|

See also |

|

Given that its own shares had fallen nearly 3% that day on the news, Nasdaq’s spokesman, Joe Christinat, was pretty cool when asked to comment on the launch of a new US equities exchange, the Members’ Exchange or MEMX, on January 7. “We welcome competition to our transparent, highly regulated equity markets,” he said, smoothly. “However, with dozens of equity trading venues already in operation in the US, we are keen to learn more about the value proposition of a new exchange.”

So was the market. The new firm’s stated aim is to offer a simple trading model with basic order types, the latest technology and a simple, low cost fee structure; but just how it plans to do so remains unclear. It has nine members: Morgan Stanley, Fidelity, Citadel Securities, Bank of America Merrill Lynch (BAML), Charles Schwab, E*Trade, TD Ameritrade, UBS and Virtu. There are many notable absentees, including Goldman Sachs and Citi.

“The primary focus of MEMX’s press release was on who it is, not what it is,” observed Kurt Dew, visiting lecturer in economics at Northeastern University in Boston, at the time. This was no accident and the weighty names involved in the project are key to its future success.

|

| Vlad Khandros, UBS |

“One of the ways MEMX differs from other exchanges is its ownership structure,” explains Vlad Khandros, global head of market structure and liquidity strategy at UBS, one of the consortium members. “It is owned by some of the world’s largest brokers, banks and financial services firms.” Little else has been revealed about the exchange. By mid-February the management team had still not been announced. Early rumours that MEMX was talking to Ronan Ryan, president of the Investors Exchange (IEX), were swiftly and vehemently squashed by the latter. An obvious candidate to head the venture was Joseph Mecane, head of execution services at consortium member Citadel Securities. He previously worked for the New York Stock Exchange (NYSE) as its head of US equities. However, on February 27 it was announced that Jonathan Keller, former chief executive officer of Instinet, Nomura’s electronic brokerage, will be appointed CEO of MEMX.

The key driver for the exchange is clear – cost. “The entity is intended to be for profit with relatively low margins,” Khandros tells Euromoney. “Some other exchanges have margins well into the double-digits so it seems feasible to be competitive and viable.”

This gets to the heart of what MEMX really is. It is the manifestation of the market’s exasperation with what it sees as oligopolistic pricing by the incumbent exchanges.

“Faced with declining trading revenue and increased competition, exchanges have turned to price-gouging the costs of data and technology,” observes Spencer Mindlin, capital markets industry analyst at Aite Group.

Dew at Northeastern University is less polite. “NYSE, Nasdaq and CBOE are reactionary market parasites,” he says.

Sarah Sullivan, analyst on the financial services team at policy analysis and regulatory due diligence research firm Capstone DC in Washington, explains the standoff from the incumbent’s point of view.

|

|

|

Sarah Sullivan, Capstone DC |

“The exchanges have tried to paint this debate as the exchanges versus Wall Street,” she says. “They argue that the cost of trading is lower than it has ever been and that they have had to invest so much in tech that this needs to be paid for.”

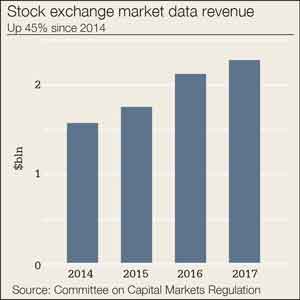

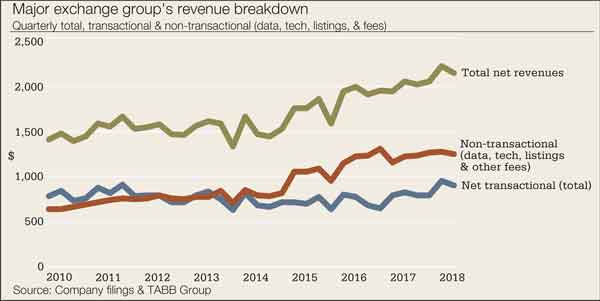

Their clients are certainly doing that. Revenues at these exchanges have grown by 5.4% per year since 2010, with non-transactional revenue (data, tech, listings and fees) now greater than transactional revenue. The number of brokers in the US has fallen by 24% over a similar period, according to Finra. So this growth in data revenue is being paid for by a shrinking pool of clients.

