Largely unnoticed by global markets, Germany has undergone a profound shift in its economic model in recent years that has sown the seeds of deteriorating competitiveness and declining business investment that suggests the eurozone’s largest economy will struggle to replicate its pre-global crisis growth rates.

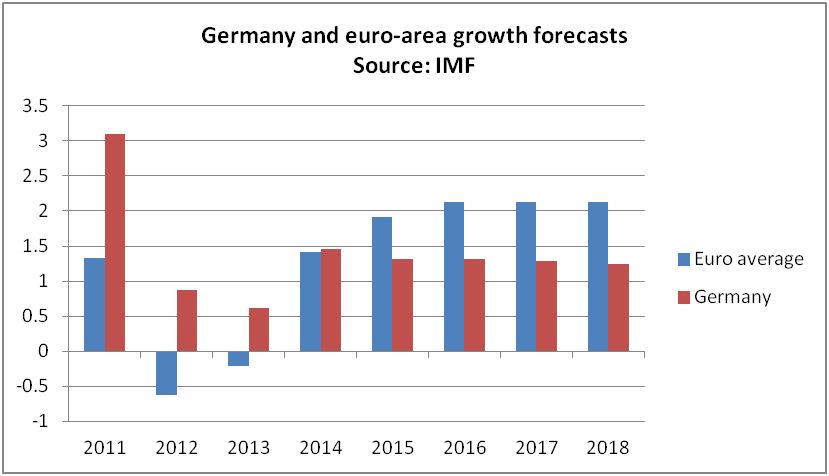

Germany accounts for 29% of euro-area GDP, reflecting the weight of the German economy on the rest of the eurozone. Largely thanks to base effects and weak German exports, the IMF forecasts the eurozone to outgrow Germany as soon as 2015 (see graph below).

|

The German economy marginally avoided a recession in Q1 2013, after posting only 0.1% growth, while 2012 saw Europe’s largest economy grow by 0.9 %.

Sylvain Broyer, head of economics at Natixis, says Germany’s post-global-crisis growth potential is wavering amid challenging demographic and labour market trends.

“The problems in Germany are the demographics: the country’s population is shrinking and potential growth is very difficult to hold at the current level,” he says. “There was a positive boost on potential growth due to the reform drive of the last decade, but that’s over and now it will be difficult for Germany to compensate the demographic trends with more reforms.”

However, the knock-on effect from rising real wages and declining labour productivity appears to be weighing negatively on economic growth and corporate profitability, according to a report by Natixis.

The bank notes that rapid real-wage growth has outperformed labour productivity growth, and has brought with it a rapid decline in corporate profitability since 2010, a 2% decline in Germany’s market share in global trade and a slowdown in employment growth since 2011.

“Real wages are rising faster than labour productivity; profitability and competitiveness are deteriorating; business investment is declining; exports are stagnant; growth is driven by household demand; asset prices are rising,” states a report by Natixis.

“The question is whether this new growth model is worrying for Germany; how soon will we see the negative effects of this model on market shares, capital accumulation and employment? The most worrying part for Germany is the rapid loss of profitability due to the fact that real-wage growth is markedly higher than productivity growth.”

However, despite calls for a hike in German consumption to boost exports from the periphery, the increase in German consumption is unlikely to have a positive impact on the rest of the euro-area, given the structural nature of the eurozone debt crisis, according to Broyer.

“The relativity of Spanish, Italian or Portuguese exports to German GDP and German domestic demand is very low, although it’s better to have good consumption than weak consumption, but it’s not the way out of recession for the periphery,” he says.

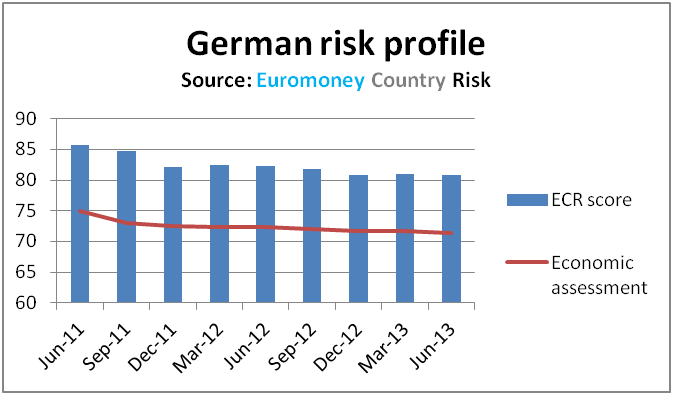

The latest results of Euromoney’s Country Risk Survey signals rising German risk perception, after analysts downgraded the country’s economic assessment for the ninth consecutive quarter (see graph below).

Germany’s economic score fell 0.4 points in Q2 2013 and by one point year-on-year, as analysts downgraded four of the country’s economic indicators, bar government finances.

Its deteriorating economic fundamentals have left the country’s overall risk assessment falling by three points since June 2010 (see graph below).

With an ECR score of 80.9 and a global rank of 13, Germany is now perceived to be riskier than Australia, New Zealand and the Netherlands. Germany’s deteriorating risk assessment means the sovereign was the third-worst AAA performer in the survey year-on-year and is the second-riskiest AAA sovereign, after neighbouring Austria.

|

Nicolas Firzli, director-general at the World Pensions Council and one of ECR’s expert contributors, attributes Germany’s riskier dynamics to under-investment in public infrastructure.

“Germany has invested 30% less in public infrastructure in GDP terms than the US and the EU average,” he says. “Germany has now reached a point where it probably has nearly exhausted its growth by labour cost-cutting and aggressive-deregulation potential.

“The delayed appearance of this infrastructure bottleneck comes at the worst possible time for Germany and the rest of the European Union.”

Firzli adds: “Tellingly, DIW Berlin, the country’s leading economic research institute, published a particularly harsh report last month showing how the country’s lack of investment in modern railroads, energy infrastructure and social housing in the past 10 years may have a very negative impact on the ability of Germany’s economy to grow.”

The core tenets of the study are summarized by Marcel Fratzscher: Investment for More Growth: An Agenda for Germany’s Future.

This article was originally published by ECR. To find out more, register for a free trial at Euromoney Country Risk.