Illustration: Jeff Wack

|

IN ADDITION |

|

Where over-leverage meets the higher cost of money is the place that the true consequences of the last 10 years of quantitative easing will be felt.

“The market doesn’t have a vision of defaults,” says David Nazar, chief investment officer at distressed debt specialist Ironshield Capital. “It is turning a blind eye to previous default cycles and has become complacent.”

The last decade has seen some lending behaviour that would indeed suggest that default or even fraud simply did not loom large in credit underwriters’ decision-making.

Some banks have already been violently shaken out of that complacency. In their fourth-quarter earnings, a handful of the world’s biggest lenders announced losses on single-name exposures the like of which had not been seen in many years.

In mid January, Bank of America revealed a $292 million charge against its lending to one (yes, just one) client, forcing chief executive Brian Moynihan to observe that: “Once in a while, something doesn’t turn out the way we want because that’s what the definition of taking risk is.”

No one would dispute the observation that this was taking risk. The key question is whether it really is just a one off or a harbinger of more to come at a bank that prides itself on responsible credit underwriting and risk management.

Moynihan is, at least, in good company.

In the same week, JPMorgan recognized a $143 million mark-to-market loss on a margin loan to the same client – stricken South African retailer Steinhoff. Citi revealed a $130 million “episodic loss” related to the same firm, while Goldman Sachs announced that the impairment of a secured loan had hit its fourth-quarter net revenue. UBS has reported SFr79 million ($84.5 million) of credit losses “mainly related to a margin loan”.

In February, it was additionally revealed that HSBC had been hit by a 40% rise in quarterly loan impairments to $658 million. This substantial figure is understood to relate to exposure to both UK construction group Carillion and Steinhoff. HSBC declined to comment further.

These painful revelations stem from a €1.6 billion margin loan that was made to former Steinhoff chair Christo Wiese in September 2016. The loan was secured against 628 million Steinhoff shares that were worth €3.2 billion at the time. It was arranged by Citi, HSBC and Nomura, with Bank of America Merrill Lynch, BNP Paribas, Goldman and JPMorgan joining as lenders.

Former Steinhoff chairman Christo Wiese, top left, and the company’s executives

appear at a parliamentary hearing into the Steinhoff scandal

Allegations of accounting fraud at the firm were behind the tight-lipped admissions in the banks’ subsequent results announcements.

As borrowers have piled into cheap leverage over the last decade, a lot of banks appear to have left themselves potentially over-exposed to single-name risk.

While it is an age-old problem, the social media age has a new term for it: FOMO, or fear of missing out. Many banks, it seems, simply could not bring themselves to turn down financing opportunities, even as the number of acquisitions mounted up. Worse still, such was their desire for lucrative deals with high coupons that banks became increasingly lax about covenants, sometimes to the extent of excluding them altogether.

At the very sharp end of the easy-money era was the growth in margin lending. Often through their private banking arms, banks increasingly turned to extending margin loans – usually secured on stock – to senior executives and part-owners of businesses.

The banks, surely, had been warned. It all seems very Icelandic entrepreneur, circa 2005. But they told investors it was a clever way to increase revenue at low risk by making collateralized loans to very wealthy individuals well known to the banks that had clear sight of their investments and debt service capacity because the banks already managed this wealth for them.

The spectacular implosion of Wiese’s margin loan is a grim reminder of how quickly allegations of fraud can destroy market value. It has also served as a reminder of just how large this business has become. Recent data from the Bank for International Settlements shows that the absolute value of margin debt held by US investors has risen from $8 billion in November 2011 to $256 billion in July 2017.

The previous peak was $79 billion in June 2007.

Margin debt has not been at these levels since the dotcom boom in 2000, when it reached $214 billion.

Should QE taper and end, we should have seen the low in rates. This can’t help but to feed through to credit in general and the low end of the credit spectrum in particular – David Nazar, Ironshield Capital

Steinhoff is not the first time some of these banks have been hit by their margin lending. In March 2001, Bank of America lent WorldCom chief executive Bernie Ebbers around $400 million, much of it backed by WorldCom stock, which collapsed when an $11 billion accounting fraud was uncovered at the company.

