|

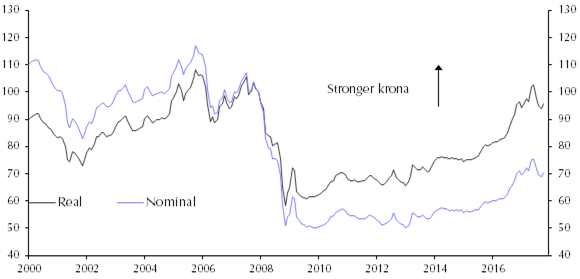

The country has already scrapped most of its capital controls this year, and the currency has steadily appreciated against the euro since.

Gisli Hauksson, co-founder and chief executive of Gamma Capital Management in Reykjavík, says: “The króna’s performance this year has definitely come as a surprise to a lot of people, given the rationale for having the capital controls in the first place was actually to keep the currency from falling.”

The remaining restrictions are designed to prevent speculative trading in the króna. It was heavily traded in the years immediately before the financial crisis. Huge króna-denominated eurobond issuance, offering an attractive interest rate versus the euro, led Iceland’s currency to swell to an unsustainable size relative to the country’s economy. But trading collapsed when Iceland found itself at the centre of the storm in 2008, with its three biggest banks falling, leading to the implementation of capital controls.

As Iceland gradually reopened its economy, it implemented a capital flow management tool last year. This forced foreign investors in króna-denominated assets to hold 40% of the value of their investment in a non-interest generating account for a year. By reducing the potential return for foreign investors, Iceland made its assets less attractive to them.

Traders argue that opening the economy up to speculators now will reduce market volatility and increase stability. The Central Bank of Iceland (CBI) may be inclined to agree, having been encouraged by the market’s reaction to the steps it has already taken in recent months.

|

Hauksson believes the CBI is likely to remove the final restrictions on króna trading quite soon. “The króna is volatile but I think that the problem would be reduced by allowing speculators to trade it again,” he says. “It is difficult to exchange opinions on the currency without speculators in the system. More speculation means more liquidity, which smooths out seasonality and reduces volatility, but since the capital controls were abolished earlier this year, liquidity has fallen sharply in the FX market, mainly due to the absence of speculators and also because the Central Bank has stopped intervening.”

But Stephen Brown, European economist at Capital Economics, says the central bank must take further steps before it can fully normalize currency trading. “Before the Central Bank of Iceland removes restrictions on speculation it will want to remove all the other remaining restrictions on trading, such as those on derivatives trading that make it difficult to hedge króna positions,” he says.

Capital controls have been gradually eased in four phases over the last 18 months. In June 2016 the CBI began by offering to buy back króna assets that it had locked up in non-interest accounts at around a 30% discount to the market rate — an offer many investors keen to unlock funds took up.

Then in October 2016 it raised the limits imposed on króna trades, before lifting them again in January 2017. In March this year it removed all limits on the size of króna positions. Having taken only 10 months to take off these capital controls, observers see no reason for the CBI to delay taking the last step. The IMF, which would surely have criticized the capital control tool more strongly if it had been implemented in a larger economy, will also no doubt approve.

Caution is key

Iceland’s relatively small economy and bureaucracy have made it easier for the CBI to take and implement decisions quickly. But the flip-side is that its small market capitalization makes it particularly vulnerable to speculators: individual traders with large positions can move the Icelandic market single-handedly.That makes it important for the CBI to be cautious. It is likely to remain particularly vigilant in monitoring the issuance of króna-denominated eurobonds, as this played a big part in inflating Iceland’s bubble pre-crisis.

Such bonds could be appealing in the current market as there is an attractive interest rate differential between the króna and the euro, with Iceland offering 4.25% for deposits, compared to the negative rate of 0.4% the ECB is charging.

Iceland’s economy looks generally healthy. At 3.7%, growth remains strong – though it has fallen from its highs of 5.2% – and it has large FX reserves compared with 10 years ago. All this looks positive for the króna.

“I expect there will be some interest in speculative trading of the króna once restrictions have been removed, but it won’t get to levels it would have if they had been removed two years ago when the króna was seen as a one-way bet,” says Brown. “While interest rates are still relatively high, the economic outlook around Europe has picked up, and rates in Iceland have come down a bit, so the divergence is not so extreme. While there is money to be made trading króna, market illiquidity means it is expensive to hedge.”

Brown adds: “The real interest in Iceland is likely to come more from foreign direct investment than speculation. There are real opportunities, especially in tourism and property, which can deliver strong, stable returns.”

The tourism industry, in particular, has benefited from currency moves in the last decade, as the collapse in the króna made visiting Iceland cheaper. Is more recent rise has eroded this advantage, but the increased number of flights and hotels in the country has kept visitors coming.

The economy therefore looks to be in good shape to take this final step in normalising currency trading.

“The Icelandic economic cycle usually ends with a sharp fall in the króna as a result of the net external trade position turning negative,” says Hauksson. “Right now, between a booming tourism sector and steadily rising consumption, it has grown between 4% and 5% this year. So even though the balance on goods is turning more negative, the current account is still significantly positive, which results in a positive trade balance and gives good support for the Icelandic króna alongside a large Central Bank FX reserve.”

While most accept that the króna played a big part in Iceland’s 2008 crisis, it has also been a big reason for the country’s resurrection, says Hauksson. “Having an independent currency that could depreciate allowed asset prices to adapt quickly. That was a painful process but the correction was over faster than it was in most other countries, and it meant the correction came in the asset markets, not the labour market. It means Iceland is economically stronger now than it was in 2006-2007,” he says.

Since then Iceland has also established itself as one of the world’s pre-eminent bitcoin hubs. The abundance of cheap, geothermal energy in the country has led to a big proportion of bitcoin mining taking place there.

Icelanders have also been keen early adopters of the cryptocurrency as a means of payment, perhaps partly because of their chastening experience with their official currency. Popstar Bjork recently made headlines by accepting bitcoin as payment for her new album.