|

Super-fast data feeds and networks have reshaped the FX trading landscape in recent years, leading some market participants to question the integrity of the market structure, given the rapid pace of technological change, according to a white paper by Tradition.

The paper, seen by Euromoney, by Dan Marcus, global head of strategy and business development at Tradition, argues: “This emphasis on speed, rather than skill, was causing participants to lose faith in the integrity of the market, and created negative knock-on effects.”

|

| We haven’t seen quite the same level of arms race in technology innovation in FX that we saw in equities Andy Young |

Many traders had lost their focus on their original reasons for trading – risk management, currency hedging and ensuring global flow of payments – and were instead engaged in a technology arms race, says Marcus, as firms sought the fastest low-latency technology and to secure discounts with platform providers based on volumes traded.

No market segment encapsulates the existential and regulatory challenge facing the trading community better than high-frequency traders, which are often blamed for this distortion.

“[However,] it is unfair to paint all those who engage in HFT with the same dark-arts brush,” says Marcus, noting the benefits they have brought to the market: liquidity, reduced spreads and lower trading costs.

He adds: “Of course, there are valid concerns relating to certain trading strategies and behaviour that became prevalent in some cases, which played a part in creating an imbalanced and fragmented market.

“But it is less about the market segment and more about the intent and behaviour behind these trading strategies, which often rely on extreme low latency and superior access to market data in order to move the market, which need to be questioned and addressed.”

Blaming high-frequency traders demonstrates a misunderstanding of the market dynamics, he argues.

“In the same way that it is the drivers caught speeding that are held responsible for their actions, as opposed to the cars they drive, the focus needed to be on eradicating disruptive trading behaviour and the intent behind it, rather than the technology.”

This means other market participants must also share in the blame. The “inconsistent, opaque and asymmetric charging models” of some FX platforms also undermined confidence in the system, argues Marcus.

In fact, the problem is a little less acute in FX than in equities, says Andy Young, capital markets specialist sales director at Colt, adding: “We haven’t seen quite the same level of arms race in technology innovation in FX that we saw in equities. Latency is important in FX, but it hasn’t reached the same level of microsecond competition as seen in equities.”

Young says FX has the advantage of being a little behind equities, meaning it benefits from technologies that have matured in the equity market and are lower cost by the time they migrate to the currency trading market.

|

Different asset classes operate in different ways,

and there is no one-stop solution for all

Dan Marcus

|

The broker community has certainly taken substantial steps towards resolving some of these issues by innovating with trading technology itself. Tradition’s part in this has been to create ParFX, designed to create a level playing field for traders regardless of size, technological sophistication, financial clout or volumes traded.

This is achieved with some fundamental technological innovations such as a randomized order entry mechanism within the matching engine, delaying order submissions, amendments and cancellations by between 20 to 80 milliseconds. This removes the advantage held by low-latency trading strategies.

Spot FX market data are also distributed to all participants, with the cost included in the connection fee, and fees transparent and applicable to all.

Tradition is not alone in pushing these kinds of innovations. Speaking to analysts for its half-year results, Gil Mandelzis, the CEO of EBS, described the changes to his business in the past three years as essentially its transformation into a technology company – or “a supermarket for FX execution”.

The investment in technology has made the business more scalable and substantially reduced the time and cost associated with bringing innovations to market, added Mandelzis.

'Supermarket' environment

The emergence of a “supermarket” environment in trading is great news for investors and recognizes the variety of interests among the trader community.

Tradition’s Marcus says: “Different asset classes operate in different ways, and there is no one-stop solution for all.”

This includes voice or hybrid trading, which remains appropriate for larger or more complex or bespoke orders, requiring “a higher touch service, structuring and a level of potential opacity to avoid market impact. Machines, or electronic trading systems, cannot replicate this type of service.”

Alex McDonald, CEO at the Wholesale Markets Brokers’ Association (WMBA), says: “The changes individual platforms have made, such as randomizing order queues, setting minimum latency and increasing minimum tick sizes, shows regulation is not needed to create fair and effective markets.

“These changes can be commercially driven and tailored to what specific segments of the market need without the liquidity fragmentation which legislation always leads to. We are seeing distinct market functionality being built for wholesale traders, prime brokerage, retail and HFT.”

Smaller players that have felt disadvantaged by their own technological inferiority are looking to leap-frog to new technologies.

Colt’s Young says: “Smaller banks have the appetite to trade FX, but they want pre-built ecosystems in place that allow them to enter the market on equal terms with other institutions without breaking the bank on new technology.

“There is a definite appetite for outsourcing technology so that banks can focus more on trading strategies and less on latency.”

It should also leave regulators free to focus less on restructuring the market, which in practice only leads to ever-increasing discrepancies between the rules in different locations, and more on enforcing rules governing the conduct of market participants, say market players.

“The problems in the FX market relate to behaviour and conduct, not structure,” says David Clark, chairman at the WMBA. “This market has worked perfectly for decades.”

|

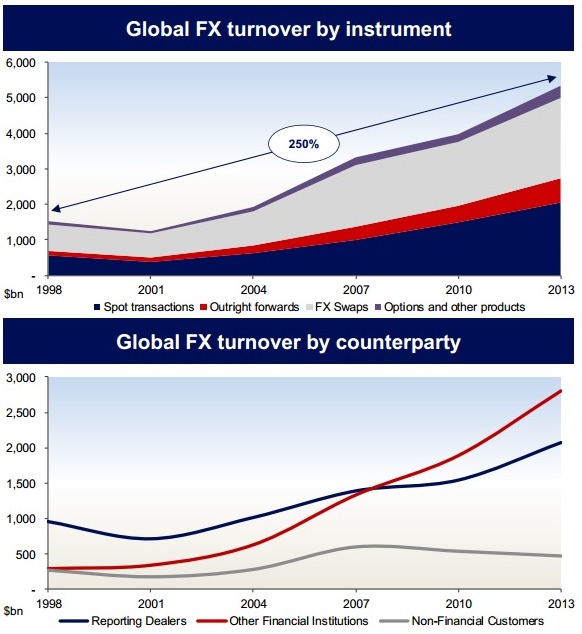

| Source: Icap |