Markets cannot price geopolitical risk.

Strategists and bankers can debate whether commodities, real estate, infrastructure, gold or crypto are the best assets to hedge against inflation.

They can talk for hours about the impact of rising rates on equity risk premia, valuations and all of that.

They can model the likely percentage point price fall on a long-duration government bond from a one basis point rise in policy rates, as easily as breathing.

They can argue that rising spreads on high-yield bonds don’t reflect the substantial cash resources borrowers secured during the Covid panic and the high average credit quality of the broad asset class.

But when analysis suddenly runs to the chances of a nuclear war between Russia and Nato, minds go blank.

The uncertainties are too extreme and the tail risks too devastating for analysts, bankers or investors to capture.

Markets, after all, consist of people buying and selling, even if they do unleash algorithms powered by artificial intelligence to read the price signals and to automate execution of the trades.

Astonishing failure

As Russian forces massed on Ukraine’s borders in February, most equity and bond investors ignored them, assuming even after the US government warned on February 10 that an invasion was imminent, that there would be a diplomatic solution because that would have been economically and financially rational.

In retrospect, it was an astonishing failure.

They focused instead only on the words of central bankers weighing the speed and quantum of the coming response to persistent price increases.

In a speech on March 21, Jerome Powell, pro tempore chair of the Federal Reserve, reflecting on how the rise in inflation has been much greater and more persistent than “forecasters” had expected, pointed out: “The inflation outlook had deteriorated significantly this year even before Russia’s invasion of Ukraine.”

