When we look back in 20 years’ time, I think it will be considered a watershed moment,” says Ed Kamonjoh, executive director at 50/50 Climate Project.

He is referring to the US 2017 proxy voting season, when the world’s two largest asset managers, BlackRock and Vanguard, voted for the very first time to back shareholder proposals on climate-related issues.

Their huge voting power pushed through resolutions at Exxon Mobil and Occidental Petroleum, underlining an historic year of more than 65 proposals from shareholders explicitly addressing climate-risk.

“BlackRock and Vanguard may have arrived late to the party, but they did arrive,” says Kamonjoh.

It is a different story when you ask BlackRock and Vanguard, both of which maintain it has just been business as usual. But pushed further, they admit that yes, they have started doing things differently. They have expanded their investment stewardship teams and plan to grow further.

They are communicating more with asset owners and companies about their engagement process around not just the ‘G’ but also the ‘ES’ in environmental, social and governance criteria. And they are escalating unfruitful engagements with companies to voting.

It is not just BlackRock and Vanguard. The influence that the world’s largest asset managers can have in pushing companies towards cleaner energy or board diversity has been recognized by pension funds, foundations, non-profits and retail investors. If you cannot convince a company to change, convince the largest asset managers to make them change through their voting power or (in the case of actively managed funds) divest.

|

|

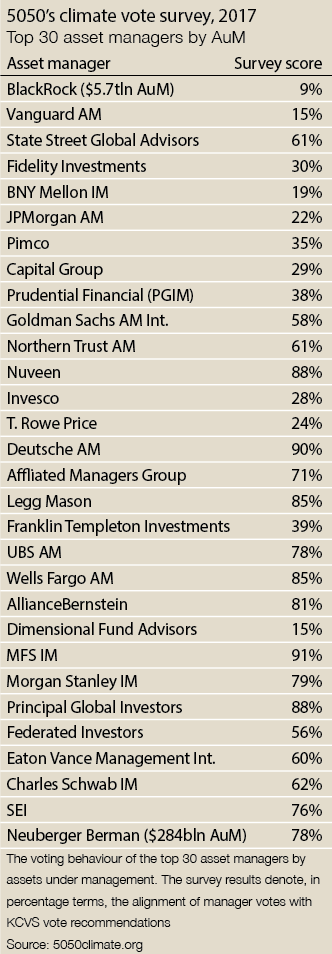

Some asset managers have been more open to listening than others. According to 50/50 Climate Project’s analysis of voting behaviour of the largest 30 asset managers by assets under management, in key climate votes at US oil and gas and utility firms over the 2017 proxy period, BlackRock voted with only 9% of the recommendations and Vanguard 15%. JPMorgan is also a laggard, voting with just 22%. State Street, the third-largest asset manager globally voted with 61%. At the higher end, UBS Asset Management and Morgan Stanley Investment Management were just shy of 80%, while Deutsche Asset Management voted with 90% of recommendations.

Despite BlackRock and Vanguard commanding a combined $10 trillion of assets under management and having the worst track record for key climate votes among the largest investment managers, there is a sense that things are reaching a tipping point. That they voted at all is, as Kamonjoh says, a momentous shift from nothing to something. Will that momentum continue?

Reticence to oppose

It has been a frustration for many asset owners in Europe and the US that their fiduciaries have not been using their voting power to enforce change.

Seattle City Employees’ Retirement System, for example, placed BlackRock, which manages a $339 million passive international equity portfolio for the pension fund, on watch in December last year because of concerns over the asset manager’s “reticence to oppose management, limited focus on environmental and social issues, inconsistency between their proxy voting record with their policies and public pronouncements and limited transparency on investment stewardship activities.”

This reticence has led shareholders of asset managers to file resolutions. Walden Asset Management, for example, filed proposals last year at BlackRock, Vanguard, BNY Mellon, T Rowe Price and JPMorgan reminding them that they were members of the UN-supported Principles for Responsible Investment (PRI) and asking them to carry out a review of their proxy voting, taking into account fiduciary duty to pay attention to climate resolutions.

In the end, all proposals were withdrawn other than at BNY Mellon and T Rowe Price.

Tim Smith, director of ESG shareowner engagement at Walden, says: “We ended up having very constructive discussions with the asset managers and learned about the steps they were taking to address board diversity, governance and climate risk with companies.”

