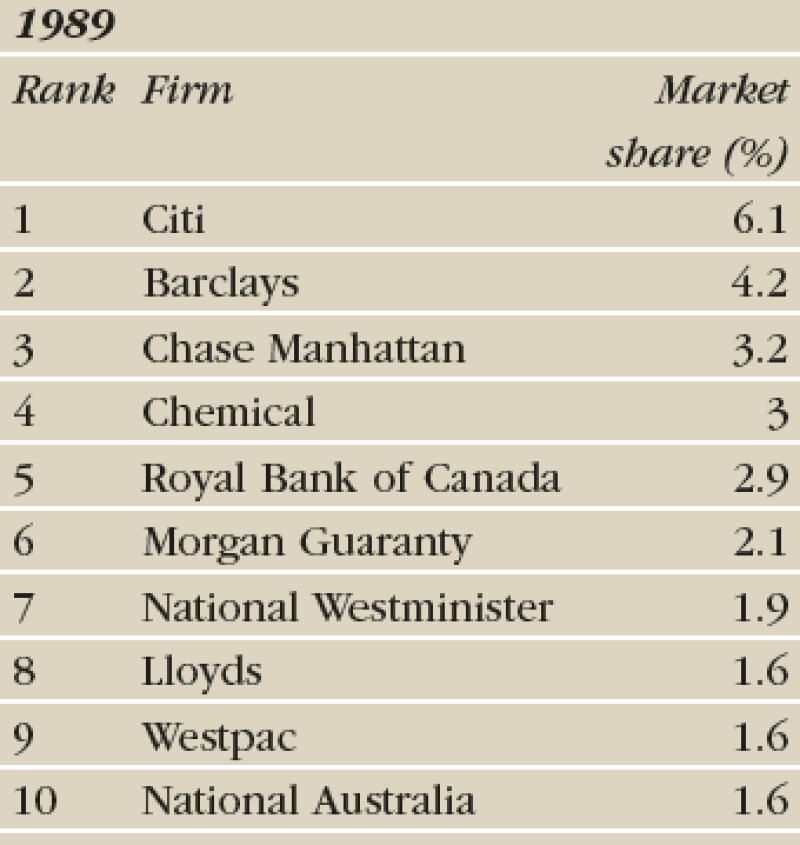

Still, despite all this, and despite the fact that the dealing floors of the time would have looked laughably antiquated to us today (clunky phones, reams of carbon-paper tickets, eye-stinging smoke from pack after pack of cigarettes), the results of that sepia-tinged survey look surprisingly modern.

Citi is number one, Chase Manhattan (JPMorgan nowadays) is number two, Morgan Guarantee (ditto) is number three and so on.

It’s true that some of the names lower down the table are a mystery – at least to me. What was European American? Wasn’t Hill Samuel a low-end chain of jewellers? But overall, if you blur some of the picture, it’s not startlingly different from one you might have seen in the last three or four years.

With this surprisingly modern looking survey, the annual Euromoney FX poll was born. Much loved through the years (and, let’s be honest, also occasionally much loathed), it is now a successful 40-year-old whose life story captures the twists and turns of the history of the world’s biggest financial market.

1980s

Although it was before my time, I have heard it said that the 1980s were the glory years of FX. For one thing, there weren’t any pesky computers to take away an honest man’s living – oh, and liquid lunches were the rule. Nor were there that many limits on behaviour on the trading floor itself – short of manslaughter that is.

Happy days.

Then there were also big FX trends to be your friends. Spurred on by Reaganomics, dollar/Deutschmark (the currency pair for ‘real men’ back then) went from 1.7200 to 3.3000 and all the way back again in the course of 10 years.

The $/D chart looks like the profile of Mont Blanc, with its peak the Plaza Accord in 1985, which aimed to weaken the rampant dollar and, in this aim, succeeded.

Make no mistake, it was the greenback that was the dominant currency back then. Maybe that explains why North American firms were so entrenched at the top of the market share table for most of the decade.

It is noticeable that, with the honourable exception of occasional appearances by Swiss Bank Corporation (SBC) and then Barclays, North American firms make up at least four and sometimes all of the top five slots throughout the decade.

The other consistent thing, of course, was that for every single survey Citibank was number one – a fact that with each passing year must have made them look untouchable as the foremost FX house.

But things were changing in Europe. For one thing there was deregulation: 1986’s Big Bang in the City of London, although focused on equities, brought large amounts of risk capital into a big European hub.

Then at the end of the decade came the fall of the Berlin Wall and breakup of the Soviet Union.

1990s

Perhaps because of these changes, 1990 was the first time two European banks made the top five: Barclays and NatWest. In 1991, SBC joined them to mark the first time the majority of the top five had come from outside North America.