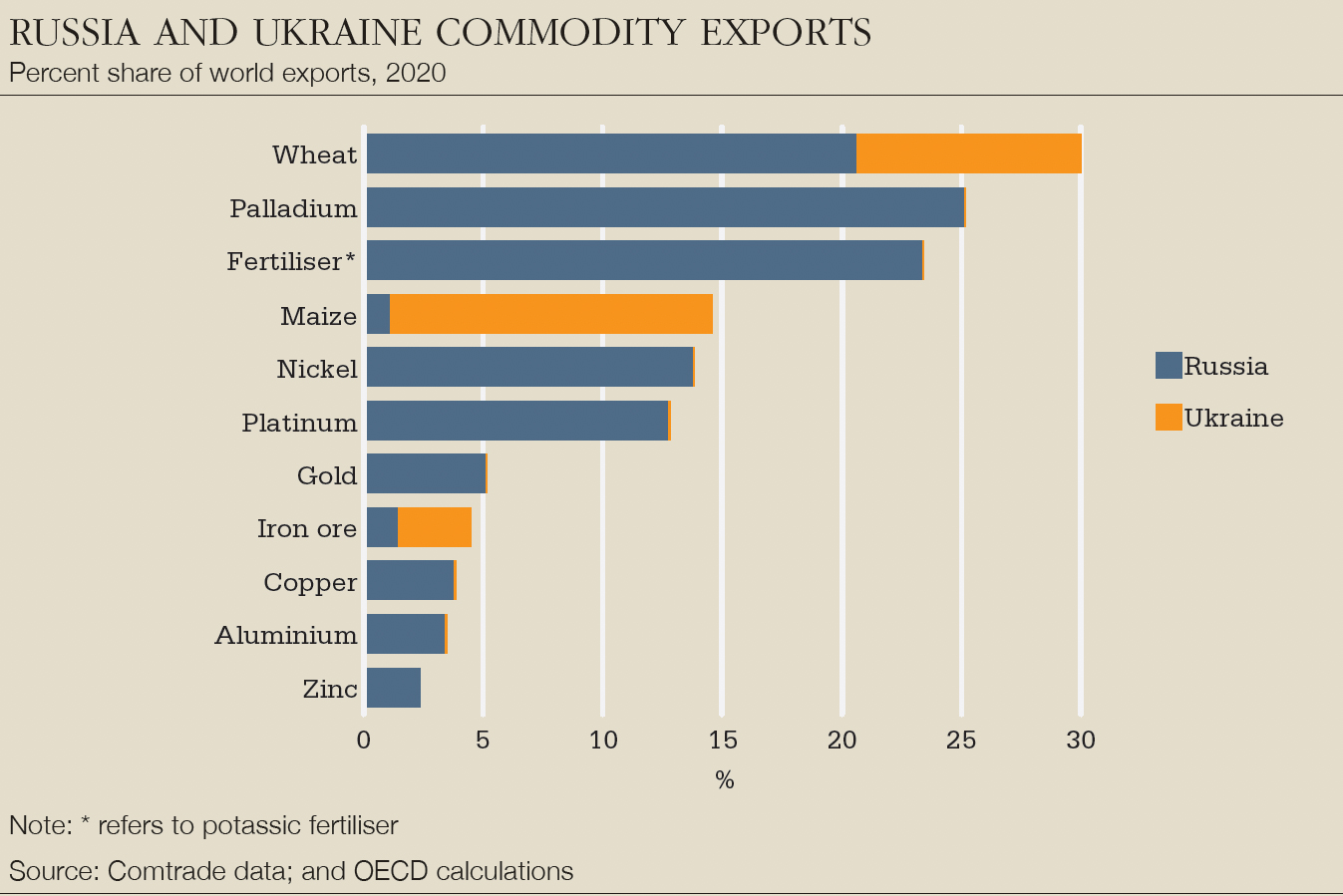

Underlining that while Russia is a leading energy exporter, Ukraine is also a key producer of wheat and of neon gas, which is used in the production of computer chips, Powell admitted: “There is no recent experience with significant market disruption across such a broad range of commodities.”

In addition to the direct effects from higher global oil, food, metals and other commodity prices, Powell said: “The invasion and related events are likely to restrain economic activity abroad and further disrupt supply chains, which would create spillovers to the US economy.”

Investors didn’t want to hear about the war. They turned their attention to his statement that the Fed might move aggressively and raise the federal funds rate by more than 25 basis points at a meeting or meetings. Markets are starting to price in 50bp hikes in May and possibly June.

The read of financial markets is that the war will bring what the war will bring. It is possible to model for the kind of relief rally that took hold in March if there is a surprise early resolution, and even for prolonged fighting contained within Ukraine. But a war with Nato is too much to contemplate.

“The volatility we have seen since the war began reflects very small changes in how investors see the probability of coming to such extreme outcomes,” one banker tells Euromoney. “It does not even come close to actually pricing in those outcomes.”

The big news is that rates are going up, perhaps far and fast. One month into the war and markets seem almost to be ignoring it.

The volatility we have seen since the war began reflects very small changes in how investors see the probability of coming to such extreme outcomes. It does not even come close to actually pricing in those outcomes

A banker

Instead, by late March, financial markets are simply folding this murderous assault on a sovereign nation back into the inflation story.

