Illustration: Kevin February

One day in May 1981, Yong Pung How turned up for his first day as managing director of a new Singapore sovereign wealth fund, although it didn’t yet have a name and nobody had ever heard of a sovereign wealth fund.

Seconded from his job as vice-chairman of OCBC, which he had one day been expected to run, he was already taking a pay cut to do this new public-service job. It is unlikely his spirits were greatly improved when he turned up at the Monetary Authority of Singapore offices on Robinson Road to find he had no staff, no secretary, no functioning telephone (it needed a key to activate it and nobody knew where it was) and no chair.

Thirty-seven years later, sitting in its offices on the 37th floor of Singapore’s Capital Tower, it is fair to say the Government of Singapore Investment Corporation (GIC) has moved up in the world. It is considered one of the most sophisticated and influential sovereign wealth funds globally.

It might well be one of the biggest too, but the government does not disclose the fund’s assets under management (AuM), reasoning that to do so would be to reveal the size of Singapore’s financial reserves and make it easier to mount speculative attacks on the Singapore dollar. Few internally even know the magic number.

“That,” says one employee, “is a burden I don’t wish to carry.”

|

|

|

Lim Chow Kiat |

Although it publishes a detailed annual report, GIC doesn’t talk a great deal and Euromoney’s interview with chief executive Lim Chow Kiat has been a long time in negotiation. In fact, the period from Euromoney’s first request for a chief executive interview to this morning’s meeting is 11 years.

There have been a lot of changes in Singapore in that time. The whole Marina Bay waterfront has been built, and from the window we can see the cranes of the port being gradually dismantled and moved to new facilities in Tuas, the land to be rebadged as the Greater Southern Waterfront.

The city state’s constant regeneration is reflected somewhat by its sovereign wealth vehicles. Nowhere else is like Singapore, with three separate sovereign institutions with distinct mandates. The Monetary Authority of Singapore, effectively the central bank with official foreign reserves of S$292.5 billion ($216 billion) as of February 2019, backs the currency; GIC invests and diversifies Singapore’s other reserves; and Temasek, founded in 1974 and with S$308 billion under management as of March 31, 2018, has its origins in the stewardship of Singapore’s state-owned companies and invests mainly in equities with a mandate to earn a spread over its cost of capital in the long term.

Of the three, GIC is the one that most resembles the classic sovereign wealth fund model: diversified across multiple asset classes, investing purely overseas and with a mandate to beat inflation. Within that framework GIC has reinvented itself several times, first evolving towards an endowment model well before that was fashionable and then conducting another investment review in 2012 to build an investment model for the future. Along with the Abu Dhabi Investment Authority (Adia) and Norway’s Government Pension Fund Global, it is perhaps the most closely watched, admired and emulated sovereign fund in the world.

Key differentiator

Euromoney starts by asking Lim about one of GIC’s key differentiators in the sovereign wealth world: being a first mover in many themes. It was the first non-hydrocarbon state to launch a sovereign wealth fund, to set up an office in San Francisco in 1986 in order to get ahead of the tech theme and is considered a pioneer in private equity and infrastructure investment. Has it benefited from its willingness to be an early entrant into new spaces?

“I guess being early is not always the best thing,” says Lim. “But thankfully, in our case, being early in a number of areas has been quite good.”

He highlights private equity: “We benefit from some of the relationships which were built many, many years ago – like 25 years ago.

“Because of the long relationship, our collaborations with them typically would be closer and better than others. That is a significant benefit.”

It’s not enough that you do better than beta. You have to deliver something risk-adjusted to account for the additional risk you have taken on – Lim Chow Kiat

The length of time in these markets has also allowed GIC to learn. Being in San Francisco in 1986 has allowed for a good education.

“Being there, you have more natural exposure to technology investment,” says Lim. “It is not all smooth sailing, it goes up and down; right after the dot.com bubble there was a winter. But even during those times we learned: how do you pick the right startup, the right entrepreneur, the right business model?”

Lim exemplifies this sense of institutional learning. He joined in 1993 as a portfolio manager before rising to head the fixed income, currency and commodities department, and later overseeing investments in Europe, Africa and the Middle East.

“I’m like a piece of furniture here,” he says. “We are fortunate that we continue to have people who stick around. We are very careful and conscientious in succession planning, making sure one generation passes to the next in a fairly deliberate manner.”