There is no doubt that the combination of historically low interest rates and surging stock markets has driven the recent dramatic rise in this business.

In many ways, margin lending is the ultimate by-product of the extraordinary lending conditions that 10 years of quantitative easing have created. However, the argument that the banks had little choice but to lend such a large amount to Wiese, because of the need to protect their cash management, export finance and clearing business with his firm, does not really explain the size of their exposure. Would Wiese really have pulled maybe 700 accounts in 40 jurisdictions if they had said no?

The explosion in margin lending shows what happens when there is too much cheap money needing to be put to work. And Steinhoff’s predicament shows exactly how painful it can get when things go wrong.

With interest rates set to rise, the perennial turning-of-the-cycle question is relevant yet again: when the tide goes out, who will be swimming naked?

Turning the metaphor to ships, some companies will be holed beneath the waterline by the excess of debt they took on and some will already be restructuring in order to avoid hitting the rocks.

Then there will be the companies that become synonymous with the end of an era. These will be companies that acquired and built leverage at extraordinary levels and which, when they became subject to the scrutiny of crisis, were soon proven to be fraudulent. They will be the Enron or WorldCom of tomorrow.

For now, that company is Steinhoff.

Forensic vigilance

Margin lending is defined as the provision of financing backed by a portfolio of cash, shares, units in managed funds, commodities, derivatives and any other form of market-traded asset that is extended to individual or corporate borrowers for the purposes of financing investments. The value of that portfolio of market-traded assets is therefore key to the process and, in an era of rampant QE-driven equity overvaluation, such lending should be approached with forensic vigilance.

By any measure, lending €1.6 billion to enable the South African retailer, which had made nine acquisitions in two years, to acquire Mattress Firm, which had itself made 18 acquisitions since 2007, is a sign of a frothy market.

Now, as the first signs of what rising rates might actually herald become apparent, the company’s implosion might be a timely reminder of just how frothy conditions have become.

Steinhoff is far from the only aggressive borrower under the spotlight. Another over-leveraged corporate that has seen its share price collapse in recent months is cable group Altice. Banks may again be exposed to risky margin lending – Altice’s share price halved in the three months to January.

Goldman Sachs is understood to have written Altice founder Patrick Drahi margin loans before the group’s IPO in 2014 and to have subsequently provided him with a funded collar facility in order for him to repay them.

An equity collar involves the simultaneous purchase of a put option with a strike price below that of the equity and the writing of a call option with a strike price above that of the equity. Both options are out-of-the-money and usually have the same expiration date.

The facility written for Drahi is understood to be still outstanding. Indeed, €2.3 billion of Altice’s €51 billion of debt outstanding is believed to remain on the balance sheets of its relationship banks, of which Goldman is a prominent member.

French fund manager Carmignac Gestion, which held a 3% stake in the firm last September and was then Altice’s major shareholder, has recently sold out of the firm, citing operating performance and concerns over its level of debt. Altice’s capital structure is now so complex that bondholder risk varies greatly. But as with any exposure, the closer you are to the assets as an investor, the safer you will be. Margin lenders will be crossing their fingers.

The availability of cheap money can be highly addictive. Michel Combes, who abruptly parted company with Altice in November last year following its poor results, took over as CFO at US mobile phone company Sprint in January this year. Almost the first thing he did was announce a high-yield bond issue – the firm’s first such deal since 2015 – sending Sprint’s outstanding bonds into a tailspin.

Sprint has roughly $30 billion debt outstanding and a debt-to-equity ratio of 196.43%, but this was not enough to put off yield-starved investors in today’s market: the deal was actually increased from $1 billion to $1.5 billion. Sprint will use Altice’s cable infrastructure to transmit cellular data and develop a 5G network in the US.