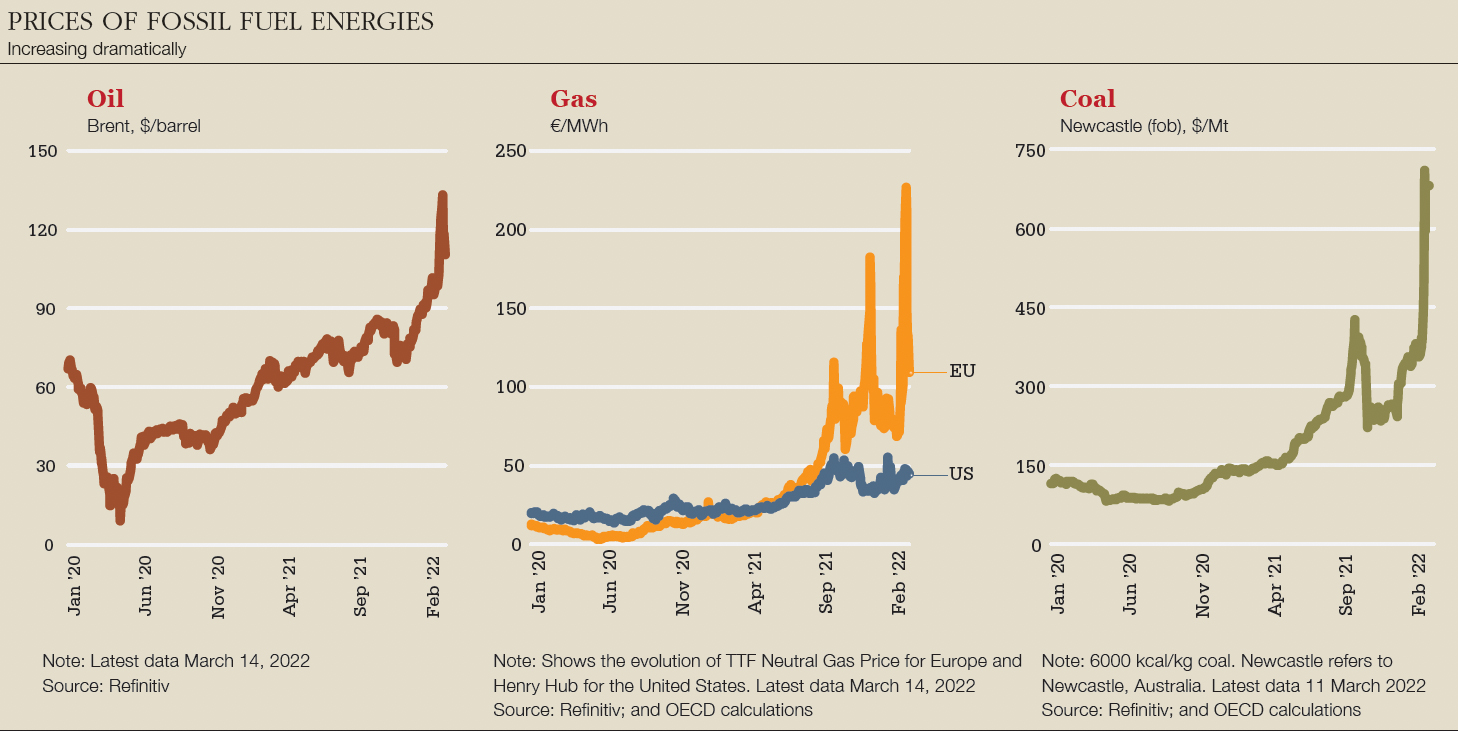

In the month since Russia’s attack, financial markets have been a little volatile, while most of the action has been in oil markets. The oil price rose from $80 at the start of this year to $133 early after the invasion, before settling back to around $120 on March 23. That was ahead of the meeting between US president Joe Biden and European leaders to devise policies for reducing European dependence on Russian energy.

There have been big intraday swings on any suggestion of increased production from Opec. It would seem rational that the higher price will spur increased production somewhere. It is also possible that slowing economic growth in leading importers will curb demand, as China locks down certain manufacturing centres once again in pursuit of its zero-Covid policy.

The International Energy Agency – set up in 1973, let’s remember, after a previous oil-price crisis – issued a 10-point plan on March 18. “As a result of Russia’s appalling aggression against Ukraine, the world may well be facing its biggest oil supply shock in decades, with huge implications for our economies and societies,” said IEA executive director Fatih Birol.

Recommendations include working from home three days a week, which no longer seems radical, given the recent rise of Covid cases around the world; avoiding business travel where other options exist, such as Zoom, presumably; making public transport cheaper; and reducing speed limits on highways.

There has been a so far mild correction in clearly over-valued equities, although one that disguises at times considerable intraday volatility.

The NYSE Fang+ index of leading US technology stocks was down 12.7% for the year to date up to March 22, after a relief rally had brought it back from a 28% fall for the year up to March 14.

“Just before the war, markets began correcting, starting with the most expensive and longest duration assets, that were the leaders in the last cycle,” Peter Oppenheimer, chief global equity strategist at Goldman Sachs, briefed on March 14, explaining why the biggest falls had come in baskets of unprofitable technology stocks.

The expensive US equity market is weighted towards technology and growth: Europe towards value, which is why it is cheaper. At the start of the year, there was a rotation into value and Europe. That has since stalled.

Goldman Sachs has cut its 2022 growth forecast for Europe from 4% to 2.5%. And while 2.5% sounds healthy, that comes from base effects and the recovery from Covid lockdowns.

