Changes to the allocation guidelines for state pension funds in Japan announced last week will prompt not only an increased allocation to equity, but also a much larger allocation to foreign assets.

The capital allocated to foreign assets will increase from 23% to a 40% target, once portfolio managers have implemented the changes to the benchmark in their portfolios. Of this, some 25% of the portfolio is to be allocated to foreign equities while around 15% comprise foreign bonds. This will take the assets under management invested abroad to $1.3 trillion for the Government Pension Investment Fund (GPIF) alone, and $1.6 trillion if the smaller state pension funds follow suit.

Despite the changes to the benchmarks being bigger than many market observers had expected, there is some uncertainty as to whether, and how quickly, pension fund managers will rebalance their portfolios, although low bond yields domestically suggest greater offshore exposures would be a highly appropriate strategy. “Pension funds have thus far not rebalanced their portfolios on a large scale, even though regulations allow them to increase their holdings of risk assets,” says Shinichiro Kadota, FX strategist at Barclays, presumably because fund managers remain unconvinced about the benefits of doing so.

However, Kadota believes the latest announcement will give them the jolt they need to act, with smaller public funds following the GPIF, and private pension fund managers following suit.

“The market impact will depend on how long it takes to effect the portfolio shift,” says Arindam Sandilya, FX strategist at JPMorgan. “If the entire reallocation happens within one year (unlikely), GPIF may need to sell as much as ¥20 trillion [$174.4 billion] of JGB and buy ¥10 trillion of domestic stocks and ¥10 trillion of foreign assets. Nonetheless, the scale of the outflows is large enough to induce material yen weakening.”

"It will take around 15 to 18 months for GPIF to complete the shift in allocations into foreign assets,” says Yujiro Goto, senior FX strategist at Nomura. “It will commence immediately as pension funds look to avoid the potential losses that will come from their JGB investments as domestic rates start to rise."

“To put the potential outflows from the GPIF into the context of Japan’s overall balance of payments, a 4% increase in its benchmark portfolio allocation to foreign assets, from the current 27% to 31%, would represent an outflow of ¥5 trillion,” says Kadota. “Such a capital outflow would surpass the expected rise in the current account surplus to ¥3.2 trillion in FY2014 from ¥1 trillion in FY2013 that our Japan economics team is forecasting.” This should contribute to keeping the yen weak against the greenback for the foreseeable future, he says.

“Increased allocations to foreign assets could be significant enough to make a difference to push the yen down against the dollar,” says Goto. “Japan's annual deficit is ¥10 trillion so a ¥20 trillion shift of assets abroad is very significant.”

Pension funds are grabbing the headlines, but Kadota says life insurance companies will also prove influential for yen levels. “These institutions are not only a potential source of direct outflows into foreign assets, but we think their FX hedging behaviour could change as the Federal Reserve begins to normalize US short rates,” it says.

Kadota believes life insurers will increase their risk appetite in 2014 with M&A activity and unhedged foreign bond investments, repeating their behaviour in Q2 2013 after the first quantitative and qualitative easing announcement.

As US rates rise, the cost of hedging foreign-currency bond investments will increase, says Kadota, leaving companies with the choice of either holding foreign bonds unhedged or returning to Japanese government bonds. “When considering each company’s risk preference and the expected level of JGB yields one year forward, we believe more companies could opt for the former,” he says.

With the foreign bond holdings of Japan’s life insurers worth around ¥50 trillion, a reduction of the hedge ratio from 70% to 50% would equate to a portfolio rebalancing of approximately ¥10 trillion, says Kadota – further contributing to yen weakness. However, again the change is expected to be very gradual and will not trigger a sudden yen weakening.