Jumbo funds that were raised to invest in distressed debt aren’t seeing the deals, so many are focusing on the hairier end of the PE spectrum instead – Johnny Colville, Houlihan Lokey

Warning signs are also flashing at Chinese conglomerate HNA, which saw group borrowing surge by more than a third in just the first 11 months of 2017 to Rmb637.5 billion ($99.14 billion) after a $40 billion acquisition spree. HNA has used margin loans and funded equity collars to, among other things, build a 10% stake in Deutsche Bank. In February, it revealed that it is now reducing that stake as its liquidity problems worsen.

UBS, with ICBC, provided the margin loans for this strategy, which have reportedly been repaid.

UBS has the largest margin lending operation of the big banks, with $55 billion of margin loans outstanding at UBS International in 2017 and $36 billion at UBS Americas. Credit Suisse has a $42 billion margin lending business and BAML a $40 billion one. In January this year the total value of outstanding margin loans topped $600 billion, prompting US regulator Finra to publish an investor report highlighting the risks inherent in such lending.

HNA offers a good example of how the type of over-leverage that has now become possible thanks to lower-for-longer interest rates can bleed across complex organizations and into many other parts of the market.

The Chinese conglomerate, already facing a liquidity squeeze, borrowed €400 million from its own subsidiary Swissport last August as a 90-day loan. In November, however, Swissport announced that it was to roll over the facility when it fell due – which is technically a breach of its bond covenants.

The news hit both Swissport’s €265 million 9.75% secured bond and its $364 million 6.75% secured bond, which had been trading at around 110 before the news broke and subsequently fell to below par. HNA is now considering an IPO of Swissport, advised by Rothschild.

“The cheap availability of leverage has given groups time to lever up,” points out Jeremy Ghose, managing director and head of Investcorp Credit Management in London. The firm has $11 billion under management primarily invested in senior secured corporate debt issued by mid- and large-cap corporates in western Europe and the US. “There are no bites to the covenants, if indeed the borrower has a covenant; so when failures come, the impact will be much greater as there is no discussion with the borrower.”

Ghose concedes that the one counter to this is that equity percentages in sponsor deals are higher than they were in 2007.

“We are in unchartered territory because we haven’t had a real credit cycle since 2008/09 – 10 years. There are a whole bunch of people in the marketplace that haven’t seen a true default cycle because of QE,” he says.

Market volatility in early February served as a sharp reminder that the withdrawal of QE and consequent rises in rates may not go as smoothly as hoped.

“The largest risk to performance in 2018 is an unexpected rise in rates volatility,” Jens Vanbrabant, head of sub-investment grade investment at asset manager ECM in London, told Euromoney shortly before the disruption began. However, he saw the chance of this as remote. “Central banks have been very good at taking control of the rates narrative, and are unwilling to risk what little GDP growth they have managed to create.”

While much of the focus in February was on inflation, rising rates are the great challenge that the market has to deal with.

“In January, we saw long term inflation expectations rise more than 13 basis points per year, but in February this fell to around 9bp,” says Payson Swaffield, chief income investment officer at Eaton Vance in Boston. “So, of the 47bp increase in the 10-year treasury yield since the end of 2017, only 9bp is due to greater inflation expectations. The 38bp balance is due to synchronized growth and the cost of money getting higher.”

Things will not be helped by the prospect of increased US borrowing to fund Trump’s tax cuts at the very moment that the key Chinese buyer of treasuries is stepping back.

|

|

David Nazar, Ironshield Capital |

“Should QE taper and end, we should have seen the low in rates,” says Nazar at Ironshield Capital. “This can’t help but to feed through to credit in general and the low end of the credit spectrum, where we focus, in particular. It will make the cost of credit higher, and credits at the low end of the spectrum are most vulnerable to increased finance costs. In recent history, we have seen small changes in the underlying benchmark yield cause effects in the market – particularly at the lower end.”

Nazar was principal of European special situations at Bank of America before quitting the bank in 2007 to set up Ironshield.