“Europe is flirting on the edge of recession, and it wouldn’t take much to push it over,” Oppenheimer says, “for example, if we had a cessation of gas supply to Europe.”

The S&P500 index was down 6.2% for the year to March 22. The EuroStoxx 600 was down 6.5%.

“We still see a path to markets ending the year higher,” Mark Haefele, chief investment officer, UBS Global Wealth Management, said on March 23, referring to Powell’s speech two days before rather than to the war. “Although there is widespread criticism, it’s too early to take the view that the Fed won’t be able to negotiate the fine line of reducing inflation without derailing growth.”

Sell-side analysts say that this is a time to actively manage underweights and overweights and take a neutral position on equity market risk, rather than allocating to cheap, passive market beta.

Of course, as new issues, IPOs and M&A fees shrink, that kind of active management chiefly benefits the sell-side.

A brief flight to safety in government bonds took the yield on the 10-year Treasury note down from 2% on the eve of the invasion to 1.725% at the start of March, followed by a speedy sell off, as attention turned back to dot plots and quantitative tightening. The 10-year hit 2.4% on March 23. The yield on two-year notes had risen 75bp this year to March 23, with the one-year forward rate for two-year Treasuries reaching 2.78%.

There have been extreme stresses in particular financial markets that required speedy resolution, for example in FX swaps with legs in Russian roubles which became almost impossible to deliver

There have been extreme stresses in particular financial markets that required speedy resolution, for example in FX swaps with legs in Russian roubles which became almost impossible to deliver. Facing the potential for billions of dollars in losses, the world’s biggest banks came together to agree compression of these trades to reduce settlement amounts.

Goldman Sachs points out that financial conditions tightened noticeably in the days immediately following the start of the Russian invasion on February 24, with its euro-area financial conditions index rising by almost 40bp. By March 23, however, we had seen an easing in financing conditions once again, driven largely by the rebound in stock indices and an improvement in the trade-weighted euro exchange rate.

The lingering effects seem to be felt most in Austria, Italy and Finland.

Electricity usage data does not yet suggest a decline in manufacturing, even though worries are growing that shortages of components might disrupt car-making, for example.

Economic consequences

While financial markets gyrate, three weeks into the war, three million people had already fled the merciless shelling of civilians in Ukraine’s cities, with the OECD predicting that at least as many again would soon follow them and maybe millions more in a wave of refugees not seen in Europe since World War II.

With Poland already taking 1.8 million of the first to leave, government spending must increase to cope, just as debt service costs are rising. Could there be six or seven million refugees, 10 million, maybe more? No one knows.

