Currency markets were sent into convulsions by the UK's decision to leave the EU. And while volatility has since calmed somewhat, further bouts are expected as officials thrash out the terms on which Brexit will be delivered.

With this in mind, businesses want to reduce their cashflow at risk and protect margins, says Matthieu Brunet, director of risk management solutions at Citi. “Given the uncertainty around future cashflows, many are looking at a more layered, progressive approach to hedging,” he says.

This may also mean changing the types of instruments used, says Brunet. “Some products, such as combinations of options, are more suited to the higher volatility environment, so corporates can look at using that to their advantage. At the moment, in GBP/USD it is cheaper to buy calls than puts.”

|

Citi published a paper, co-authored by Brunet, advising its corporate clients about managing their FX risk following the UK's Brexit vote. When discussing its Q2 numbers, the bank's CFO John Gerspach told analysts the bank now makes more than 40% of its rates and currencies revenue from corporate clients, a proportion he reckons is higher than at competitors.

“The benefits of using options are that they can help to mitigate the earnings noise that comes from derivative mark-to-market volatility, and in a scenario where a corporate has already incurred earnings translation losses they may be an attractive way to hedge while maintaining the potential to benefit should FX rates subsequently move favourably,” Citi says in the paper.

Citi notes that in the aftermath of Brexit, sterling fell more than 18 cents against the USD within days, trading from 1.4990 down to an intraday low of 1.3000 on Tuesday July 5th. The June month-end close of 1.3311 is the pair’s lowest point in over 30 years.

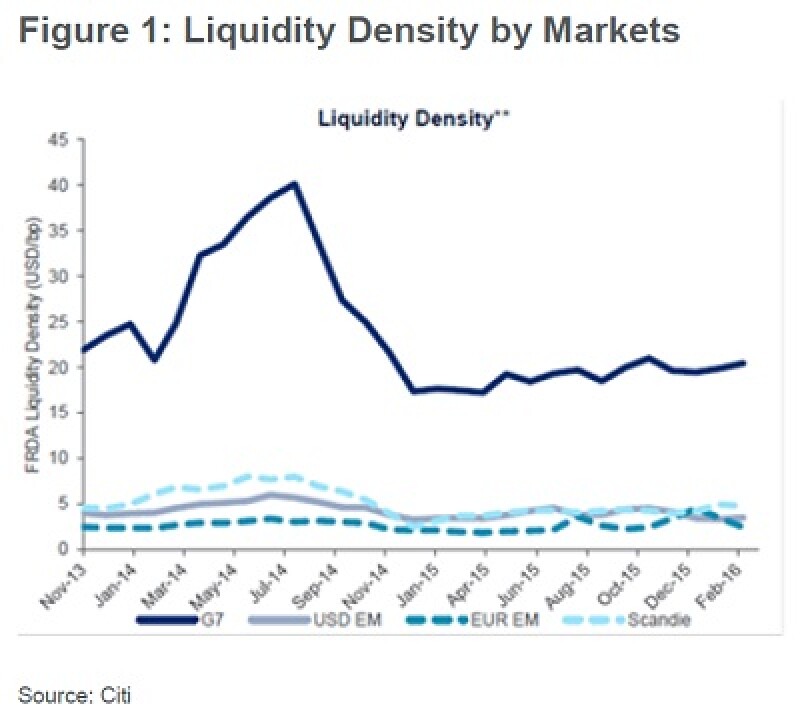

Part of the reason for the move was illiquidity, says Citi, which in the weeks leading up to the referendum was already 50% below the 2014 peaks in G7 currencies. “Our electronic traders estimate that liquidity dropped an extra 80% on June 24th and retraced in the following days to 70% of pre-Brexit levels,” says the bank.

The Brexit vote has given many corporates “a sense of déjà vu from the 2008 credit crisis,” Citi says, reminding risk managers of the importance and benefits that can be secured by having a disciplined counterparty credit risk programme.

Stephen Baseby, associate policy & technical director at The Association of Corporate Treasurers, says: “In the short term, many of our members have hedging protection so the volatility is not an immediate concern. But these hedges will run off in due course, so there is a problem there.”