Refinancing dominance

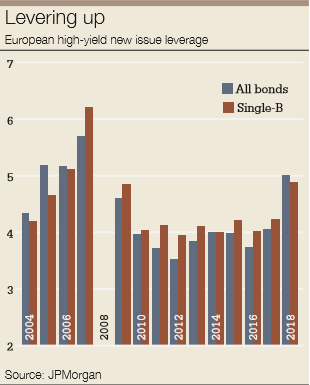

One of the most remarkable features of the sub-investment grade market over the last year has been the dominance of refinancing in deal volumes. According to Lipper research, $933 billion of leveraged finance activity in 2017 was down to refinancing, which surpassed the previous record set in 2013 by 23%. The new money share of the market dropped to just one third of volume from 47% in 2016.

The story was the same in Europe – a market driven not by new economic activity but by firms simply being able to replace already historically cheap credit with even cheaper money. Endless refinancing eventually became the search for the greater fool.

“The record-setting volume of repricings and refinancing was a bit of a surprise last year, given the amount of refinancing/repricings that took place in 2015 and 2016,” admits Chris Munro, co-head of global leveraged finance at BAML in London. “We thought the pace would trickle off at some point, but it continues to be the largest segment of the market. We expect this trend will continue into 2018, but at some point the economics of a refinancing won’t be as compelling as they are right now. We are however optimistic that, given the robust environment for M&A, event-driven financing could replace some or all of any slowdown in refinancing activity.”

That hope is echoed by Ray Doody, global head of leveraged and acquisition finance at HSBC.

“Rates have probably troughed, so there are probably going to be fewer refinancing trades in 2018 than we saw last year,” he tells Euromoney.

“There will be more dependence on M&A for deals in future,” he reckons. “This year is the first year where people have been saying at the beginning of the year that the economy is looking better than it has in the last 10 years. So we are likely to see more M&A as a result. Corporate-to-corporate deals that give rise to big levered flows are what investors really want to see.”

Doody joined HSBC last year from JPMorgan, where he had led the European leveraged finance business since 2008.

The US investment-grade market could see exactly that in spades with the news that Singapore-based Broadcom’s proposed acquisition of chip maker Qualcomm would entail the largest-ever bridge financing of $100 billion. Twelve banks are lined up to provide the funding, led by BAML and JPMorgan. Other lenders include Citi, Deutsche Bank, Mizuho Financial, Mitsubishi UFJ, Sumitomo Mitsui, Wells Fargo, Bank of Nova Scotia, Bank of Montreal, Royal Bank of Canada and Morgan Stanley.

The largest bridge loan prior to this was that for the Anheuser-Busch InBev deal in 2015. The Qualcomm deal also involves the largest-ever break-up fee: $8 billion.

Any deal could be some way off, but it will inevitably see Qualcomm’s single-A rating cut by multiple notches; in early February, the firm’s bonds had already fallen in value by 6% since news of the bid was announced in November.

Heading into sub-investment grade is no longer the hurdle that it once was for many firms, due – unsurprisingly – to the low cost and flexibility of funding now available at lower credit ratings. Cheap money has fundamentally changed corporate behaviour.

|

| Chris Munro, BAML |

“There can be great opportunities among fallen angels, you just have to do the work to understand why they have fallen,” says Munro at BAML. “Some may have fallen for fundamental credit or structural issues, but for others it could be a short-term phenomenon and there could be a very clear and achievable path back to investment grade.

“Some companies, for example, have actively chosen to go into the sub-investment grade territory because the cost of financing and the funding flexibility that is achievable are currently very attractive and can enable them to achieve their strategic objectives.”

Roughly $70 billion of debt is poised to move into high yield from investment grade in 2018, according to Morgan Stanley. This is double the volume predicted to move the other way from high yield to investment grade. Why? Because many investment-grade firms are now so aggressively levered that any M&A activity that adds to debt will inevitably lead to them becoming fallen angels.

Corporates have had access to very cheap money for a long time and often have simply used it to buy back stock or fund dividend recaps. Many believe that despite the prospect of rate rises, even weaker sub-investment grade credit may not be as exposed as it seems.

“The market is not at unsustainable levels of indebtedness,” says ECM’s Vanbrabant. “In 2006/07 there was an extra turn of leverage – a lot of which was second lien and subordinated. This meant that senior leverage was closer to six or seven times.

“The second lien and mezz market is not there now, so leverage is all senior,” he explains. “You have to ask to what extent are you dependent on equity support and to what extent on cash flows?”