Just why asset managers have been reticent about voting on environmental and social topics to the point where their relationships with asset owners have become strained raises questions.

“Conflicts of interest” is the answer many asset owners and commentators provide.

“While you won’t find an asset manager that admits it, of course they are conflicted,” says Andrew Behar, chief executive of As You Sow, which promotes environmental and social corporate responsibility. “The mutual fund companies are record keepers and advisers for the retirement plans of the companies held in their funds. How can you vote against a CEO pay package, or against management’s wishes broadly, when they are your customer and you could easily be replaced?”

Kamonjoh adds that the “symbiotic relationship” between asset managers and companies is “an open secret”. He points to comments by John Bogle, founder and former leader of Vanguard, who warned in 2002, as the SEC was considering requiring mutual funds and other registered management investment advisers to disclose their proxy votes, that: “Votes against management may jeopardize the retention of clients of 401(k) and pension accounts.”

“While you won’t find an asset manager that admits it, of course they are conflicted” – Andrew Behar, CEO of As You Sow

There is evidence to suggest that Bogle’s point about conflicts was right. A report in April by 50/50 Climate Project analyzing the 2016 proxy voting season showed that Fidelity, BlackRock, and Vanguard managed over $13 billion in assets for the pension and welfare plans of the largest oil and gas and utility companies, earning them over $18 million in fees the year before.

Did that sway their votes? As food for thought, the report points out that Vanguard was paid $3.8 million in fees by Chevron in 2015, and managed at least $863 million for the oil giant. Vanguard was also Chevron’s largest shareholder during the 2016 proxy season, controlling 6.2% of shares outstanding. Yet while 46% of Chevron shares were voted against the company’s compensation plan, Vanguard voted to approve it, ensuring it received majority support. Vanguard also voted against a resolution calling on Chevron to disclose the portfolio impact of scenarios in which global warming is restricted to a two-degree Celsius increase.

Meanwhile, BlackRock managed nearly $3 billion for BP’s retirement plans in 2015, receiving over $2 million in fees. BP posted a $6.5 billion net loss for 2015, including a $10 billion charge for its liabilities from the Deepwater Horizon disaster, yet BP’s proposed executive compensation plan for 2016 would have awarded its chief executive a 20% pay increase. While a majority of BP’s shares were voted against this plan, BlackRock voted in favour of it.

It is not just BlackRock and Vanguard. Wells Fargo, which had and still has a very strong track record of voting to back climate-change proposals in support of two-degree scenario planning, bizarrely voted against the proposal at Chevron in 2016. Was it a coincidence that Wells Fargo then chief executive, John Stumpf, sat on the board of Chevron over the 2016 proxy period? Wells Fargo funds also voted in favour of approving Chevron’s ‘Say on pay’ programme when Stumpf sat on Chevron’s compensation committee, even as 46% of shares voted at Chevron’s 2016 AGM opposed it.

While it is obvious that asset managers have conflicts, it is of course hard to say for certain that voting decisions like these are driven by those conflicts.

Michelle Edkins, global head of investment stewardship at BlackRock, says that when it comes to discussions about conflicts of interest, it is often forgotten that BlackRock has just as many clients that are labour unions, public sector and left-of-spectrum pension funds as it does large corporations.

“Generally, we are unaware of the relationships BlackRock may have with corporates in terms of managing their pension funds, and the people we are engaging with at companies are unaware as well,” she adds.

While the asset managers that seem to vote least on climate issues can insist their voting was not motivated by their relationship with the company, there seems to be a power structure between asset owner, asset manager and company whereby the latter seems to be at the top of the pyramid. For example, BlackRock, JPMorgan and Vanguard (Fidelity did not participate in interviews) all say they regard voting as a last resort.

|

| Nicolas Huber, Deutsche Asset Management: “Our voting policy is very clear and precise and strives to reduce room for interpretation” |

Contrast this with the view of Deutsche Asset Management (DeAM). Nicolas Huber is head of corporate governance at the firm. He says the bank made a shift away from guidelines to rules around engagement and voting in ESG issues in 2011, when it also started voting outside Germany.

DeAM will vote in favour of proposals that will enhance a company’s approach to climate change risk, CO2 emissions or greater transparency on ESG matters.

Through its votes, it also supports diversified boards – not only geared to gender but also age and cultural and professional background. Voting is far from a last resort, says Huber. Rather, any deviation from its voting rules has to be agreed by an internal escalation board.