The EU’s tentative first step towards the euro – the Exchange Rate Mechanism, or ERM – was attracting speculative flows from bond players comforted by the system’s tight banding of national currencies.

It didn’t last, however. In 1992 and again in 1993, the system blew up spectacularly. FX made front-page headlines. Screaming, waving, gesticulating 20- and 30-somethings were a nightly vision on the 10 o’clock news. By now, I was one of them.

The turbulence was reflected in the poll’s make up for the next few years. Names came and went from the top five in rapid succession, although Citi hung on tight at number one.

Perhaps the cause of this positional churn was that overall market share concentration was still pretty low so that small year-on-year alterations in a bank’s market share had a large effect on its ranking.

All this was to change. At the start of the decade, the top five accounted for around 20% of surveyed flows. By 1999 this number had reached 33%.

Why? In part, the change reflects the process of banking industry consolidation. Regulatory impediments to mergers were removed one after the other in the US throughout the decade. As a result, banks flowed together like the molten blobs of killer robot at the end of ‘Terminator II’. Manufacturers Hanover into Chemical; Chemical into Chase; and ultimately Chase into JPMorgan. All this is reflected in the shifting set of names in the survey.

Then on January 1, 1999, came another sort of consolidation: the creation of the euro. In one bound, the European FX market – previously hideously fragmented – was unified into a single, giant bloc.

Last, like a softly ticking time bomb, the FX market’s other great change agent began its countdown. This was rising computer power, which enabled the creation of the internet, the construction of electronic trading venues such as EBS, the extinction of voice spot brokers, which spurred banks’ first stumbling steps towards automation – all in quick succession.

2000s

The start of a new millennium heralded an appropriately monumental event, or at least that’s what some people thought inside Deutsche Bank. Citibank, after two decades unchallenged at the top of the Euromoney heap, was kicked out of its castle by the German firm.

True, this win was a bit of an outlier and Citi were back on top in 2001, but a genuine seismic shift had occurred. The continuing aftershocks were reflected in the Euromoney surveys in the next few years.

A vicious three-way fight for top spot was won first by UBS, then by Deutsche, which then held on to the crown for the rest of the decade. The market share of the top five rose inexorably: from 38% in 2000 to a startling 62% by 2009. What’s more, by 2009, the top five places were dominated by Europeans; only Citi kept the Stars and Stripes flying at number five.

The chief driver of all this was an escalating arms race in automated trading, in which Deutsche, UBS and Barclays excelled in particular. Two completely coincidental following winds helped them in their path to the top: the scale benefits brought by the euro and the global financial crisis of 2007 to 2008 that made many clients wary of US banks.

In fact, the entire structure of the FX market was twisting and creaking into its very new shape during this period.

Away from the overall market share table, the details of Euromoney’s surveys reflect this in, for example, the rise of market share channelled through FX platforms (unheard of at the start of the decade) and the swelling importance of a client type called ‘high-frequency trading firms’.

All told, a trading floor time-traveller from 1979, arriving in 2000 and looking at the FX market would still have been able to recognize (after he’d been forced to stub out his cigarette) the faint but comfortingly familiar outlines of the world he had known. By 2009, it would have seemed a confusing, almost silent alien planet.

2010s

In the most recvent decade in the life of the survey, some of the trends of the previous 10 years have been unwound somewhat. American banks, led by Citi and then followed by the enormous JPMorgan, have re-established themselves as leaders in FX as the credit impact of 2007 and 2008 fades into history.

As a result, some previously dominant European banks have had a rough ride. Barclays, RBS, even Deutsche have slipped down the rankings (although Deutsche appears to be on the way back).

Market concentration – seemingly destined to grow without ceasing – has reversed a little as technological knowledge has become more widespread, and volatility has been squeezed out of the market. In the latest survey in 2019, the top five banks only account for 40% of market share.

Did I say banks? Let me correct that to liquidity providers, since one strong trend in the Euromoney surveys of the 2010s has been the increasing importance of the specialist e-market making firms such as XTX, HCTech, Jump and Citadel Securities.

Best not show the flared-trouser-wearing 1979 time-traveller these guys – the shock might be too great, especially after lunch.

It’s just one more sign, if one were needed, that the FX market is still evolving rapidly.

What will the future hold? Perhaps in 10 years’ time we’ll be looking at market shares in cryptocurrencies as a separate category. In 20 or 30 years, we may see the rise of completely automated firms – just self-governing AIs; no humans required at all.

Good luck getting them to the awards ceremony.

Or, in 40 years, perhaps the chief controversy will be disputes over market shares in trading a lunar dollar (or lunar yuan).

If so, I probably won’t be around to see it, but I hope that the Euromoney FX survey will be – just as it has been every year since 1979.

Source for all charts: Euromoney Data