In the post-Lehman orgy of portfolio flows to emerging markets (EMs), policymakers found themselves grappling with the macroeconomic fallout: currency appreciation – in the absence of aggressive FX interventions by central banks – decimating nascent manufacturing industries, rising inflation and potential asset bubbles. The fallout was so severe it triggered the now infamous remark from the Brazilian finance minister Guido Mantega of an “international currency war” with the Fed’s QE policy, serving as a backdoor route to weaken the dollar and boost the US’s export competitiveness.

At the heart of the EM challenge was the economic policy conundrum known as the “impossible trinity”. This states it is impossible for countries to manage their exchange rates, boast an independent monetary policy and allow the free movement of capital, all at the same time.

Portfolio flows to high-yield markets in South America and Asia heaped on inflationary pressures and domestic credit growth, while interest rate hikes to redress the situation sucked in more capital.

This pro-cyclical policy response, combined with a lax fiscal stance and structural-reform inertia, helped drive the EM rout in recent months in current-account deficit nations. When external liquidity vanished, the impossible-trinity challenge went into reverse as capital fled these markets, imperilling exchange-rate stability.

Historically, China has bucked the impossible-trinity dilemma thanks to its nominally closed capital account, and achieved monetary autonomy thanks to costly open-market operations and reserve requirement ratios as sterilization tools.

However, moves to boost offshore trading of the renminbi in Hong Kong in recent years, dubbed the CNH market by traders, highlights how Beijing is taking meaningful steps to cast the renminbi as a trade and investment currency – but that has come at a cost of policy flexibility and heaped on new financial risks.

For all intents and purposes, China’s capital account is de facto more porous than markets appreciate and, as a result, it faces the impossible-trinity challenge – a key and under-appreciated factor in the likely success of rebalancing its economy.

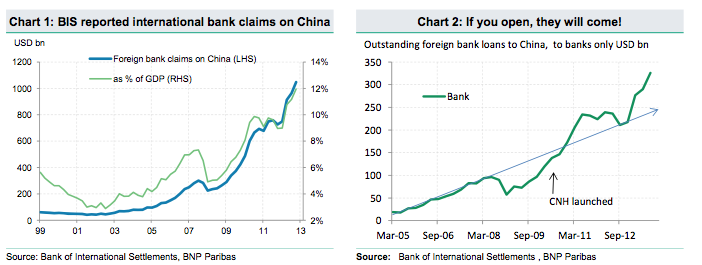

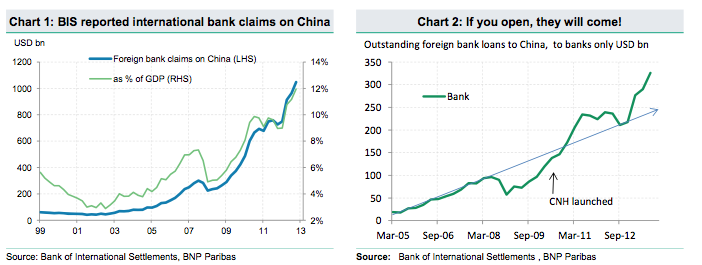

As Euromoney has reported, the surge in international bank exposures to China during the past five years, fuelled by the development of the CNH market, means, in effect, China’s capital account is effectively open, with gross international-bank exposures to the country now at $1 trillion, representing 12% of GDP.

During the past 12 months alone, international banks ramped up their exposures by $320 billion, representing 4% of China’s huge economy, driven by the RMB carry trade and tightening of credit in the shadow-banking system.

Analysts at BNP Paribas say the cross-border lending party has much more room to grow without regulatory redress, which is unlikely as Beijing is moving towards capital-account liberalization.

“How does the explosion in cross-border lending relate to the CNH carry trade?” they ask. “Most directly, the trend is linked to the difference between money-market rates onshore and offshore. Foreign banks can borrow in USD or in CNH – where they are naturally borrowed against clients’ offshore deposits – and remit the funds onshore where they would earn higher interest.

“Similarly, Chinese banks often issue CDs [certificates of deposit] in the CNH market, and the funds are ultimately used onshore – so the cheaper they can raise CDs, the larger the incentive to issue.”

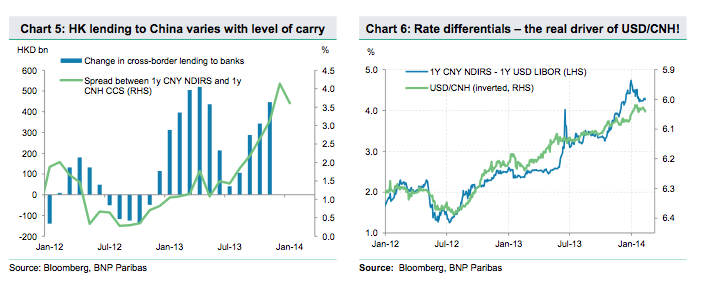

They add: “Empirically, the pace at which foreign banks lend to China is a function of the spread between onshore and offshore rates (see chart 5). Note that thanks to easing of curbs on backflow of RMB and cross-border lending, the only real hurdle to cross-border lending is banks’ internal country and risk-management limits.

“In theory, the carry trade can go on indefinitely, until a shock to the system or a change in regulations causes a major disruption.”

As a result, China’s capital controls are “defunct”, say BNP analysts.

There are three broad macro issues.

Firstly, the recent RMB volatility is an outcome of this impossible trinity or “trillemma” – the struggle to balance its exchange rate and growth objectives while mitigating against excessive speculative capital flows.

In other words, a steadily appreciating renminbi has triggered an explosion of speculative capital inflows, highlighted by the premium the offshore CNH trade demanded against the onshore CNY. As a result, Beijing has sought to add two-way risk to the currency, as demonstrated by the mid-March move to widen the CNY’s daily trading band.

Secondly, the policy to trigger RMB volatility – to temper capital flows and reduce sterilization costs aimed at addressing imported inflation – will imperil efforts to stabilize Chinese growth in the years ahead.

Put another way, the move to remove the one-way bet on the currency – a function of Beijing’s trillemma of controlling the exchange rate, money supply and allowing capital flows all at the same time – comes at a cost, says David Lubin, head of EMs research at Citi.

“One element of the ‘Chi-lemma’ will be to make sure that more exchange-rate volatility doesn’t come at the expense of a sudden slowdown in credit growth that could squeeze the economy,” he says.

“That challenge will be particularly difficult at a time when the front-end of the US yield curve might shift up in the next few months: rising short-term interest rates in the US might erode banks’ willingness to roll over their cross-border loans to borrowers in China, especially when there is more uncertainty about the path of the exchange rate.” (For more on China’s tapering challenge, go here.)

Thirdly, another unique aspect of Beijing’s trillemma – other than the extraordinary pace of the speculative flows to the country in recent years – is its bid to promote the renminbi as a truly international currency, from a trade, investment and reserve perspective.

Says Lubin: “Financial liberalization and an opening of the capital account will be needed to shore up the RMB’s attractiveness now that the days of the one-way bet are past. Chinese policymakers seem committed to this. But liberalizing the capital account will be a tough challenge for China when the direction of flows is likely to be outwards rather than inwards.”

In conclusion, in the medium- to long-term, China’s RMB policy will be key in determining how it rebalances its economy, but there will be costs involved. In the short-term, Beijing can’t control both the RMB and capital flows since cross-border lending is driving carry-trade flows and putting upward pressure on the currency – a noxious cocktail that has caused hangovers in other EMs in recent years.