It was only a matter of time before these clients hit back. The exchanges were given a boost in 2016 when an SEC judge ruled the cost of market data is subject to competitive forces, but that has done little to quell the growing rebellion among those that have to pay these costs.

“This effort [MEMX] is real and should surprise no one,” states Adam Sussman, head of market structure and liquidity partnerships at trading and liquidity network Liquidnet. “The most puzzling thing is why it took so long.”

Larry Tabb, founder and research chairman at New York-based capital markets research and consulting firm Tabb Group, concurs. “This is standard practice in the industry,” he says. “When certain interests start charging too much, especially in a concentrated market, the brokers that use these services bond together and create competition.”

Competition

MEMX plans to do this by simply charging less than NYSE, Nasdaq and CBOE. There are two types of fees that the exchanges levy: access fees, which cover direct access to the securities information processor (SIP) feeds, (providing real-time consolidated feeds of top of book trade and quote data: the best bid price), and use fees, which cover display and non-display data.

According to a research paper published in August last year by Charles Jones, professor of finance and economics at Columbia Business School, a global investment bank with a wide range of trading activities that subscribes to all of NYSE Group’s proprietary integrated data feeds and the similar feeds for Nasdaq and CBOE in order to display limit order books, provide trading algorithms and support an affiliated dark pool, would pay $100,800 per month for NYSE data, $127,720 for Nasdaq data, and $37,000 for CBOE data (for 75 display-only devices and for non-display use in one non-display category). “This is an insignificant cost for these types of investment banks, which measure their annual equity trading revenues in billions of dollars,” declares Jones. The research paper was financed by NYSE.

“This debate has gone on for years in an echo chamber that lacks much objective data, because much of the data that would be helpful is known only to the exchanges.” -Brad Katsuyama, IEX

The crucial question, however, is what kind of margins the exchanges are making on their data feeds, which are simply regenerated from the trading activity of their own members. IEX, which does not charge for market data, caused uproar in the market on January 29 when it published a study examining how much it costs IEX to produce similar data and compared with how much the other exchanges charge.

The data was split into three: market data, physical connectivity and logical connectivity. The research found that for market data, which includes depth-of-book data products, other exchanges charged between 900% and 1,800% more than IEX’s costs. For physical connectivity, they charge 2,000% to 4,200% over IEX’s costs; while for virtual data sessions (logical connectivity) the charge is 500% to 1,800% more than IEX’s costs.

“Exchanges have forced customers into a fixed cost paradigm,” IEX head of communications Gerald Lam tells Euromoney. “Fees are subscription in nature, so you are on the hook at the beginning of every month. Our pricing is completely variable – you only pay when you trade.”

|

|

Brad Katsuyama, chief executive and co-founder at IEX, has long lobbied for more transparency on exchange costs.

“This debate has gone on for years in an echo chamber that lacks much objective data, because much of the data that would be helpful is known only to the exchanges,” he says. “It is not possible to determine whether these fees are fair, reasonable and based on competition without a basic understanding of the economics of these products and services – first and foremost, what does it cost the exchanges to provide them?”

Phil Mackintosh, Nasdaq’s chief economist, swiftly challenged the IEX numbers. “Even if we add the costs of colocation, data and trading per share for each of the exchanges, we see that the costs, including SIP allocations, range from 0.067 to 0.091 cents per share (6.7 to 9.1 mils). That is less than 10% of the average algorithm commission of 0.9 cents per share reported by Greenwich Associates,” he said, claiming “the ‘free data and colo model’ offered by IEX is the most expensive exchange on a per share basis.”

Growing acrimony

The fight over exchange pricing has rumbled on for years, but it increased in intensity over an ill-tempered two-day roundtable at the SEC last October.

|

| Larry Tabb, Tabb Group |

“The exchanges know that their members are not happy with them. The SEC meeting in October was pretty acrimonious,” reveals Tabb. Sullivan agrees. “The SEC roundtable in October was a very heated affair. The panel interrupted and talked over each other, which is very unusual for an SEC panel,” she tells Euromoney.

