There is a certain cosiness to the 36th floor of the Brics Tower, where the executives of the New Development Bank reside, and it’s not just because it’s a grim and murky day in Shanghai.

“The guy who just walked in is one of the vice-presidents; his office is next to mine,” says Leslie Maasdorp, CFO of New Development Bank and a vice-president himself. “The president’s office is there. There are two more VPs there,” he says, pointing. “On this floor is the entire credit committee.”

Being small, centralized and nimble is a key differentiator for NDB, says Maasdorp: “If there’s a project, we don’t have to wait for weeks to convene the investment committee. We call a meeting, assess the project, approve it and move on with our lives.

“To convene five people on one floor is a lot easier than 12 in different time zones.”

Over the last 12 months, NDB has had the chance to put that nimbleness to the test. It has gone from being an interesting idea to being a genuine lender and, in doing so, has become perhaps the single most important outcome of Jim O’Neill’s iconic Brics acronym of 2001 referring to Brazil, Russia, India and China.

Bric became a formal institution in 2010, with South Africa added later in the year. It was never entirely clear what it meant, other than an arbitrary and conveniently pronounceable aggregation of enormous emerging market economies. It was and is strikingly diverse in geography, culture, political systems and economic outlook.

So why did such an apparently meaningless bloc need a bank?

|

| Leslie Maasdorp, New Development Bank |

“In the context that there are several multilateral banks, why was this thing actually set up?” Maasdorp nods.

“The creation of the bank,” he says, “is an expression of the intent of emerging markets to take their rightful role in global governance.”

Also, the five Brics nations illustrated the desperate need for infrastructure development in emerging markets. Clearly, they are not the only countries with that need – Indonesia and the Philippines need roads and power just as much as South Africa and India – but there was a sense that a bank for the Bric economies would still have plenty it could achieve.

“Also, given climate change – and we are absolutely persuaded that the world is undergoing fundamental changes – these banks have a public good objective to build infrastructure in a new kind of way,” Maasdorp says. “It’s not just about building roads or ports or power plants, but looking through the lens of what damage you are doing to the environment.”

A Brics bank, it was decided, should be all about sustainable infrastructure, climate resilient and built with proper governance. It would also need to have a long-term view and a profound understanding of technological change.

“You cannot just build a road,” Maasdorp says. “You’ve got to configure what autonomous driving will mean in five, 10, 25 years for that road. So we weren’t just created to be another bank for emerging markets.”

With those ambitions in mind, the bank set about the practical side of formation. The idea of a Brics bank was first mooted at the fourth Brics summit, in New Delhi in 2012. The finance ministers of the five constituent nations reported back with their ideas at the next summit in Durban the following year.

During the next one, in Fortaleza in Brazil in 2014, an agreement was signed to establish what was now called the New Development Bank. The inaugural meeting of its board of governors took place just before the Ufa summit in Russia, on July 7, 2015. KV Kamath, formerly chief executive of India’s ICICI Bank, and chairman of Infosys, was appointed president. The agreement for the bank’s headquarters, in Shanghai’s Pudong, was signed in February 2016.

Commitment

The bank’s shareholding is split equally five ways among the member countries and they have all been expected to commit themselves fully.

“The bank shareholders put in considerable capital to create this institution,” says Maasdorp, whose own background includes being president of Bank of America Merrill Lynch for southern Africa, vice-chairman of Barclays Capital and Absa Capital and an international adviser to Goldman Sachs.

He has had several senior roles in the South African government, including as deputy director general, leading the restructuring and privatization of state-owned enterprises in the late 1990s.

“This is a major commitment by these institutions,” Maasdorp says. “Each put in $2 billion, coming in instalments; we just received the fourth instalment and are more than halfway to the $10 billion.”

This is another important distinction, he says. The ratio of paid-in capital to subscribed capital at the NDB – 20%, with $10 billion paid in and $50 billion subscribed – is the highest among multilateral banks.

“It’s a much higher proportion of equity, which demonstrates the strong commitment of our shareholders to the institution,” he says.

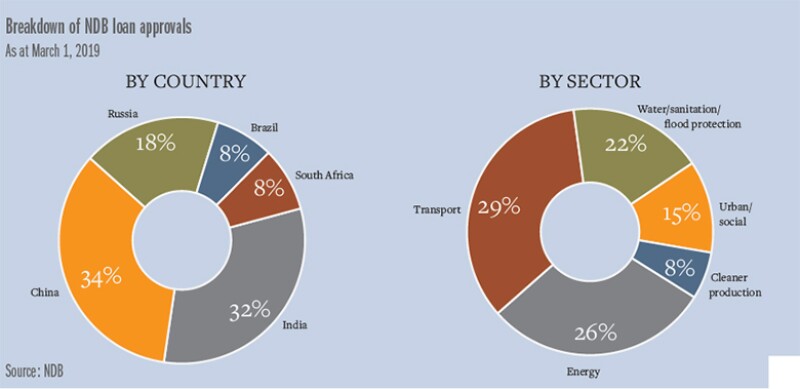

In 2016 to 2017, the bank approved loans involving financial assistance of over $3.4 billion across green and renewable energy, transportation, water sanitation and irrigation. But the real milestones began to come in 2018.

