Some problems are simply too big to ignore, no matter how hard you try. The Italian banks have tried very hard to ignore their non-performing loan problems for a very long time. Their €360 billion of bad debt is equivalent to one fifth of the country’s GDP, so it is hard to believe that turning a blind eye is going to work for much longer.

The European Central Bank certainly doesn’t seem to think so, and when it decided to write to the worst culprit of them all – Monte dei Paschi di Siena (MPS) – in July to demand that something be done, it lit a fire under a festering problem that is now large enough to undo the years of painstaking work that has gone into establishing a harmonised regime for bank resolution across Europe, the Bank Recovery and Resolution Directive (BRRD).

This is because their mountain of bad debts is preventing many banks from rebuilding their capital to levels that will satisfy their EU overlords. In a recent research paper entitled ‘Capital shortfalls of European banks since the start of banking union’, academics Viral Acharya, Diane Pierret and Sascha Steffen calculate that Italian banks have a combined capital shortfall of €97 billion in a stressed scenario, which corresponds to about 6% of GDP.

“The market is nervous about Italian banks, and rightly so,” says Gennaro Pucci, chief investment officer at PVE Capital in London, which bought €565 million worth of Italian NPLs between 2014 and 2016. “There are such a large number of losses in the system. When the numbers are this significant, you can’t just hope that it will go away.”

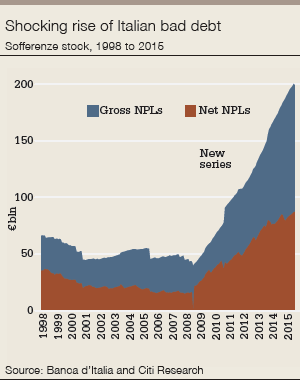

The number of total gross NPLs in Italy has increased by 160% since 2009; bad loans now represent 18% of all outstanding loans in the system, according to Citi. In 2009, just 8% of outstanding loans were bad. ‘Sofferenze’ loans, the worst performing category of NPLs, account for 60% of the total.

Its NPLs have made Italy the conduit for the market’s nervousness about European banks: UniCredit’s share price has tumbled from €6.45 in April 2015 to €2.40 today, while MPS has been all but wiped out – falling from €9.45 to €0.24 over the same period. This is despite the fact that the Italian banks’ capital levels are not actually the worst in the region. According to Acharya, Pierret and Steffen’s research, capital shortfalls as a percentage of GDP in the banking sectors of Germany, Spain and the UK are all worse than those for Italy.

Despite this, it is Italy that has been the focus of attention. “Italy is a wealthy country and was not as overdeveloped as Spain or Ireland. There is also a high savings rate. These positives may have allowed for a certain amount of complacency,” says Raoul Ruparel, co-director and head of economic research at think tank Open Europe.

Plans to establish a bad bank before the implementation of BRRD on January 1 proved fruitless, so the system needs to be fixed within the new stricter regulations. “If Italy had set up a bad bank at the same time as Spain or Ireland, they would have had to take bailout with conditions, and there weren’t many European leaders pushing for Italy to take a bailout at the time,” Ruparel recalls. “It is easy to criticise now.”

|

|

Gennaro Pucci, chief investment officer at PVE Capital |

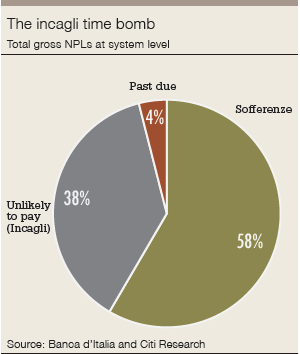

Pucci believes that the intense focus on the €200 billion of sofferenze loans is masking looming problems elsewhere in the system as well. Loans that are currently performing but are classed as unlikely to pay, known as ‘incagli’ loans, also present a dangerous threat to stability. According to Citi, in the third quarter of 2015 gross sofferenze accounted for 11% of banks’ loans.

