Since the onset of the global financial crisis, Fitch, Moody’s and S&P have come under much scrutiny, criticized for failing to assess the creditworthiness of sovereigns, financial institutions and mortgage-backed securities.

The rating agencies were then cast as the villains of the eurozone crisis after relegating Portugal, Ireland and Greece to junk status in 2010, triggering a pro-cyclical hike in sovereign borrowing costs in the euro-area and a global market maelstrom.

As a result, US and European regulators, through the European Securities and Markets Authority and the Dodd-Frank Wall Street Reform and Consumer Protection Act, have taken draconian measures to boost ratings transparency and diversify the playing field.

|

| Ewen Cameron Watt, BlackRock |

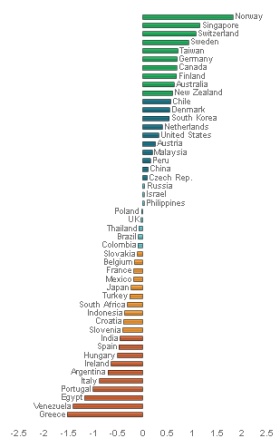

While new indices have been developed to provide alternative views on bank-creditworthiness, the BlackRock sovereign risk index (BSRI) offers an alternative benchmark for tracking sovereign credit risk.

Since this index hails from the world’s largest investor – with $3.8 trillion of assets under management – it’s worth closer inspection. The index, devised two and a half years ago, was created by BlackRock because it viewed other market analysis, including that by the ratings agencies, as being too simplistic, explains Ewen Cameron Watt, chief investment strategist at BlackRock.

“Rating agencies tend to lag behind the curve. In practice, markets and credit default swaps changes long before an agency change its sovereign outlook.”

Gathered from publicly available financial data, the index uses more than 30 quantitative measures, with qualitative insight from third-parties to compliment the data. Indeed, Moody’s, Fitch and S&P are much more qualitative and committee-based in their decision-making process, and are sponsored by the sovereigns, whereas BlackRock isn’t.

The index is made up of four main categories that count toward a country’s score and ranking. Fiscal space, including such metrics as debt-to-GDP and dependency ratios, accounts for 40%. Willingness to pay, which measures the government’s effectiveness and stability, accounts for 30%. External finance position, or the country’s exposure to foreign currency debt, is weighted at 20% and financial sector health accounts for 10%.

The index covers 48 countries in the relative ranking. “A country’s ranking might improve either because factors specific to the country have improved or because factors specific to other countries have deteriorated,” says Watt.

BlackRock is wary about introducing more, smaller economies on to the index. “[Data derived] in smaller countries can be of lower quality and this would affect the rating of all the other countries because the results are all relative to one another,” says Watt.

The index influences portfolios depending on the needs and mandates of BlackRock’s clients, explains Watt, declining to clarify further, and it is also a standalone product devised to enhance BlackRock’s proprietary research. “When you are paid by an investor to manage their money, acting on third-party decisions is not good enough,” he says.

In the most recent note, according to the index, the external finance scores of most emerging markets, including China, Thailand and Malaysia, are deteriorating, while euro-pessimism might be on the wane as the BSRI scores of Spain, Ireland and Austria have jumped due to improvements in their fiscal space and external-finance scores.

In addition, the “deteriorating” position of France is noted in the index. “We have noticed a gradually deteriorating trend in our model for France over several quarters,” says Watt.

While Watt notes it is important not to paint all emerging markets with the same brush, and that there is “great divergence” between them, the fact the index uses the same criteria to measure developed and emerging markets could cause methodological problems, a challenge vexing all endeavours to capture government creditworthiness.

Richard Segal, head of international credit strategy at Jefferies, says: “It is very difficult to create a model which can accurately index a developed economy as well as a developing economy. Although lots of risk models rely on indicators such as debt/GDP, it is complicated to mix developed and emerging economies here because GDP is often a proxy for revenues and the revenue-to-GDP ratio is not stable across countries.

“And if you have both debt/GDP and debt/revenues as variables, you’re over-counting the importance of debt.”

Moreover, the weightings and the criteria used could be subjective, creating bias results, says Segal. “Not everything needs to be included in the index, but most things need to be considered,” he says.

Nevertheless, while Moody’s, Fitch and S&P hold 95% of the markets share, there is growing demand for different agencies to offer a variety of products, notes Segal.

More importantly “different indexes should be used to compliment the work of the rating agencies, which are often misused”, he adds.

“S&P, Moody’s and Fitch should all be utilized in a specific way – to measure the default risk on government debt,” says Segal. “Ultimately, when they are overused or misused to measure risk in certain areas, they become blamed for more than what’s actually their fault.”

|

| BlackRock Sovereign Rate Index June 2013 |