Sanusi Lamido Sanusi, governor of the Central Bank of Nigeria, has made the reinvigoration of Nigeria’s payments system, and the reduction of its reliance on cash, a priority of his governorship.

The policy is intended to increase the country’s economic sophistication, closing the gap on – and ultimately overtaking – the west in payments convenience and security.

In the short term, the “cashless policy” is designed to improve Nigeria’s tax collection and enhance control over FX flows. By making payments more traceable, it should also help to reduce corruption – one of the primary reasons Sanusi has pushed these changes.

The scheme imposes caps and penalties for transactions involving more than N500,000 (€2,000) daily or N3 million for corporates. Exceeding this limit draws a 3% penalty fee – or 5% for corporates – charged by the bank.

Introduced as a pilot scheme in Lagos in 2012, on July 1 it was extended to Ogun, Rivers, Anambra, Abia, Kano and Abuja.

|

The policy has begun forcing more transactions on to electronic payments, from a very low base, and there are around 120,000 point-of-sale (POS) electronic payment machines in the country. Sanusi has a said biometric authentication of POS terminals and ATMs will be introduced in 2015.

The value of POS transactions grew from N100 million in May 2011 to N3.34 billion in May 2013, according to Globasure, a Nigerian payments systems vendor.

However, this is still a small number of machines for such a vast and populous country at 180 million.

Even ATM machines are hard to come by for those wishing to use banks. There are 12 ATM machines per 100,000 Nigerians in the country, says Globasure, compared to 169 per 100,000 Americans.

Nevertheless, whether intentionally or not, the policy might be contributing to a shortage of smaller currency denominations, with reports on the ground suggesting local merchants are struggling to provide change for cash transactions.

The changing face of Nigerian cards is also helping to bring corruption and fraud under control.

“The change from magnetic stripe-based cards to chip-and-pin-compliant channel and tokens in 2010 has resulted in over 90% reduction in card-related fraud incidences,” says Bola Adesola, CEO at Standard Chartered in Nigeria.

Another flagship policy is the phasing out of commission on turnover, a charge of N5 on every N1,000 credited or debited to a retail Nigerian current account. This is to be reduced to three per mille this year and two per mille in 2014, one per mille in 2015 and then abolished in 2016.

“This is forcing Nigerian banks to think and be more creative” by removing this easy income for which they do not have to work, says Charles Weller, Nigeria country head at Deutsche Bank. “It will make them more delivery orientated by taking away their easy income.”

Ultimately, it should lead to increased choice and sophistication in the Nigerian bank market, bring many of the country’s unbanked into the system and improve services for all.

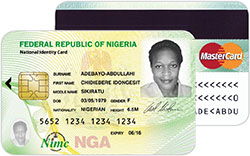

There are other initiatives being piloted too. One, pioneered by MasterCard and the government, provides Nigerians with a National Identity Smart Card, simultaneously an ID and electronic payment card.

Announced in May, this represents the largest roll-out of a formal electronic payment system in Nigeria and the broadest financial inclusion initiative of its kind in Africa, according to MasterCard.

The card is being given to Nigerians aged 16 and older and foreign residents in the country for more than two years. It is accepted in 210 countries and territories, at more than 35 million locations around the world, according to MasterCard.

In addition, in July, the central bank commenced with image-based clearing to reduce the clearing cycle for cheques – a payment system most Nigerians are comfortable with – to one day.

In the same month, United Bank for Africa introduced personalized debit card All About U, allowing customers to personalize their payment card with a photograph of their choosing, a service that has been offered with some success in Europe and elsewhere.

Ultimately, monetary authorities in Nigeria will continue to drive electronic payment systems to reduce banks’ and customers’ transaction costs, boost transparency and sharpen policy tools to control domestic credit conditions.

Nevertheless, Nigeria’s payment culture is at a nascent stage, with few customers tied to existing systems, which means there is a healthy battle between cards and mobile money.

Although card-use is growing and making headway into the rural areas, mobile money has much greater potential in Nigeria, says Sachin Shah, head of cash management, at Standard Bank Group.

Cards will be disintermediated as they are squeezed on both sides, he concludes, with smaller transactions gravitating to mobile money, and larger sums transferred between bank accounts.