It is fair to say that GIC has been instrumental in the development of the whole fund management industry in Singapore. Groups like Wellington Management and Bridgewater Associates first came to Singapore to service GIC, subsequently diversifying their client list from there. GIC invested in Bridgewater itself early on. Insiders say they were working together back when founder Ray Dalio used to answer his own phone.

“That’s how far back we go,” says one.

It is not easy to be a portfolio manager at GIC. As a starting point, you have to justify the right to invest any capital at all.

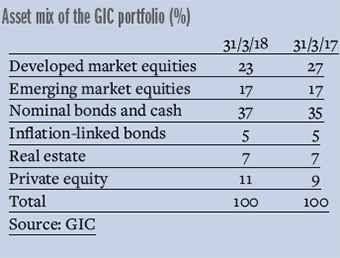

The 2012 investment review brought about a change in approach. GIC now considers six core asset classes: nominal bonds and cash; inflation-linked bonds; developed market equities; emerging market equities; real estate; and private equity. Then about 20 strategies are laid over those asset classes.

Then there are a series of building blocks. GIC has what it calls a reference portfolio, made up of 65% global equities and 35% global bonds. It is not a benchmark as such, but it represents the overall risk tolerance GIC thinks appropriate in order to generate good long-term returns over global inflation.

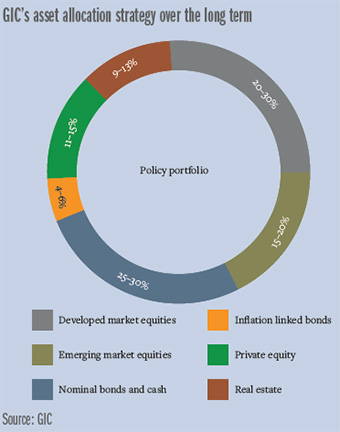

Next is the policy portfolio. This sets GIC’s asset allocation strategy over the long term. Currently the ranges within it are 25% to 30% nominal bonds and cash, 20% to 30% developed market equities, 15% to 20% emerging market equities, 11% to 15% private equity, 9% to 13% real estate and 4% to 6% inflation-linked bonds.

Things get interesting when you get to the active portfolio, through which managers attempt to add value to the policy portfolio without skewing the amount of risk that is being taken.

Lim explains: “Our starting point is beta: getting a return by holding on to something for the long term and earning that risk premium over 20 or 30 years.

“So for us to be out of that, we would need the alternative to be better. ‘Better’ typically means more return. But sometimes better can mean lower risk.”

Internally, the process of taking the money out of beta and into an active position is known as skill-based strategies.

“So the team have to make a proposal that what they are going to do will be better than the beta that they have. Their job – their key performance indicator, their bar – is to do better than what they have foregone.

“There is a cost to it: the opportunity cost of foregoing beta and the riskiness of the investment. It’s not enough that you do better than beta. You have to deliver something risk-adjusted to account for the additional risk you have taken on.

“It works pretty well.”

And how do internal managers feel about it?

Lim laughs. “I think they recognize that at the end of the day a pool of capital has different uses. And they recognize that the default position is for GIC to earn this long-term risk premium. For them to really add value, they must be better than that.

“Of course alpha is a tough game. But at the same time GIC affords our alpha teams some advantages: the time horizon, the size, the connections that we have with the investee community. I hope they feel like it is fair game that they have to deliver that.”

It is perhaps a particularly difficult time to do that.

“Beta has done great for the last 10 years,” Lim says. Interest rates have come down and prices have gone up. “But that also means going forward is a lot harder, because yields are so low.”

In the environment of the last 10 years, alpha has been tough to find as volatility has been low. But it has increased and Lim expects it to continue to do so: “The odds seem quite good, I would say, because there are quite a few of these big events in the world that could drive volatility higher.”

Challenge

Although we don’t know how big GIC is, it is certainly big. For example, it is one of the largest real estate managers in the world, despite the fact that real estate should only represent 8% to 13% of the portfolio – and that makes it difficult to keep allocations in some asset classes as high as GIC would like them to be. So, for example, on March 31, 2018, the allocation to real estate stood at 7%, below the intended range, while nominal bonds and cash stood at 37%, above the intended ceiling.