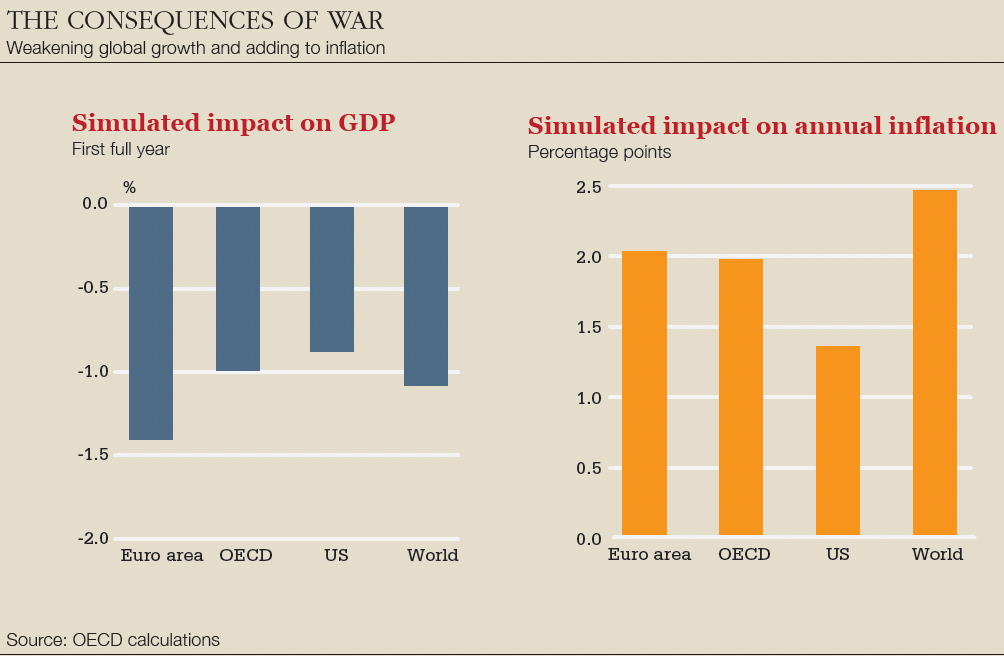

The latest OECD economic estimates released on March 17 are bleak, but they don’t look so very alarming. It suggests global economic growth could be more than one percentage point lower this year than it projected before the conflict, and 1.5 percentage points lower in Europe.

Goldman Sachs estimates that if Russian gas stops flowing completely to Europe, the economic hit this year could be a further 2.5 percentage points. Even without that, it has cut its profit growth forecast for European companies to 2% in 2022, compared with 8% before the war. It has cut its profit growth forecast for the S&P500 to 5%, also from 8% previously.

Meanwhile, the OECD says inflation could be higher than it would have been if war had not broken out, by at least a further 2.5 percentage points on aggregate across countries.

War is stagflationary.

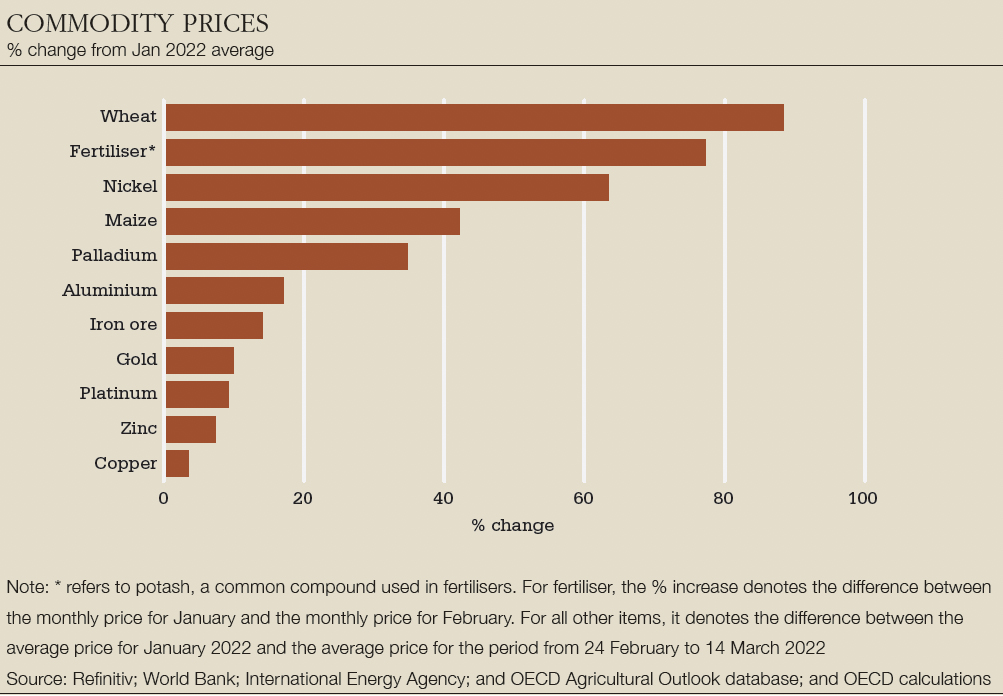

But with developed-world central banks already so far behind the curve on inflation, they risk all credibility if they pivot back from their recent hawkish turn and continue to accommodate, even as wheat prices double, fertilizer prices are up 80% and it becomes obvious that, at the very least, the poorest in developed markets as well as in emerging markets will need some protection from rising food and energy costs.

Price rises will crimp household budgets and reduce demand for goods and services, while rising input prices, including labour costs, also eat into corporate margins and reduce profits.