Erik Johnson, director of risk management solutions at Citi, who also co-authored the report, points out that some corporates “face a situation where the hedges they put on before Brexit are now out of the money. Hence, the use of optionality, for some, is a more effective way to hedge exposures in this volatile environment.”

But the impact of the current currency market volatility will depend on the nature of a specific business. Many businesses involved in importing and exporting and relatively dollarised, giving them a natural built-in hedge.

|

The impact is most acute for businesses whose supply chains are outside the UK but who rely heavily on UK sales. For those importing parts, assembling in the UK but selling predominantly outside the UK the effect of currency volatility is relatively muted, with the potential benefit of reduced costs for the UK part of the business.

But while some benefit and some lose out, “we are making broadly similar recommendations for corporates that have either benefited or been negatively impacted by the Brexit vote,” says Citi.

Baseby says corporates have to look far beyond the direct implications on their own businesses. “Many businesses are importing or exporting or manufacturing overseas. The impact of Brexit is not only being felt by the businesses themselves, but by their suppliers and their customers. Businesses need to understand the impact on them, but it is going to take more than a few months before this can happen,” he says.

Among the questions corporates are asking themselves is whether Brexit affects the efficiency of their capital structures. Citi says: “Many corporates have sought to raise foreign currency debt as a way to rebalance mismatches between foreign currency assets and liabilities.”

Baseby says: “Most businesses prefer to focus debt raising within a single entity to avoid structural subordination issues. Brexit means they may want to think about raising debt at the local entity level, but this means they do face the problem of potential structural subordination. Each business will have to look at its own capital structure, but overall it makes things more messy and more expensive. And this is the point at which companies may start to think about whether it makes sense to change their domicile.”

Passporting or Equivalence?

But it is not only corporates that are struggling with these issues. Banks had already been gravitating towards an increasingly domestic focus since the financial crisis, in response to increased pressure from governments to serve local markets. Now there is concern that Brexit could accelerate this trend, if the settlement makes it hard for banks based in the UK to access the EU market.

Baseby says: “There is a real concern around financial services and continued access to the large pool of banks we have in the UK. This could have a real impact on the availability of things like interest rate derivatives and FX hedging products. Even the government does not seem clear about where things are going.”

Passporting — the current mechanism that allows firms authorised in one country belonging to the European Economic Area (EEA) to carry out activities in any other — is the ideal solution, but until now this has required an acceptance by the host state of the European Union principle of freedom of movement. So Equivalence — whereby a state’s regulatory regime can be deemed by the EU to be equivalent to its own, thereby allowing firms to access EU markets — might be more realistic, says Baseby.

“But deals on Equivalence can take a long time to arrange,” he adds. “It has taken four years for the US and EU to agree on Equivalence for CCPs, and that was supposed to be easy. And we wouldn't only need it for the EU, but for the rest of the G20 as well.”

Kit Juckes, macro strategist at SG, believes corporates need not worry too much about banks' commitment to London and the UK. “As far as the supply of hedging products is concerned, where there is demand there will always be supply and the financial industry will continue to find solutions to work around any problems that may arise from Brexit negotiations.”

But clearly the increased need for longer term hedging strategies comes at a difficult time for banks. Not only are they coming to terms with the impact of the vote on their own businesses, they are also being squeezed by increasing regulatory pressures. Basel and MIFID II make hedging instruments more expensive for them to provide.

So alongside the potential capacity issues, if banks withdraw from the UK market, and increased volatility, businesses face a triple whammy of escalating FX hedging costs.

Overall, however, Baseby remains cautiously optimistic that the situation for corporate treasurers will ease as time goes on. “We may not know the specifics of the Brexit deal for some time but we should soon start to get some clarity around the process. Even that will be helpful as it should give a sense of the direction of travel and timing,” he says.

Juckes agrees. “Businesses based in the UK have hedged their currency and other exposures for years. Yes they face more uncertainty now, but sterling volatility is already down from its June peak and uncertainty will continue to fall as negotiations continue, especially if Article 50 is triggered, or it becomes clear it will not be triggered,” he says.

“In the meantime investment decisions may be put off where possible, but changes to where manufacturing or sales take place are unlikely until the deal has been finalised.”