(InRev, a European association for investors in non-listed real estate vehicles, publishes an annual ranking of property holdings at investment managers, based on public information, which is why GIC isn’t in the ranking. Making the top 10 of that list required about $60 billion in real estate assets as of the end of 2017. If GIC were to be at that level and $60 billion represented 7% of the portfolio, GIC would have $857 billion under management and be among the biggest funds in the world. But this is nothing more than educated guesswork. The Sovereign Wealth Center research group puts the group AuM figure at $398 billion.)

In any event, the challenge of keeping money where you want it to be is most obviously the case in private equity, real estate and infrastructure; private equity in particular because investments mature.

“Money comes back. It’s hard,” Lim says. “The guys are working day and night 24/7.

“Having a lot of very strong relationships helps, because in most cases we partner with general partners, family offices, even corporates.” That helps to gain access to asset classes where there is a great deal of demand. “But still, it is a struggle, partly because competition is very keen. In the last 15 years we saw a lot of influxes of large pools of capital.”

You said earlier that GIC seems to be unique, but the unique thing is not what most people see. The most unique thing is the governance arrangement – Lim Chow Kiat

In infrastructure, he says, the challenge is supply, not demand. “There’s capital available, but the pipeline of supply – of bankable projects – is not as strong.”

Although multilaterals do valuable work in trying to help to prepare projects for investors to come in, he says that is a long-term effort and he is concerned about the fact that projects are becoming increasingly politicized “in the name of the rise of consumers, in the name of not giving value away to foreigners and big corporations; which is not a healthy development.”

He worries about changing regulation and notes that particularly in emerging markets, “they need to be more careful with tinkering with any agreements they have already signed, any regulation they have already put in place. Infrastructure has that particular challenge.”

So, what makes a bankable project? Regulatory certainty?

“Not just that, but it has to be big. The other is that on the supply side, governments need to have the expertise. They need to know how to work out the regulation, to assemble the assets, to make the financing arrangements, a lot of those things that are still somewhat lacking.”

The point Lim makes about relationships with investee companies is important. GIC is so influential now that it can be helpful to the companies it invests in, whether through advice or just connections. A good example is Vietnam. GIC was an early investor in Techcombank and in January took its stake in Vietcombank to 2.55% following a private placement, having been an early investor beforehand.

Nguyen Le Quoc Anh, chief executive of Techcombank, told Euromoney at the time of the bank’s IPO in 2018 that GIC’s knowledge was helpful: “We said [to GIC]: ‘We know how to run a bank, but we need a portfolio company to tell us what else is going on in the region.’”

Lim says: “We are largely a financial investor, so our help a lot of the time is at the governance level and in introducing, sharing our network with our investees. In recent years, we have really stepped up on that.”

GIC holds occasional invitation-only events where a couple of hundred investees or other business partners are invited and encouraged to talk. “We provide the platform for them to do that.”

NIRC

For the moment, GIC invests without much concern about funds being taken away from them; there has only really been one drawdown from the past reserves pool to which GIC contributes, during the global financial crisis, for a national resilience package in 2009. The finance minister at the time, Tharman Shanmugaratnam, made it clear this would not be a regular occurrence.

Tharman will become deputy chairman of GIC from May 1.

He called it “exceptional measures for exceptionally dangerous times”.

There is, however, a process called the Net Investment Returns Contribution (NIRC), made up of up to 50% of the net investment returns on the net assets invested by GIC, MAS and Temasek, and up to 50% of the net investment income derived from past reserves from the remaining assets. The amount that is taken is published in each year’s government budget. The government has used this contribution for 11 years, principally to top up endowment and trust funds, and it is now the single largest contributor to government revenues, worth S$17.17 billion to the 2019 budget.

But since the NIRC involves investing returns, not the funds that were deployed in order to gain the returns, this doesn’t affect the fund’s liquidity position or require it to change its long-term approach.

“It doesn’t look like it will seriously affect how we operate,” Lim says. “I wouldn’t be too concerned about that. The real challenge is the investment environment.”

The government itself addresses this in a statement: “By basing the government’s spending on expected long-term returns of the investment entities on the framework, the investment entities [Temasek, GIC and MAS] are not pressured to sell assets, realize capital gains and pay more dividends.”