Many participants argue that, while the impact of rising rates will be understandably felt in investment grade, high yield will be relatively immune as long as the economy is robust.

“The market is very healthy and borrowers can refinance easily,” says Vanbrabant. “The number of stressed and distressed companies is very low; the proportion of loans trading below 80 is at the lowest levels since 2008. During the recent rates induced volatility [prior to February], credit spreads were well behaved. High yield moved a bit and loans didn’t move at all. The credit market is still reflecting that it is a source of yield.”

QE withdrawal

The rampant liquidity available is not likely to change quickly and the overriding technical that has been driving the markets to this point is still in place. But at some point, QE withdrawal of big enough magnitude will have to be dealt with. The more recent volatility saw the US high-yield index widen 28 basis points between January 31 and February 9, while euro and sterling high yield both widened by 20bp to reach 234 and 338 respectively.

|

|

“In high yield, rate risk is greater than credit risk,” Swaffield confirms. “The 1.3% fall in the high yield index between the end of December and Friday February 9 was mostly the result of embedded duration. Credit spreads haven’t widened.”

Volatility now seems inevitable across the corporate bond market, however.

“Investors will focus this year in terms of where they buy,” explains Simon Francis, co-head of EMEA leveraged finance at Citi in London. “Higher coupon deals in the bond market will be less sensitive to interest rate movements. Overall, we expect more volatility in the bond market compared to the loan market. But even if markets were to move 50bp to 100bp, I don’t think that it stops strategic M&A dialogue. I would be more cautious if the market takes time to find a new level.”

So much money is now cheaply available, however, that discipline is inevitably breaking down.

“Typically the early part of the year is heavily weighted towards double-B large-cap repeat issuers, as part of their ongoing financing needs,” observed JPMorgan credit strategist Daniel Lamy of the European market in early February. “Year to date double-Bs constitute only 40% of issuance, the lowest first-quarter share since 2007.”

He adds that, in addition to the weaker ratings mix, so far issuance this year has been more highly levered and a greater share classed as “credit negative” from a use-of-proceeds perspective.

That is surely not a healthy sign.

Triple-C issuance is still only around 2% of the European high-yield index, compared with 6% to 7% in the US, but pricing on low single-B and triple-C credits came in an astonishing 250bp during 2017. Being paid plus or minus 6% return for triple-C risk is not an adequate return for risk in anyone’s book.

The question is whether and where the extraordinary amounts of debt that companies have accumulated during 10 years of pretty much zero rates will manifest itself. Steinhoff’s spectacular collapse was triggered by long-circulating rumours of fraud, but it is also in the crosshairs of one of the weakest parts of the corporate universe – heavily indebted retailers.

|

|

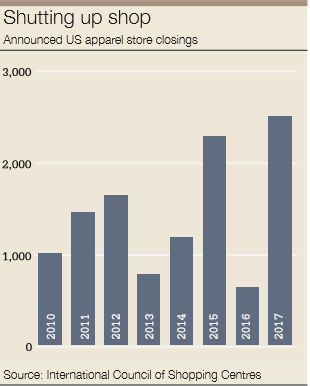

“We had the most store closures in US history last year,” points out David Berliner at corporate finance advisory firm BDO Global. “There are too many stores per capita and those stores are too big. Retailers in distress, such as Sears, JC Penney and Neiman Marcus, have taken on a lot of debt. 1,300 shopping malls across the country are anchored by department stores and other large retailers.”

Recent data from Moody’s reveals that one-year default expectations in the retail segment have hit 4.5% in the US and 1.75% in Europe. This is the third most-risky sector behind advertising, printing and publishing (5.75% in the US and 1.8% in Europe) and US durable consumer goods (5.1%).

“Retail is one of the sectors that has had its difficulties,” says Munro at BAML. “There are some macro trends, such as the rise of Amazon and online shopping that have impacted a large portion of the sector, but it’s unfair to lump all retailers together. Investors will look at every credit on an individual basis, and those that can demonstrate robust growth, margins and free cash flow will continue to have access to the market.”