“We take good corporate governance very seriously,” he says. “Whether it’s an index or active investment, we have the same rules. That has given us the advantage of having a very clear position on what is important to us. Our voting policy is very clear and precise and strives to reduce room for interpretation.”

Huber says it is clear for DeAM that it is acting on behalf of the owners of the company.

Voting inconsistency

This kind of black-and-white approach is something asset owners say they wish was implemented more broadly, particularly in light of perceived inconsistencies in voting. For example, while BlackRock, Vanguard and JPMorgan voted for proposals at Exxon, Occidental and utility PPL to report portfolio impact for limiting global warming to two degrees, they did not do so at Kinder Morgan, Devon Energy or Duke Energy. Similarly, Fidelity voted for the proposal at Exxon and Duke but not at Occidental.

“That’s hard to understand and makes one question whether the votes were purely done because Exxon is so high profile?” says Andrew Logan, who heads up oil and gas research at sustainability non-profit, Ceres.

Jamie Kramer, head of strategic product management and ESG at JPMorgan Asset Management, is open regarding suggested inconsistencies in the industry. She says the firm works on a “case-by-case” basis.

“If we feel that a company is aligning their business with a two-degree scenario, for example, and the management is talking about it and making changes, then we may not support a shareholder proposal that forces them to disclose what they are doing,” says Kramer. “Where we will support a proposal is when a company has a high degree of exposure, is not looking at the impact to its company and is not taking measures to address our concerns.”

Indeed the largest managers say that many of their concerns are dealt with during their engagement process, which by its nature is more nuanced. Glenn Booraem, head of global fund corporate governance at Vanguard, says voting is just part of a larger continuum of engagement: “There is a lot of attention on shareholder meetings and votes, but for us they serve as part of a long-term discussion with companies, which is much less visible perhaps.”

For example, Booraem points out that while it voted on around 10 proposals regarding board diversity, the issue was discussed at many more companies.

“Engagement gives us the ability to get into the nuances that may not be reflected in a binary vote,” he adds.

Indeed, one shareholder points out that a vote passed for female representation on the board of one women’s retail company resulted in the chairman putting his wife on the board. In that case, engagement would have played a more positive role than just a vote.

|

|

Rakhi Kumar, State Street Global Advisors |

Rakhi Kumar is head of ESG investments and asset stewardship at State Street Global Advisors. In contrast to Huber, she says that voting can be something of a grey area. “Companies have more information about themselves than we do,” she says. “They give us insights and we can ask for more information, but sometimes we have to accept we may not know exactly what is happening, and management may be making the right decision. In which case, then it becomes a phased engagement where you assess a company over a two-year period perhaps.”

The point is, she says, “it can’t always be black and white.”

It is easy to see from an asset owners’ perspective that saying ‘we’re engaging’ can seem opaque and not as concrete as a vote. As You Sow’s Behar says it would be helpful to see the minutes of engagement meetings, while Ceres’ Logan notes: “That argument would have more credibility if asset managers were willing to disclose how their engagement has actually moved companies.”

Kamonjoh says that information would be particularly useful around close votes. He points out that if BlackRock and Vanguard had voted in favour of the two-degree proposals at Southern Company and PNM Resources, then the proposals would have been approved. At Southern, shareholder support for the proposal was 46%; at PNM, investor support stopped just short of a majority, at 49.9%.

“They can talk about their engagement efforts, but when shareholder support is so significant then it seems counterproductive to claim they are working behind the scenes to improve disclosure practices,” says Kamonjoh. “In these instances, the ‘against’ votes merely serve to delay action by the companies’ boards. [They] deserve a better explanation.”

State Street puts out a quarterly newsletter for clients that discusses how it has voted and the steps it has taken around engagement. Among fund managers with assets of over $1 trillion, it is the firm that seems to have struck the best balance between maintaining strong relationships with companies and with its asset owners. Kumar has a lot to do with that, but State Street began a little earlier than its largest peers in addressing engagement on climate risk.

While State Street may have voted for more than 60% of climate-related proposals last year, we may be unlikely to see it reach 100%.

“If you always vote the same way, you risk deterring companies from having open conversations with you,” says Kumar. “And as a passive investor with no ability to divest, it’s important to keep a dialogue going. It’s a long-term relationship.”