Generally, Lim and his staff are at pains to point out that GIC is just a fund manager on behalf of its client – the government: “We don’t get involved in the spending. Our job is to make sure that we generate good long-term returns.

“You said earlier that GIC seems to be unique,” he adds. “But the unique thing is not what most people see. The most unique thing is the governance arrangement. The government makes it very clear and is very disciplined about that – to leave GIC alone to just focus on making money. It is hard for a lot of governments to do that.”

He takes the same approach when asked about the mystery AuM number. “That’s not our prerogative,” he says. “It’s the government. Professionally it has not hindered our work.”

GIC also stands out for its headcount of about 1,500 people, which is thought to be second only to Adia (1,700 employees at the end of 2017). So why do so much internally?

“Various reasons,” says Lim, “one of which, of course, is cost. To be sure, we use a lot of external managers – hundreds of them in all asset classes – but in-house has a cost advantage. I won’t tell our guys they are cheap, but it does.”

Outsourcing takes place in market segments where GIC doesn’t feel it has the internal capability or if there are opportunistic situations that are brought to it. It is somewhat notorious among external managers for its internal knowledge. More than one manager has told Euromoney how it pitched up to GIC with its best idea only to find that it was already doing it, and doing it well, internally.

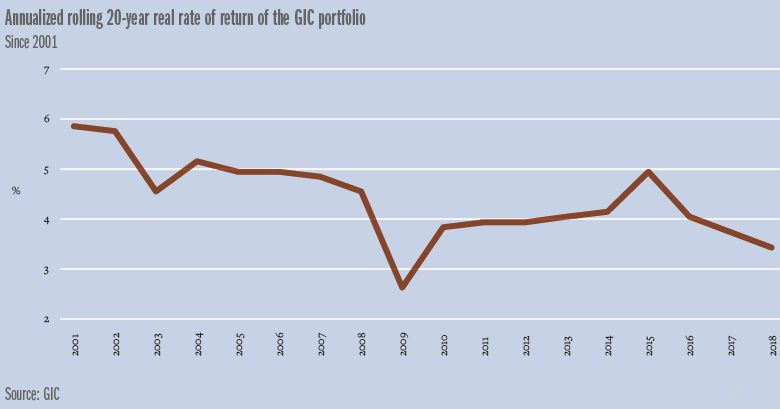

That said, GIC’s long-term return – its main performance metric is a 20-year annualized return – was 3.4% above global inflation up to March 31, 2018. This is not exceptional and well below the almost 6% it stood at in 2001, although this is partly a result of the tech stock boom in the late 1990s gradually falling from the long-term numbers, with the post-bubble declines still there.

Public duty

Back when Yong Pung How stepped out of his impressive OCBC career to start GIC with no chair there was a clear sense of public duty about the fund. Yong had at first politely declined the offer, whereupon Goh Keng Swee, one of the architects of modern Singapore and one of the founders of the MAS a decade earlier, went to OCBC chairman Tan Chin Tuan to ask if he would lend Yong to the national cause.

Singapore is still an intensely patriotic place and GIC has retained a sense of public duty, no matter how many non-Singaporeans have come and gone through its doors over the years.

“I would say that GIC-ans share a lot of what you might call noble purpose,” Lim says. “That is a very powerful recruitment tool for us. And not just with Singaporeans: I find it interesting and amazing that a lot of our non-Singaporean colleagues identify with the idea that you would patiently, in a disciplined way, manage a pool of money that would benefit a lot of people.”

Did he feel that way in 1993? “I certainly did in my case. I was originally from Malaysia; I came here as a teenager and had my education here, so I felt like the country had really helped me a lot.”

At GIC, he thought, “I could have some impact.”

It is also, he says, a good place to work: “We give a lot of opportunities to people, like my own experience, in that it opens the door to world markets. It’s a challenging but interesting job. You learn every day.”

Asked if he wants to say anything in conclusion, he turns again to the environment of uncertainty in the world today.

“All this geopolitical stuff. We were fortunate that since the 1980s, or even earlier, all this politics didn’t really matter. By and large politics was swinging around the centre. But this time we truly have the prospect of politics going to extremes, and that is going to have a significant impact on economies and asset prices.”

And demonstrating yourself as an institution with good intentions is more important than ever?

“Definitely. Because everyone is watching. Good behaviour will be rewarded. And bad behaviour will be punished.”