The valuation multiple that investors place on those declining profits is also set to shrink. Higher discount rates imply a much lower net present value on future corporate earnings.

We have been surprised by the lack of reaction of financial markets, which might be part of the overall uncertainty

Laurence Boone, OECD

“We have been surprised by the lack of reaction of financial markets, which might be part of the overall uncertainty,” says OECD chief economist and deputy secretary-general Laurence Boone.

The OECD advocates higher government spending, including perhaps EU burden sharing, to support neighbouring countries taking the most refugees from Ukraine and means-tested support to spare vulnerable households from the worst of rising food and energy prices.

Looking further ahead, the war emphasizes the urgent need to mobilize private and public investment in energy efficiency and clean energy so as to reduce Europe’s dependence on Russian natural gas and oil.

Strategists at Bank of America calculate that annual European defence spending could rise by between €150 billion and €200 billion. They add that inflated gas and energy prices mean that high energy-intensive industries could be priced out and will need to leave Europe. For local ones (such as cement), it means more margin pressure and price rises.

They suggest that the Russia-Ukraine conflict will have far-reaching effects that look set to redefine many megatrends in Europe: “We believe it is one of those rare events in history that will reshape geopolitics, societies and markets. Europe will transition to be more independent and redefine many of its sectors and economic paradigms.”

The sell side is now starting to suggest some longer-term winners to investors, for example in defence and energy transition, as well as losers in retail and real estate.

In the short run, “should financial markets become more shaken, then central banks do have a role in stabilizing them,” Boone says.

Guy Wagner, chief investment officer at Banque de Luxembourg Investments, notes that the factors behind the inflation of financial asset prices over the last few decades are now starting to reverse.

Most obviously, the post-Cold War peace dividend is disappearing. The pandemic and now war in Ukraine have shown the dangers of an economic model based on efficiency at the expense of security. The era of globalization is giving way to an era in which economic and commercial relations will once again be conditioned by national security concerns.

He writes: “The downward movement in interest rates that began in the early 1980s has come to an end. All this at a time when valuation multiples are high and irresponsible central bank policies have encouraged a massive move into risky assets.”

That is why it might be wise to use the recent recovery in markets to buy some insurance against those unquantifiable tail risks. It is not just that markets moved back up in mid March: volatility came down, making options cheaper.

Goldman pointed out on March 22 that while three-month implied volatility is historically high, since the VIX peak on March 7, it has come down by more than three standard deviations for the main equity indices and for European assets where uncertainty risk premia were particularly elevated in the days after Russia invaded.

The relief rally is certainly at odds with its read of downside risks, while the firm also sees little upside based on its economists’ base case.

Before the war, investors might have hoped that rising growth would bail out markets from the hit of rising rates to combat inflation. The war will increase inflation and lower growth. That’s a bad mix.

And if this is a radically new cycle, we go into it with stocks still at very high valuations, nominal bond rates still far below neutral, and credit spreads not far above historic tights.

Oppenheimer says: “We had been used to a very deflationary world for a very long time. After the global financial crisis, banks de-levered their balance sheets, companies reduced debt and investors focused on growth because it was so scarce. Now, margin-sustainability is going to be much more important for investors.”

In its assessment on March 21, Goldman reported that the initial investor pessimism that greeted the outbreak of war had faded materially.

It’s hard to see why.

On March 23, Bjarne Schieldrop, chief commodities analyst at SEB, pointed out that while the IEA and others have already warned about looming losses of oil supply, the market isn’t really pricing it, hoping that Russian oil will keep flowing under the radar to India and China.

Brent averaged $100 to $120 a barrel from 2011 to 2014 during the Arab Spring. In today’s money, that is around $120 to $145 a barrel. And the world coped.

But this could be worse. “Continued curbs have the potential to drive oil to $200 per barrel,” writes Schieldrop, or even higher. It can’t do that without “breaking the global economy”.

And if Putin should next attack an EU country or a member of Nato?

Perhaps there’s a reason why the people paid to manage our money live in their metaverse of models.

It’s pure escapism.

Markets have looked resilient so far. But confidence hangs by a thread.