Here, the ever-present concerns over covenant protection will come into play.

“Deal structure does concern us,” says Ghose at Investcorp. “The lack of legal bite in the documentation is clearly of concern. When something goes wrong, there is nothing to trigger a discussion with the borrower. The language of trading and transferring that is being put in place by borrowers also makes it quite difficult to trade out of names as sponsors control who can own the loan.”

With the vast majority of leveraged loans now covenant-lite, the market could very quickly see the impact of this on corporate behaviour. Firms that have lenders breathing down their necks are forced to take action. Where there are no early warning signs, the obvious worry is that by the time problems become apparent it is already too late.

“Sears, whose loan agreements were entered before the current wave of covenant-lite loans, has had seven years of losses but has survived by selling off pieces of itself,” explains Berliner. “Things will be a lot worse without covenants to trip as lenders can’t put the brakes on. When there are no covenants to trip it is a concern for lenders.”

Another retailer that has struggled for a long time is UK apparel chain New Look. The firm, which lost £10.4 million in the six months to September last year, has a £1.2 billion debt pile, which translates to an eye-watering gross leverage of 13.9 times.

It is, coincidentally, owned by South African investment firm Brait Investments, of which Steinhoff’s Christo Wiese is a non-executive director.

Brait bought New Look for £1.9 billion in 2015, funding the purchase from the proceeds of a stake in African retailer Pepkor Holdings. What is additionally shocking is that New Look has been operating at this level of indebtedness for years. When Brait bought the firm from Permira and Apax, it did not lever it up. In December, however, New Look was downgraded to Caa2 from Caa1 by Moody’s.

The firm has £700 million 6.5% notes due 2022 outstanding, along with £364 million 4.5% bonds also due in 2022. The former were trading at 35 pence in the pound in January, down from 90p a year ago. Lenders, including Carlyle, Blackstone’s credit division GSO, asset managers CQS and M&G Investments, investment firm Alcentra and distressed debt investor Avenue Capital Group are understood to have formed a group to negotiate on a restructuring.

“A jolt to the market could come from a well-known name in the retail sector facing difficulties,” predicts Ghose.

“This could lead to a default which could impact the market. There are a large number of credit funds in, for example, New Look. A company like this defaulting would have a big impact,” he says, warning: “There are handful of names where if they do hit a wall people are stuck – they can’t get out.”

Distressed debt

When and if that happens, a decade of QE has changed the fundamentals of distressed debt investing too. Specialists have simply been crowded out by other investors desperate for any kind of yield. The implications in a downturn are obvious.

|

|

|

Johnny Colville, |

“Jumbo funds that were raised to invest in distressed debt aren’t seeing the deals, so many are focusing on the hairier end of the PE spectrum instead,” says Johnny Colville, managing director in the financial sponsors group at Houlihan Lokey, who joined the investment bank in September 2016 from HSBC. “If your plan was to buy a distressed high-street name at 80 and sell at 90, you aren’t going to be able to do so, as all the big credit funds will be all over it.”

He is sanguine, however, about the risk that these funds face if performance deteriorates: “A credit fund that is sitting on cash needs to get invested. Debt-to-equity ratios haven’t compressed, with sizeable equity cheques being written. An equity cushion of 50% means a business has to self-evidently halve in value before a credit investor runs into trouble. If the borrower can service its interest and there is cash in the till, then you are not going to lose money.”

In some parts of the retail sector, however, there is a very real risk that businesses can and will halve in value, which is why these credits are approached so warily by many.

“Sears was number one in the US a few years ago but is now in a death spiral that it is almost impossible to pull out of,” muses Berliner. “We are seeing a shakeout in the sector between good and bad retailers. We will start to see retailers fix the bricks-and-mortar problem. Stores need personalization, they need AI or computer displays with knowledgeable staff and easy returns. The internet has taken away the easy stuff and we will see the better retailers figure out what people want and adapt.”

The extent to which firms are willing and able to adapt will dictate future distress in the sector. The smarter players are already taking action.