The row seems to have reached a tipping point. “The owners of the Members Exchange are the ones who have been paying rapidly increasing fees and are not happy,” says Richard Johnson, vice-president, market structure and technology at Greenwich Associates. “This is an indirect attack on the other exchanges.”

But is another exchange really the answer?

There are already 13 exchanges and 45 alternative equity trading systems in the US, so adding another one would not, at first glance, seem to be the ideal move. NYSE, Nasdaq and CBOE control 60% of trading and between them own all of the exchanges with the exception the IEX.

Before the demutualization of Nasdaq in 2000 and NYSE in 2005 these exchanges did not charge their clients for market data. It was only after 2008 when they became for-profit companies that they began to charge.

MEMX is far from the first time that this oligopoly has been challenged since the Regulation National Market System (Reg NMS) opened the exchanges up to competition in 2005. Quasi-exchanges known as ECNs had opened up in the late 1990s and early 2000s, operating under a lower regulatory threshold and automated by Nasdaq. They were swiftly bought up by the incumbents.

Earlier consortia exchanges have included Chi-X Global (founded by Instinet and owned by BAML, GETCO, Goldman Sachs, Morgan Stanley and Quantlab Group), which was sold to Better Alternative Trading System (BATS) Europe in 2011. BATS also acquired Direct Edge, the New Jersey-based operator of the EDGA and EDGX exchanges, in 2014. BATS itself (owned by Citigroup, Credit Suisse, Tradebot Systems, Deutsche Bank, GETCO, JPMorgan, Lime Brokerage, Lehman Brothers, Merrill Lynch and Morgan Stanley) was bought by CBOE for $3.2 billion in 2016.

“It may look like a rinse and repeat exercise when a consortium of banks, brokerages and high frequency trading firms band together to launch a new US exchange such as MEMX,” points out Mindlin. “But the market’s structure is different than it was the last two times.”

IEX was founded in 2012 by ex-RBC traders Brad Katsuyama, Ronan Ryan, John Schwall and Rob Park, and finally gained regulatory approval in July 2016. It was made famous by Michael Lewis’s book ‘Flash Boys’ published two years earlier. Until MEMX receives its licence it remains the only independent equity exchange in the market but with a less than 3% market share.

“MEMX does have a better chance than IEX, but it depends on their market model and technology,” says Tabb. “These guys have a tremendous advantage here because they control the order flow. Even if they only run 15% to 20% of flow through the new platform, that will give them market share.”

Cookie cutter

The fastest way to get exchange approval is for MEMX to have a cookie cutter, maker-taker structure. It has explicitly ruled out incorporating a speed bump like IEX did, which slows trading by 350 microseconds and delayed the latter’s licensing by two years. However, Gerald Lam, head of communications at IEX, tells Euromoney that this is a mistake. “It is a problem when you have fragmentation without differentiation,” he warns. NYSE, having lobbied furiously against IEX’s speed bump, introduced one of its own to its small and mid-cap exchange, NYSE America, in 2017.

Lam argues that new entrants need to innovate – just being cheaper isn’t enough. Certainly, one more exchange means that clients will have to pay one more set of fees, but Liquidnet’s Sussman seems rather more relaxed on this point. “Fragmentation is like having kids – after you have three of them, you just go numb to the pain,” he says.

MEMX will certainly need the best in class market data and infrastructure in order to persuade brokers to use it as a routing aggregator and market data supplier. Achieving this against such entrenched incumbents will be very hard. NYSE rolled out a new trading platform, Pillar, in 2016 and Nasdaq is working on a unified technology programme called the Financial Framework. CBOE got state of the art technology from its 2017 acquisition of BATS.

“MEMX membership, as the press release betrays, is too diverse – this diversity militates against anything specific or different, limiting the potential for innovation.” -Kurt Dew, Northeastern University

But this is where the members come in. MEMX includes two of the largest retail wholesalers (Citadel Securities and Virtu), four of the largest online brokers (Schwab, TD Ameritrade, E-Trade and Fidelity) and three of the largest retail warehouses (BAML, Morgan Stanley and UBS).