Biggest shift

Keeping a dialogue going with asset owners is now seen as being as important as the dialogue with companies; it is probably the biggest shift that the world’s largest asset managers have made. In the case of Vanguard, chief executive Bill McNabb published a letter to public companies globally at the end of August stating what it expected from boards on governance, diversity and climate risk. The letter, although not directed at asset owners, may as well have been.

Booraem says it has been a conscious effort: “This year, we decided to invest more in telling our engagement story and further explaining how and why we engage on certain topics.” For example, Vanguard included engagement case studies in its 2017 report.

Edkins says BlackRock is also now making sure it communicates its stewardship strategies more publicly: “We’ve always had a definitive strategy around engagement and voting, it’s just that we were never expected before to publicly disclose much of this information. In addition to our voting guidelines and quarterly reporting, we now also put our engagement priorities on our website, for example.”

This year, State Street put out two papers explaining its policy around stewardship and the business case for adapting for climate change. Indeed, the fact that nearly all large asset managers approached by Euromoney were not just willing but keen to speak in detail about their stewardship (even when their track record on voting has been erratic) is more evidence that they have understood the importance of being transparent.

Some commentators suggest that transparency on voting could soon be mandatory. In Japan, it is now a requirement under the revised stewardship code for investors to disclose how they have voted on individual company AGM resolutions.

“Previously, the requirement was simply for there to be vote disclosure,” says Kerrie Waring, executive director at the International Corporate Governance Network. “I suspect the future revision in the UK might go the same way. And new requirements from the European shareholder rights directive call for the same.”

Laura Campos, director of corporate and political accountability at the Nathan Cummings Foundation, says questions about proxy voting policies should just be part of any conversation with a manager: “We need managers that are thinking about the long-term impacts on the portfolio – whether they are running retirement plans or managing endowments set up to exist in perpetuity – which means factoring in the move to clean energy and voting proxies accordingly.”

Asset owners like the Nathan Cummings Foundation are simply demanding more information. DeAM’s Huber says he has seen a growing number of more detailed requests for proposals (RFPs) from asset owners over recent years: “Three to four years ago, asset owners began to ask about the execution of voting rights. Two years ago they then began to ask what kind of policies we had in place, and in the last 12 months, they are asking how transparent we are around voting decisions and about our processes around engagement and voting.”

“The move from active to passive has put a lot more power in the hands of passive managers to influence companies” – Chris Greenwald, UBS Asset Management

Over the next three to five years Huber expects that asset owners will not only ask for transparency around engagement and voting, but they will also want to know exactly why managers voted the way they did and what the impact has been.

If passive managers think that they do not have to work harder for asset owners on engagement simply because they have to invest in an index, UBS Asset Management (UBSAM) is proving them all wrong. Like Deutsche, UBS has been clear about its larger strategic decision to become a leader in sustainable investing and so is focusing on engagement and voting in its asset management arm.

Now UBSAM is working to tweak passive portfolios to better reflect asset owners’ values.

Chris Greenwald, head of sustainable investing research at UBS Asset Management says: “Nest Pension Fund wanted to incorporate an assessment of climate risk into its passive equity allocation, so we worked together with our rules-based quant team and our own sustainable equities team to incorporate that risk into the portfolio while maintaining a low tracking error by reallocating the weight in favour of companies better prepared for a two-degree carbon reduction scenario in the future.”

UBSAM has developed proprietary scoring, as well as a fund vehicle for other clients that will launch later this year. Greenwald says engagement is still a key part of the strategy. Rather than just underweighting companies, UBS reaches out to management to explain why they have underperformed its metrics and the concrete steps they could pursue.

It is a big shift with passive management. Some companies, because they are a part of an index, have less motivation to react to shareholder proposals because they know they cannot be divested. But strategies like UBS’s would force them to take notice.

Greenwald says it is important for passive managers to realize the influence they can have: “The move from active to passive has put a lot more power in the hands of passive managers to influence companies.”

Ultimately it comes back to the vote, and Greenwald says the whole process with Nest made UBSAM take a deeper look at how it votes.

Walden’s Smith says while it is important to have global investment leaders seen to be talking about the issue, publishing papers on the topics and discussing their engagement strategies, voting is really where the commitment is best shown.

“Asset managers will tell you the dialogue they are having is more important than a vote,” he says. “We disagree and, while we feel positive about the move from uniformly voting ‘against’ to supportive votes on climate change, more improvement is expected.”