“Traditional bricks-and-mortar retailers are turning into data experts,” says Colville at Houlihan Lokey. “There is massive value in data and analytics, so businesses are increasingly looking to optimize this, rather than selling yet more ‘stuff’ that nobody needs. But that requires a different kind of banker, with a different skill-set.” Coincidentally, Houlihan Lokey recently announced the acquisition of Quayle Munro, which has 30 bankers focused on data and analytics.

Retail risks have attracted a lot of attention because of the fundamental changes that the sector is undergoing. But leverage has risen across sectors and geographies.

The market has long taken comfort in the fact that the risks to the system are nowhere near what they were in 2007 due to the neutering of the most egregious innovations in structured finance and securitization. But cheap debt is everywhere, and many of those innovations are starting to creep back.

Corporates have taken on debt on extraordinarily cheap terms – and this may well come back to haunt them.

“This will all come down to rates, which will take some time to percolate through,” says Nazar. “But it will become more apparent over the course of this year.”

It may take a few more spectacular blow ups before investors and issuers really start to sit up and take notice. Equity markets are sending unambiguous signals, but in credit the reaction is diluted by all the QE-driven money still looking for a home.

“The stock market is looking forward, but the high-yield market has not done so year to date,” says Swaffield. “If it were, we would see greater volatility in high yield. The Fed funds futures market is still disconnected from the Fed’s dot plot forecast – the market is still expecting fewer rate rises than the Fed is indicating.”

While corporates have tapped high-yield bonds for funding, sponsors have been taking advantage of extraordinarily loose lending terms in the leveraged loan market. And even with private equity’s dry powder now having hit the $1.7 trillion mark, there are no signs of any retrenchment in that part of the market either.

“Funds tell LPs [limited partnerships] it isn’t about IRR [internal rates of return] now, it is all about the money multiple,” says Colville. “They are all playing portfolio theory – as long as there is one rock star investment in the fund, given the ongoing desire from LPs to deploy capital in search of yield, the next fund-raising will be fine.”

The pressure to put money to work in private equity will, therefore, keep the leverage juggernaut rolling for quite some time in this part of the market. Indeed, 2017 saw 152 public to private deals – a total that is nudging the all-time high of 196 deals that took place in 2007. That’s not a desperately healthy precedent.

At the end of February, Toys R Us, owned by private equity firms Bain Capital and KKR, collapsed under the weight of $5 billion of loans they had burdened it with.

It is not only the retail sector where the implications of this easy money are there for all to see. The UK mid-market restaurant sector is now showing clear signs of the overcapacity that years of overexpansion – often funded by private equity money – has created.

“High fixed-cost businesses will suffer because of potential wage inflation and rates going up,” says Ghose. “This includes both retail and restaurant chains. We are seeing issues in these industries because the model is fundamentally changing.”

For many investors, navigating the corporate bond and loan market may involve playing much more defence than offence as the debt chickens of a decade of loose money come home to roost. The yield-chasing of the last 10 years may now finally need to make way for more vigilance.

“You make money by avoiding the losers,” states Vanbrabant. “We did not buy Steinhoff as we had a view that there were a few red flags. Our job as credit fund managers is to navigate that maze.”

Steinhoff’s troubles

The problems at Steinhoff came to a head towards the end of 2017 when accounting irregularities prompted the resignation of chief executive Markus Jooste and a delay in publication of the firm’s financial results on December 5.

Trouble had been brewing, however, since the summer, when a German business news magazine raised questions over inflated revenue figures at some subsidiaries that are now being investigated by German prosecutors. On December 6, Steinhoff’s board confirmed that this could impact the valuation and recoverability of up to €6 billion-worth of non-South African assets.

The impact on Steinhoff’s share price was swift and savage. According to Markit, 40% of Steinhoff shares that were available to borrow were out on loan before the December 6 announcement – showing how many people were already shorting the stock.

The share price fell 62% in a day once the news broke; by January 30, the Steinhoff International Holdings NV share price was down 85% from November 2017, wiping €12.4 billion from its market capitalization.

