Currency volatility is a cause for concern for any multinational company, but extreme volatility in EM currencies is spooking treasurers.

Jeremy Monnier, global head of FX solutions at Deutsche Bank, says: “Not only have [EM] currencies lost value and become more volatile, they have become more difficult and expensive to hedge.”

The dilemma facing EM currencies is that their respective countries have accumulated considerable dollar-based debt over the course of the past few years, says Paul Chappell, founder of currency management firm C-View.

“As the economy shrinks and they seek to repay down some of that debt, they are using up reserves to prevent their currencies from deteriorating too rapidly,” he says. “None of this makes you feel particularly bullish.”

|

2016: EM currencies vs US dollar |

|

|

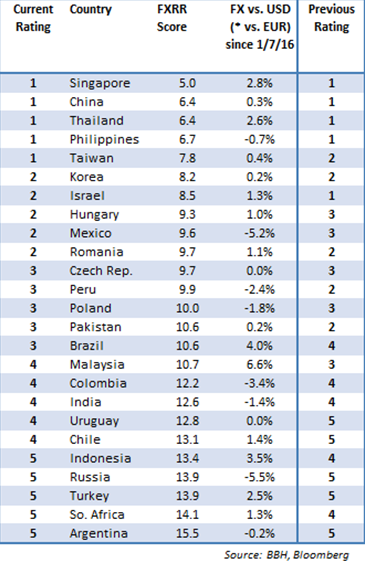

The 10 countries that are at the top of our table have |

Weaker currencies means that, for example, a US-domiciled company with revenues in EM countries such as South Korea will get hit when translating those revenues back into the US dollar. Some countries’ currencies have rallied in recent weeks against the dollar, including the Thai baht and the Malaysian ringgit, but currency experts remain cautious on this bounce from a low base.

Chappell says: “The fundamentals in emerging-market currencies are not too poor, but whilst we have got these capital movements and debt issues, it is much harder to see these currencies really recovering on a substantive basis.”

Furthermore, currency volatility can be a major risk factor in a company’s key metrics such as those set by rating agencies, says Satu Jaatinen, head of global corporate solutions at Commerzbank. She advises treasurers to take a two-pronged approach.

“Sometimes hedging emerging markets can be very expensive, sometimes quite cheap,” she says.

“It is good for the companies to be aware of the discrepancies between the two extremes and be ready to act accordingly: hedge when hedging is cheap and either refrain from hedging or hedge in the short term or via options, when expensive, in key metrics terms.”

The Brazilian real, Russian rouble, Chinese yuan, South African rand, Mexican peso and Turkish lira are particularly troublesome currencies for treasurers.

However, in many EM markets, interest rates in China are prohibitively high to engage in hedging.

Commerzbank is working with local treasurers at industrial manufacturers in China that need to hedge illiquid currency pairs, such as the Chinese yuan against the Brazilian real.

Previously, these hedges were done in US dollars. Now they need to consider a cross, which is not necessarily available in the market, and whether they should buy two options or an option plus a forward.

SABMiller

Forward contracts are the main hedges of choice for brewer SABMiller, which operates across six continents in far-flung countries such as Honduras, Mozambique and Moldova.

Forwards allow a company to lock in today’s exchange rate for a future currency purchase, thus guaranteeing a set exchange rate. This is SABMiller’s preferred route for its transactional exposures, such as importing raw materials to brew beer, according to UK-based treasury manager Tom Gilliam.

SABMiller’s policy is to layer in FX forwards over the course of up to 18 months. During that period, it enters into hedges every month or every other month.

“We apply that principle everywhere where we can, but [there are] quite a lot of countries where there simply aren’t FX markets going out to 18 months, or markets are so illiquid it is extremely expensive,” he says.

|

|

Satu Jaatinen, |

Forwards can be prohibitively expensive for some companies. A corporate treasurer that wishes to buy one-year protection against the depreciation of the Brazilian real versus the euro with a forward contract will typically have to pay a cost of 13.5% of the total amount. Some banks have developed dynamic solutions that offer a bit more flexibility. Deutsche Bank offers automatic rolling collars; the bank claims that volumes have increased more than 500% in the past year on the back of growing client interest in hedging EM FX risk.

Deutsche’s Monnier says: “The strategy has been used successfully by a wide range of companies across Europe; eg, with one company saving €30 million on a hedge for its Latin American, Eastern European and Asian currency exposures.”

Firstly, the hedge is broken into a shorter period, one month for example, instead of a year, so that the cost is 1% instead of 13.50% as in the case of the real.

Secondly, treasurers monitor market trends and only enter such expensive protection when necessary. For example, if a certain currency is rapidly depreciating, they might enter a forward. Otherwise, they might stick to a cheaper solution, such as a collar.

This only hedges outside a certain band, so if the currency doesn’t move then there is no hedge. If it depreciates, a hedge kicks in. If the currency appreciates, the treasurer will benefit up to a certain point, after which they pay a fee.

Automatic rolling collars take this strategy one step further, by automating execution.