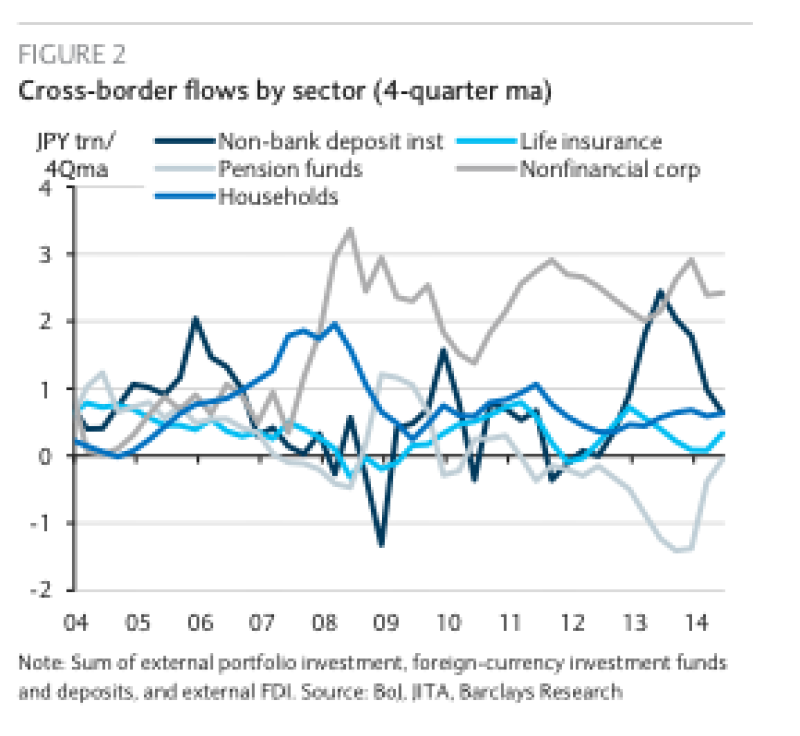

And then there is archetypal retail investor Mrs Watanabe, who already has a taste for foreign assets, although the share of foreign-currency assets in households’ balance sheets has actually dipped since before 2008. The share of foreign assets was 2.5% in June 2014, compared with the pre-crisis peak of 2.9%, suggesting allocations to foreign assets might rise again.

There are reasons to believe some of this increase might come before the end of the year. “Japan introduced individual savings accounts up to the value of ¥1 million but the entitlement cannot carry over into the next year,” says Goto. “It isn't clear exactly how much of this potential investment is still to be allocated but it looks like there could be a rush of investments in November and December, as utilization ratio is likely to still be at about 30%.”

However, the likely beneficiary of increased allocations has changed compared with what might have been expected in the past. “Retail investors used to prefer the high-yielding currencies until relatively recently, but now they clearly prefer US dollar exposure to emerging market currencies,” says Goto. “According to Nomura individual investor surveys, the former popularity of the Brazilian real has declined and even currencies like the Australian and New Zealand dollars, which deliver more yield than US dollars, are less popular than they were back in 2007-08.”

There have been some isolated pockets of interest in emerging markets. “In the past, India wasn't popular at all, but in the last three or four months we have seen an increasing interest in India and to a lesser extent Turkey,” says Goto. “With the new government in India it is a simple story for salespeople to sell and retail investors to understand. But this is very limited compared with the interest in US dollar assets.”

The most popular mutual funds have been the global infrastructure-related equity funds denominated in US dollars, adds Goto.

The sensitivity of Japanese retail investors to global interest rate expectations once again demonstrates their sophistication. “Retail investors focus on countries where there are expectations for rate hikes, and therefore a higher exchange rate,” says Kadota. “The New Zealand dollar was very popular at the start of the year but flows slowed down as soon as the Reserve Bank of New Zealand stopped hiking rates.”

However, while Mrs Watanabe has been positioning for US rate rises and exiting emerging market currency exposure, “the Japanese household sector has also been slowly shifting into riskier assets since Abenomics began in late 2012, a trend that is likely to continue,” says Kadota.

Taken together it all spells continued weakening of yen against the dollar – and also probably against euros.

“I expect the yen to weaken against the euro as the Bank of Japan expands its balance sheet much faster than the European Central Bank,” says Goto.

But although many in the markets have welcomed the GPIF's benchmark changes and increased appetite for foreign securities in Japan generally, there have been isolated words of caution. “Japan wants to boost the returns on its pension funds, but may achieve quite the opposite,” says Axel Merk, president and CIO of Merk Investments. “In the short term, yes, both domestic and international equity prices soared. But the new allocation has only been announced, not implemented. As such, the pension funds will buy assets at elevated prices. And because Japan’s population is ageing, odds are that they will be net sellers rather than buyers over time.”

Merk believes if Abenomics succeeds in its aims, Japanese government bonds will sell off, yields will spike and Japan will find it increasingly difficult to service its debts. The changes to GPIF could therefore be evidence Japan is preparing to “default”, he says.

“By buying foreign assets, Japan is ready to debase the value of the yen further, while trying to preserve the purchasing power of those assets,” says Merk. "We consider Japan’s recent moves deeply troubling acts of desperation. In our assessment, Japan signals it wants to move its pension assets offshore as it prepares for a default."