Steinhoff has at least 200 subsidiaries and affiliates worldwide, including Conforama in France, Poundland in the UK and Mattress Firm in the US. Indeed, its recent debt-fuelled acquisition spree, which has seen nine companies acquired in just two years, is at the heart of its problems.

“The valuations placed on the group’s serial M&A purchases looked wrong and, indeed, now look even more wrong as disruption in global retail has accelerated,” said analysts at CreditSights in December. The addition of Poundland and Mattress Firm in 2016 added $5.5 billion in debt to Steinhoff’s already stretched balance sheet.

These acquisitions also necessitated the fateful margin loan that has so spectacularly tripped up some of the world’s leading lenders.

Christo Wiese, then Steinhoff’s chair, pledged 628 million shares as collateral for the loan in September 2016 to enable him to buy shares in the IPO to fund the deals. Wiese underwrote €1.9 billion of the €2.45 billion IPO and the rest was taken by black empowerment vehicle Lancaster 101. Wiese financed this through a margin loan and collar via borrowing vehicle Upington Investment Holdings.

The 628 million shares were double the amount that Wiese had committed to buying in the capital raise itself. The shares, which were then worth €3.2 billion, were pledged against a €1.6 billion loan from Citi, HSBC and Nomura. Other banks that took exposure to the loan included BAML, BNP Paribas, Goldman Sachs and JPMorgan.

When the stock collapsed, the banks were understood to still be exposed to €1.1 billion of the loan, which if the revelations in the recent quarterly results are anything to go by, looks like it might be close to the mark.

Rout

In September 2016, when the loan was agreed, the stock was worth €5.055 a share, but in December it was valued at just €0.49 following the rout – with the 628 million shares pledged as security worth just 9.8% of their original price.

The lending banks swiftly enforced the sale of 98.4 million shares – less than 16% of the original amount – late on Thursday December 7 but have been left nursing the painful losses that they were forced to reveal in their quarterly results.

Steinhoff has three convertible bond issues outstanding: €465 million 4% notes due 2021; €1.1 billion 1.25% notes due 2022; and €1.1 billion 1.25% notes due 2023. There is also a 1.875% senior note due 2025.

Its bond yields blew out to more than 14% when news of the scandal broke. The fact that the ECB had bought some of the 2025 bond attracted unwanted attention after the problems at the issuer came to light; the central bank quietly disposed of its entire position in early January, at a rumoured loss of €50 million.

An Austrian subsidiary of Steinhoff issued roughly €650 million of Schuldscheine in July 2015 through BayernLB, BNP Paribas, DZ Bank, Erste Bank, Société Générale and Raiffeisen Bank International.

According to Bloomberg, these notes were trading in the low 70s in January (but up from 65% at the beginning of the month).

Steinhoff met bankers in London on December 19, having previously announced that despite meeting with its lenders, “significant near-term liquidity is still required”. However, at the January 26 bank meeting it confirmed that “immediate operational liquidity requirements have been largely addressed”.

This had been achieved by rolling over €690 million in notional facilities and – in some cases – fire sale disposals. The firm sold about 29.4 million shares in South African financial services firm PSG to raise R7.1 billion ($590 million) and disposed of the company’s Gulfstream 550 jet (worth $25 million when the firm bought it in 2016).

Steinhoff has also sold the Vienna headquarters of Leiner Immobilien for €60 million, while Conforama sold 17% of online retailer Showroomprive for €79 million, which CreditSights states is half of what it bought it for last year.

Despite the terrible press swirling around Steinhoff, several group companies have been able to secure additional funding since the accounting irregularities came to light in December.

Mattress Firm secured a $225 million new credit facility from existing lenders in December 2017. Pepkor Europe, the parent of UK discounter retailer Poundland, secured a £180 million loan from US hedge fund Davidson Kempner in January 2018, while Conforama arranged €115 million three-year funding from a French asset manager in the same month.

PwC is now carrying out an independent investigation into what went wrong at Steinhoff. The firm has hired Moelis to oversee negotiations with lenders and Alix Partners to advise on liquidity management and operational measures.

On Friday February, 2 Steinhoff said it would suspend dividend payments until the end of June.