What’s in a number? When it’s $10 trillion, maybe quite a lot. Three instances of it in January – one on the way down, one on the way up, and one an aspiration – might tell us something about 2022 and beyond.

First, the way down. Negative-yielding debt – the stuff that JPMorgan chief executive Jamie Dimon hates with a passion, saying in 2019 that there was something irrational about buying it – finally fell back through $10 trillion in mid January for the first time since the early days of the coronavirus pandemic in April 2020.

That matters because while negative-yielding debt peaked at nearly $18 trillion at the end of 2020, it is now back to where it stood at the start of the pandemic. In the intervening period, its seemingly inexorable rise has been the basis of the Tina trade – that There Is No Alternative to piling into stocks as central bank policy presses down on returns that investors can expect from bonds.

If anything captures the lay of the land right now, it might just be that $10 trillion number

A slew of rate rises this year are now taken for granted. Dimon thinks there could be as many as seven, although, not for the first time, he is an outlier. The US Federal Reserve said in December that it envisaged three hikes in 2022; markets are pricing in four.

Debate is raging over whether that will kick off with 50 basis points in March, as Pershing Square Capital Management chief executive Bill Ackman would like, or a more sedate 25bp. Ackman told his Twitter followers in mid January that the Fed would need the bigger move to tackle “the unresolved elephant in the room” – the central bank’s loss of credibility in fighting inflation.