It would be helpful if asset owners, such as Nest Pension Fund, joined firms like Walden in being clearer about what they expect and want from their portfolio.

|

|

|

Kris Douma, Principles for |

Kris Douma, director of investment practices and engagement at the Principles for Responsible Investment, says pension funds and foundations need to take greater responsibility: “I have some sympathy with asset managers as often asset owners are complaining that the managers are not acting in line with their values, but it is rare that they clearly state what they expect.”

He suggests asset owners develop a clear policy around what they expect on voting and, if outsourcing management, then build those policies into the selection process and RFPs.

“Stewardship is the key part of the fiduciary duty of an asset owner – it just can’t be thrown onto the asset manager,” says Douma. “They have to communicate what they want – not in press releases or conferences, but in the selection of their managers.”

So far, only large US west- and east-coast pension funds and a handful of European funds do what Douma is suggesting. Lothian Pension Fund is one.

As part of the tendering process for new manager selection, the pension fund scores managers on their approach to responsible investment, whether they have a strong record in voting, a strong record in engagement and how they integrate ESG issues into the core of their processes.

Managers are permitted by Lothian to carry out their own voting and engagement, and are expected to provide regular reporting on their activities.

“They are asked to respect Lothian’s values and engagement targets in the voting of underlying shares held by Lothian,” says the pension fund’s chief executive Clare Scott. Those managers unwilling or unable to comply with these requirements pass responsibility for voting and engagement back to Lothian, which uses third-party provider Hermes to undertake voting and engagement on its behalf. Scott says if the investment team at Lothian is unhappy with the performance of a manager in this area, a first step would be to engage with management: “In the event that we were unable to come to a satisfactory conclusion, we would move voting and engagement in-house.”

Catherine Howarth, chief executive of ShareAction, agrees that responsibility lies with the asset owners. Her organization has been providing asset owners with information on how their managers are voting and how the companies they are invested in are responding to calls for greater climate risk disclosure.

“Information is power, and more information is being brought to the public attention on shareholder proposals and how asset managers have voted around those proposals by the likes of us and organizations like Ceres and 50/50 Climate Project,” says Howarth. “That means asset owners now are armed with what they need to make decisions and are empowered to open discussion at meetings. They have to take responsibility now, and many are.”

“It’s a hollow argument to defend inactivity based on the notion that you will risk offending some of your investors” – Matthew Weatherly-White, The Caprock Group

Some pension funds like Denmark’s ATP have even dropped external asset managers so that they can have better control over the voting process. ATP, which has some $136 billion in assets, also moved its investments from derivatives to cash shares so it can vote.

More pension funds are likely to follow this route if their asset managers do not start representing their values through voting.

It is this word “values” that really seems to be causing some of the friction between asset managers and asset owners, however.

Balancing values

Asking companies to disclose climate risk planning or to add diversity to their board is seen as an expression of a pension funds’ values. But some asset managers appear fearful to be seen as representing any particular set of values in case they upset a client with different ones.

Kramer, for example, says JPMorgan is unable to take “a singular view on values” because those of its clients and employees differ. Vanguard’s Booraem echoes her point.

To some extent it seems to be a regional or cultural difference. DeAM and UBSAM are both clear that their firms’ support diversity and protecting the environment, so there is little to debate. Similarly, asset managers in New Zealand, Australia and Japan have accepted protecting against the impact of climate change and encouraging diversity is not really a ‘value’ but rather ‘a norm’ – driven largely by asset owners.

Indeed, this argument by the US houses of not wanting to represent one value over another seems dubious – particularly as some seem to simply defer to Institutional Shareholder Services’ recommendations for voting on more qualitative issues rather than take responsibility.

“It’s a hollow argument to defend inactivity based on the notion that you will risk offending some of your investors,” comments Matthew Weatherly-White, co-founder of multi-family office the Caprock Group. “The market rewards leaders and innovators. They may seem to some as wild-eyed activists, but I think those who stand up to support gender equality, fair representation and not damaging the environment will be seen to have stood on the right side of history.”

|

| Glenn Booraem, Vanguard: “There is a lot of attention on shareholder meetings and votes, but for us they serve as part of a long-term discussion with companies, which is much less visible perhaps” |

Nonetheless, the big four all say that they have to lead with economics and not ideology.