The first one Maasdorp raises is particularly important for a CFO in charge of treasury matters: a credit rating. The bank is now rated AA+ by both S&P and Fitch.

“The credit rating is a very critical metric for a financial institution, even more so for a multilateral bank,” says Maasdorp.

Although NDB, like any multilateral, has both paid-in and subscribed capital, “the most important resource for us is the capital we raise in the debt capital markets. To raise those resources as cheaply as possible you need a solid and high credit rating.”

Most of its peers are triple-A, reflecting risk-aversion, liquidity, solidity and low leverage. NDB has started out a notch below. But that must be seen in context: the weighted average of the five constituent members is BBB minus. Brazil and South Africa, at BB+ are junk status (though South Africa is investment grade, Baa3, with Moody’s); Russia and India, at BBB minus, are just on the cusp of investment grade; and China, at A+, is the strongest but still the subject of a recent downgrade.

“Over the last few years each of our countries have experienced a downturn, but despite that the bank’s own credit rating is several levels above the average of those countries, which is a significant achievement,” Maasdorp says. “It’s because of the financial metrics and benchmarks, which are very solid, and that’s what Fitch and S&P recognized. The credit rating is the first major achievement of the bank, a critical ingredient.”

Also, the lending book is now getting up to high levels. At the time of this interview, it stands at $8.4 billion of approved loans.

“That’s a small amount in the context of infrastructure requirements globally and in those countries,” says Maasdorp, “but it’s a significant number for a new institution a little bit more than three years old.”

Projects

NDB has proven it can identify, appraise and fund projects, but what it hasn’t done nearly so much of is put the funds that it has approved to work. Only $650 million has been disbursed to date.

“There is obviously a delay in getting disbursements out,” says Maasdorp. “It’s one thing to design a project and have it formally approved by the board, but it’s another to have the money flowing, the procurement done, the power station built, the port upgraded.”

Still, he presents this as just a matter of time and points out that the approvals to date cover 30 projects in all five countries.

With the bank established, there is an intention to grow it – not just in terms of loan book but also location.

“It was never intended only to be a Brics bank,” says Maasdorp. “The idea was always to create an institution that can eventually become the voice of emerging markets.”

The bank’s governors are considering a “phased expansion”, he says.

The articles of association are quite clear on how this might happen. They countenance a gradual dilution through which the Brics countries drop to 55% between them – that is, from 20% each to 11% – with another 25% allocated to emerging markets and 20% to developed countries that would come in as non-borrowing members.

|

The articles of association also specify that no non-founding nation can come to hold more than 7% of the shareholding.

“There’s nothing unusual about that,” Maasdorp says. “It’s the way AIIB [Asian Infrastructure Investment Bank] is also set up and how other MDBs [multilateral development banks] work. We are unique now in that we only have borrowing members – lending to ourselves, where we are the shareholders and also the borrowers.”

But that won’t be the case for ever. He says he hopes “the likes of the UK, Germany, France will join.” (This is perhaps not a good moment to ask the US to participate in globalization.)

Maasdorp says there is “very strong interest” for others to join, partly because of the sheer scale of their needs. “Whether it’s Vietnam, Turkey or Mexico, they have a massive need for funding.”

Also, the gap is so severe that there is no sense of multilaterals stepping on one another’s toes: joining one does not annoy another, so one might as well join as many as possible. Notably the Mumbai metro rail project, to which the NDB has committed a $260 million loan, involves funding from NDB, AIIB and the Asian Development Bank (ADB).

“There’s a sufficient number of projects out there, and not enough capital,” says Maasdorp.

Then there is the China angle. China is now the headquarters of two multilaterals, first AIIB and now NDB.

“There’s no question China is playing a bigger role in the multilateral system,” says Maasdorp.

But while the bank talks of expansion, it still faces a challenge in getting things done in its founder countries. There has been a heavy focus on China and India, and far less on South Africa.

“There is definitely an intention to have a properly balanced portfolio among the five countries,” he says. “It’s not surprising that China and India would be disproportionate in the initial phase.”

They have larger economies and China has a very clear infrastructure rollout programme mandated by the state, he says. “You wouldn’t find such a robust clearly defined five-year plan in South Africa. They’re certainly not building 60 airports there.”