On the up

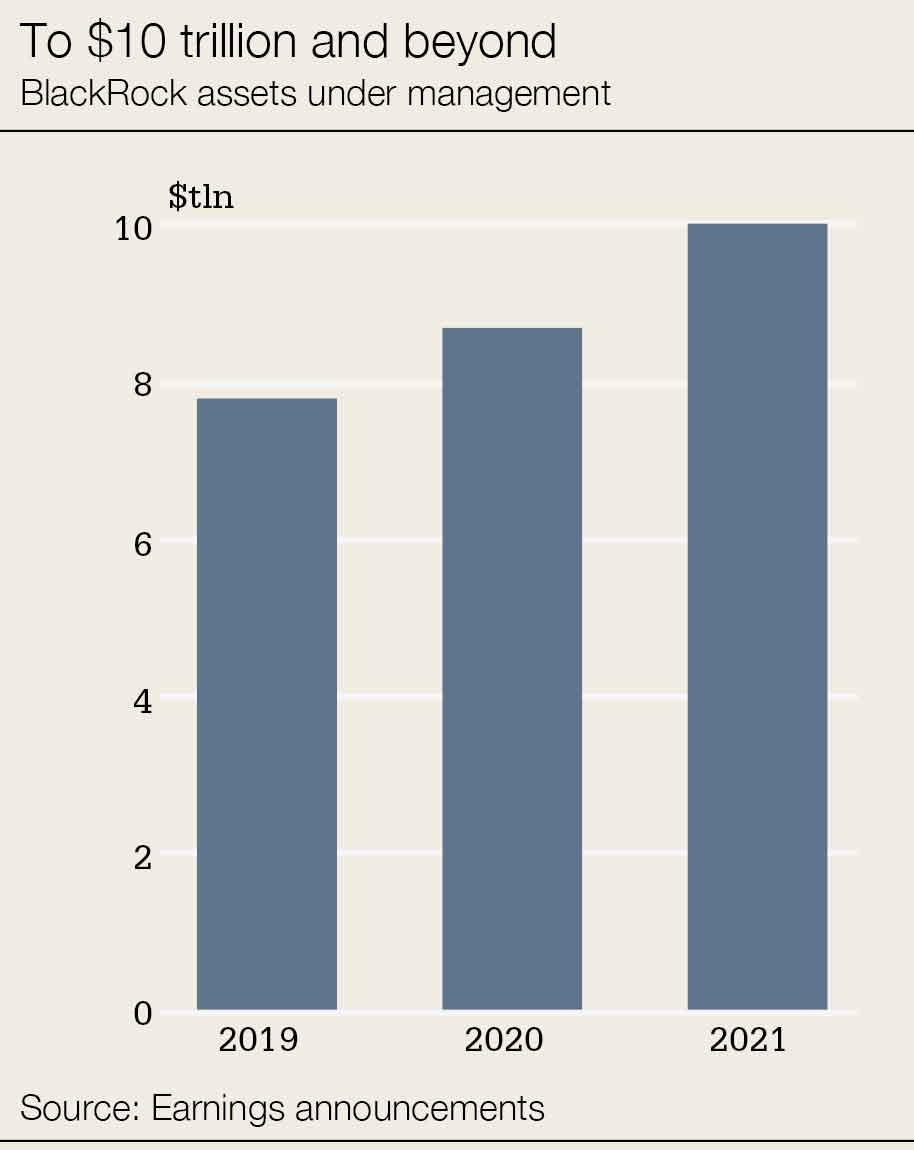

Now, the way up. BlackRock’s assets under management (AuM) ended 2021 at $10.01 trillion, according to its annual earnings report on January 14, after rising by $1.33 trillion in the last 12 months.

It is the first time that a listed fund manager has broken through the $10 trillion level. Remarkably, BlackRock’s AuM stood at a mere $5 trillion as recently as 2016.

The latest result underscored not only the ‘everything rally’ in markets but also how phenomenal the surge of flows into asset managers continues to be – some $104 billion of net inflows came into BlackRock’s exchange-traded funds (ETFs) in the last quarter of 2021 alone.

What chief executive Larry Fink liked most about BlackRock’s growth in 2021 was the diversification he is getting from a rise in active strategies – some 60% of the organic fee growth that year was from actives, he told investors. For BlackRock that’s encouraging when set against the wind-down of Tina, an environment that ought to favour firms able to perform in the more thoughtful business of actual money management rather than acting as custodians of passive funds.

And what of the aspiration? Morgan Stanley – which saw its shares perk up a little on January 19 after it reported revenue and pre-provision profit increases in 2021 that were bested only by Goldman Sachs among its bulge-bracket peers – says it wants to hike its wealth and investment management client assets to $10 trillion.

That’s a hefty increase from the $6.5 trillion level that the firm stands at now, and it says a lot about where chief executive James Gorman sees the firm heading as conditions normalize from the monetary policy-driven bonanza of 2020 and 2021.

Gorman had already spent years changing the balance of the firm’s business before the pandemic. As we showed in our February 2020 analysis of revenue diversification at the 12 biggest global corporate and investment banks since the global financial crisis, in 2019 Morgan Stanley’s investment banking and trading operations accounted for 48% of group revenues, down from 59% in 2006.

And excluding the outsized activity of 2020, that is roughly where they still stand, at 50% in 2021 – although pandemic conditions certainly helped the bank to get more bang for its buck, with the investment bank’s contribution to overall pre-provision profits rising from 49% in 2019 to 60% in 2021.

Even before the expected reset of industry-wide capital markets revenues after the pandemic glut, Gorman knew that the big growth opportunity for Morgan Stanley lay elsewhere. Of the $11 billion year-on-year revenue increase that the firm enjoyed in 2021, $7.6 billion came from jumps in the bank’s asset and wealth management divisions.

That comparison was admittedly skewed by the integration of investment manager Eaton Vance, which it acquired last year, but if Morgan Stanley is now pulling in those revenues on AuM of $6.5 trillion, then hitting Gorman’s target of $10 trillion would suggest another $11 billion uplift in revenues to come – all else being equal.

No cheer

The continuing diversification at Morgan Stanley shouldn’t give competitors much to cheer, however. It is hardly going to be dialling back its formidable investment bank. Others with less impressive market shares have more room to grow on paper, but should not expect to be taking business from a firm like Morgan Stanley. The likes of Barclays, BNP Paribas and, yes, Deutsche Bank may have to fight over what leaks away from firms such as Credit Suisse and hope for a growing pie, even if their slice remains much the same.

Negative-yielding debt on the way down and the waning of Tina, the biggest asset managers ever more dominant – and resurgent in active strategies – and diversification the key for the big investment banks as capital market conditions normalize: if anything captures the lie of the land right now, it might just be that $10 trillion number.