“The 20-odd million clients we have likely have views that span the ideological spectrum, so it makes sense for us to act in line with investment success first,” says Booraem. That said, Booraem hints that this idea of ‘values’ can be circumvented if more data can be found to point to the positive impact on financial performance on diversity and addressing climate risk.

He says that recent data has helped his firm make more of a case for going against management: “We need the research above all, and that research is emerging.”

Of course it would be much easier for asset managers to vote in line with shareholder proposals on climate disclosure if more research were available. It would also be easier for asset owners to hold asset managers to task when they did not.

“We all know it’s a risk, but until you can measure it, how can you know how to value it? We’re all in a learning phase here,” says Kumar.

One head of ESG adds that the US asset managers have tended to vote based on past performance. Obviously that data is easier to point to, but he makes the case that it is preferable to take a forward-looking approach: “Having the right people on board who are well diversified over a period of three to seven years is more relevant, if perhaps more time consuming to consider, and the data less quantitative for now.”

Douma at Principles for Responsible Investment agrees that data is a challenge that is perhaps hindering the move by large asset managers to vote against corporate boards when it comes to climate change and board diversity, but believes that the shift to more quantitative data is coming.

However, that data needs to come from the companies themselves.

Drew Hambly, head of shareholder voting at Morgan Stanley, says his firm has been pushing for greater disclosure from companies: “It seems reasonable to ask for enhanced disclosure around water use, energy use or greenhouse gases if we feel a company is lagging its competitors. Not that performance is not important anymore, but we are more focused on getting relevant disclosure we may use to help us analyze a company’s risk profile and future performance.”

Hambly says he has seen an improvement in disclosure from companies: “If you look at the S&P500, 80% of its companies have a CSR report, which is a big improvement from five years ago. Some are better than others, but this is certainly a move in the right direction.”

The challenge, says BlackRock’s Edkins, is knowing what to provide to investors: “Undoubtedly, we are moving towards greater transparency, and some companies are going beyond what is required of them by regulators. But we need a deeper discussion around what information would be helpful for investment and stewardship decision-making. I have some sympathy with companies that are suffering from fatigue from the wide range of queries coming at them. We have to start somewhere of course, but there is also a need to crystallize the information that is required.”

“It seems reasonable to ask for enhanced disclosure around water use, energy use or greenhouse gases if we feel a company is lagging its competitors” – Drew Hambly, Morgan Stanley

Standardization of reporting and information would be useful and could be on the way. PRI recently met with seven investment organizations and eight corporate reporting organizations to look at moving towards standardized reporting for ESG issues.

“There won’t be a backslide around transparency,” says Hambly.

Given the hires that the asset managers are making, it seems unlikely there will be a retreat from the progress made in the 2017 proxy year.

Edkins says BlackRock added seven to its investment stewardship team last year, taking the total to 31 – double what it was in 2009 – and will be adding more.

Booraem says Vanguard has doubled its stewardship team to 20 over the last few years and is continuing to expand.

Kramer seems to be trying to bring JPMorgan up to speed (smoothing the imbalance of a 75% focus on governance and just 25% on environmental and social engagement) and integrating ESG more broadly across the company with the formation of the Sustainable Investment Leadership team last year.

ShareAction’s Howarth says the true test will be whether or not the likes of BlackRock, Vanguard and Fidelity will be willing to escalate the pressure by voting for board changes if Exxon and Occidental do not change post vote.

“Are they going to hold these companies to a higher standard?” she asks.

She points to Legal & General Investment Management as a standard bearer. It has pledged to divest from active portfolios and to vote against the chairs of companies that are unresponsive to shareholder calls for action. While passive funds cannot divest, they could certainly make changes on the board.

Behar adds: “If companies don’t follow up and engage in a material way with proponents after there have been majority votes against them, then it is my hope asset managers will deliver no-confidence votes against the entire board to open up some seats and bring in more competent and future-thinking board members.”

Edkins says BlackRock will take further action: “Most companies will take a vote against management seriously and they also understand that BlackRock is going to be an investor for the foreseeable future so would want a supportive relationship. But in the case that companies still weren’t moving in line with our request, then we would escalate it by voting against the leadership or chair of the committee. It is our view that the board of directors is responsible for ensuring shareholder interest is protected. If we don’t feel they are doing that, then yes, we should and would vote against re-election.”

The 2018 proxy voting season should an interesting one.