“These firms all route to one another,” claims one industry expert. “You can see how much these brokers route to Citadel Securities and Virtu. If, on day one, MEMX has a 5% market share then the regulators will be looking for sweetheart deals between the members,” he claims. Khandros at UBS brushes off any such suggestion. “Each firm has an independent best execution obligation in terms of deciding where and how to route,” he says.

And, as Mindlin points out, the market has changed. It is hardly surprising that the brokers route so much flow to Citadel Securities and Virtu – between them these two firms now account for 40% of the market. A small number of exchange members now account for the vast majority of order flow: there are now fewer banks in the market and most have exited primary market making. The high frequency trading sector has also matured and its profits normalized, resulting in a smaller number of firms. “Now we seem to have a market structure with a small, homogenous pool of similar-looking participants,” states Mindlin.

As a consequence, MEMX’s ownership covers such a large part of the industry that the incumbents need to sit up and take notice.

|

|

|

Richard Johnson, |

“The exchanges should be concerned,” warns Johnson. “MEMX can be successful. Citadel Securities and Virtu have very robust technology and no hurdles that they couldn’t overcome. They are well funded and have a lot of flow.”

This strength can also be a weakness, however. Consortia are hard to manage and it will be difficult for the exchange to claim to be always acting in its members’ best interests when they come from such a broad spectrum of the industry. Dew sees this as a limitation. “MEMX membership, as the press release betrays, is too diverse – this diversity militates against anything specific or different, limiting the potential for innovation,” he says.

Khandros at UBS acknowledges that MEMX is not the first time that a consortium has attempted to take on the incumbents, but he says that this has informed the offering.

“There are definitely elements of other consortia that were intended to enhance competition,” he says. “Many of us have been involved in other deals, which brought diverse constituents around the table. We have learned from these as to what worked well and what can be further improved.”

He dismisses any concern over the diversity of the members as they all face the same fee problem. “It was surprising to see how so many different firms aligned when faced with similar challenges.”

Many see MEMX as simply BATS 2.0. But there is an important difference: retail. “Within MEMX there are three big firms that sell retail order flow and two big purchasers of retail order flow,” points out one market expert.

“This could be seen as one giant strategic threat, with the Members Exchange saying to the exchanges that they will come after their transaction revenue if they don’t cut data charges.” -Richard Johnson, Greenwich Associates

The involvement of these firms is significant due to another area of exchange practice that the regulators are scrutinizing more closely, payment for order flow. The order protection rule of Reg NMS states that brokers are required to route orders to exchanges with the best prices: this is best execution SEC rule 611.

Nevertheless, under the maker-taker exchange model brokers receive compensation (rebates) for directing orders to a particular exchange as payment for order flow. This is hugely controversial, riven as it is with conflicts of interest (brokers claim that it keeps fees down for the end client). In 2016, the SEC raised questions about the practice but has not moved to ban it as yet. In December last year, however, it launched a transaction fee pilot that could spell the end for the practice.

Certainly, if this pilot results in a world where exchanges cannot rebate customers for posting liquidity, it will make much more sense for retail firms to own the exchange function than it does now. “If payment for order flow goes away, the retail brokers will want to have their own exchange,” says the expert. “That could be what is behind this. I have never before seen retail wanting their own exchange.”

Work ahead

In order to demonstrate the competitive threat that MEMX poses, it certainly needs to move quickly. “MEMX hopes to file its application for exchange registration with the SEC this quarter,” Khandros explains. “Getting the announcement out and getting funding secured were major undertakings, but the venture still has a tremendous amount of work ahead. Working with the SEC to successfully advance the application for exchange registration will be paramount. People are excited over this project and many have expressed their support and enthusiasm.”

It will take more than enthusiasm to make a significant dent in the incumbent’s dominant market share, however, as IEX has found. “Even if they get it live, it has more like a five-year trajectory to gain significant market share,” Tabb reckons. “Consortiums are not easy to pull off – it will be difficult to both start and exchange and manage a consortium.”

However, the members involved, the amount of order flow that they control and the recent increased regulatory scrutiny might mean that this time things could be different.

“This could be seen as one giant strategic threat, with the Members Exchange saying to the exchanges that they will come after their transaction revenue if they don’t cut data charges,” says Johnson. “However, I don’t think that it is just a threat.”