Still, he expects what he calls “a hockey stick” graph of investment uptick in South Africa, noting that new president Cyril Ramaphosa said in his first address to the nation that he would stimulate new investment in infrastructure. NDB has a target of $1.5 billion to $2 billion to be deployed in South Africa this year, which would be a fourfold increase on the $500 million committed in 2018.

“What you are going to see now is a shift in momentum towards Brazil and South Africa,” says Maasdorp.

These are not always easy places to do deals on the right terms, however. The first attempt to engage with South Africa involved lending to a renewable energy project through the national utility Eskom. That was swiftly caught up in allegations of corruption.

“We originally had a loan to Eskom, which was saddled with corruption allegations and governance challenges,” he confirms. “So that loan was put on ice and never formally concluded.”

The management of Eskom has changed since then, as has the national leadership.

“We have great confidence in the new leadership in South Africa,” says Maasdorp. “That’s given us comfort levels.”

And what of the new leadership in Brazil? “People are taking office as we speak. [Euromoney was speaking to Maasdorp at the beginning of the year.] We don’t know the people yet, so it is too early to comment on what the likely impact is going to be.”

But he says he takes comfort from public statements about fighting corruption.

Funding

With the debt rating in place, Maasdorp is now planning to use it in funding. He intends to borrow both in dollars and in local currency, most obviously in renminbi, since China has by far the biggest domestic capital market of the five founder nations. It will then lend in local currency.

“The aim is not to raise local currency, as some have done, and swap for the arbitrage,” he says. “We will raise local currency and lend in local currency, and remove the exchange rate risk.”

The bank borrowed in renminbi in July 2016, raising Rmb3 billion ($446 million), and has a Rmb10 billion programme registered, approved in December by the People’s Bank of China. A first tranche of that programme raised Rmb3 billion in February. Renminbi funds are already being deployed: the bank has committed a Rmb2 billion loan for the Guangdong Yangjiang Shapa offshore wind power project.

The NDB is registering a rand bond programme in South Africa and plans an inward listing on the Johannesburg Stock Exchange, which was “at an advanced stage of regulatory approval” in March.

India will probably be next, starting with an offshore rupee bond. The hope is that, in addition to raising appropriate funding, the bank can also help the development of the local bond markets, which tend to be dominated by shorter-term money; NDB expects to extend the maturity profile of local bond curves, matching the long duration of its project loans.

Climate change, cybersecurity, refugees, terrorism – all these things have cross-jurisdictional origins and you can’t deal with them without institutions that take a transnational view - Leslie Maasdorp, NDB

A debut in dollars won’t come before 2020.

“It takes a lot more time to register a US dollar programme,” says Maasdorp. “AIIB has just registered theirs and it has taken the better part of 15 months to do. We’ve been watching that closely.”

Indeed, NDB has been watching AIIB, which is somewhat ahead in its staffing and membership, if not lending.

“We work very closely together,” says Maasdorp. “We will do a lot more with them this year.”

Like AIIB, NDB believes it can be much faster than older multilaterals.

“We want to be more agile. Just faster, basically,” he says. “We have decided that the time it takes for a project to be designed and approved should not be more than six months.”

That contrasts with a more typical 18 months today. “We are hoping to remove the occupational hazard aspects of dealing with MDBs. They are seen as bureaucratic and slow moving, with red tape. But when you are new, you have a huge advantage because there is no legacy.”

This is fine, but the reason banks like the ADB take so long is because they feel it is necessary for suitable due diligence and the avoidance of corruption.

“There’s no way that the bank can change from the accepted policies and practices of how risk management in project appraisal is done,” says Maasdorp. “If you look at our policies, they are mirror images of those at the European Investment Bank, ADB and so on.”

Instead, he says, the scope for improvement in efficiency comes in other areas, principally size, which brings us back to his comment about all the expertise being on one floor. Technology, too, has a role to play, with greater use of video links instead of feeling obliged to fly to countries for loan negotiations. But there will not be compromise on environmental sustainability, he says.

The bank won’t stay small. At the time of our interview, NDB has 145 staff, expects to hit 250 by the end of 2019, 390 by the end of 2020 and 500 by 2021.

And looking further out, 10 years from now, how will the multilateral landscape look?

“I’d say there are going to be fundamental changes in this space,” he says. “The Trump phenomenon has caused a questioning of the role of multilaterals in the world, but I think that debate will be useful because it will deepen the understanding of multilaterals – not just banks, but the WTO, the UN.

“Climate change, cybersecurity, refugees, terrorism – all these things have cross-jurisdictional origins and you can’t deal with them without institutions that take a transnational view.”