Pucci says that they hold the same amount again as incagli loans that are likely to go bad.

“The market is focusing on €40 billion of losses in the system, but if you include incagli, or loans that are unlikely to be repaid, the figure increases to around €100 billion,” he says. “When incagli are taken into account, the Texas ratio [a measure of bad loans as a proportion of capital reserves] of all small and medium-sized banks in Italy is over 100, and the large banks are dangerously close to 100.”

A Texas ratio of more than 100% indicates that action on capital is urgently needed. MPS has a Texas ratio of 145%. Intesa Sanpaolo has a ratio of 85%, UniCredit 95%, Banco Popolare 135% and UBI Banca 110%. The risk is, therefore, that the market is woefully underestimating how many incagli loans will become sofferenze loans.

Urgent fix

The system urgently needs to be fixed before this happens. After lengthy negotiations, the Italian government revealed its €120 billion guarantee plan for securitized NPLs in February this year (Guaranzia sulla Cartolarizzazione delle Sofferenze, or GACS). The scheme was launched on April 15 and will run for 18 months, enabling banks to purchase a government guarantee for the senior notes of NPL securitizations, which will facilitate their sale to private investors.

The scheme does not count as state aid because the banks pay the market price for the guarantee, which is calculated using a basket of single name CDS on Italian issuers based on the underlying rating of the debt instruments. The price is determined using the mid-price of the basket over the previous six months. Given how wildly Italian bank CDS have moved in recent months, predicting the price could be a tricky business. Nevertheless, the fact that the bank has to pay a market-based price for the guarantee is key to getting around EU rules.

GACS only kicks in if the bank can sell at least 50% of the junior notes in the transaction to private investors and it can achieve accounting de-recognition of the NPLs. There remains some confusion over whether or not the guarantee can be enforced before maturity of the notes. JPMorgan and Mediobanca have calculated that use of the guarantee can shave around 200 basis points off the financing cost of securitizing the NPLs.

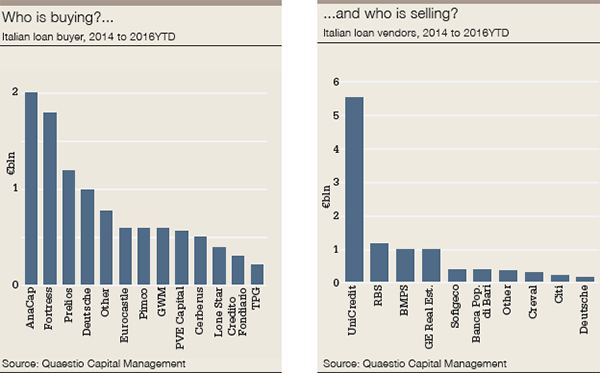

“Having the GACS guarantee may close a bit of the gap between seller and buyers, and may help facilitate a very large transaction,” says Justin Sulger, head of credit at AnaCap in London, which has been one of the most active buyers of Italian NPLs in the market, acquiring €2 billion-worth of loans since 2014. “However, rarely have we ever been in a transaction or negotiations with sellers where the lack of senior debt was the problem.”

This suggests that the guarantee could be being targeted at the wrong part of the capital structure altogether. Indeed, several NPL buyers report being deluged with offers of leverage for deals.

In January this year, Citi analyst Azzura Guelfi calculated the potential coverage ratio that would be required for a bank to transfer its sofferenze to a private buyer or securitization SPV. She found that the least impacted bank was Intesa Sanpaolo and the most impacted were Banco Popolare and Banca Popolare dell’Emilia Romagna. In terms of capital Banco Popolare and UniCredit were most sensitive to this additional cost. But Guelfi pointed out that the analysis only focused on sofferenze and that the impact could be different if any actions were taken on other categories, such as incagli.

Lightning rod

The situation at MPS has become the lightning rod through which the broader Italian banking crisis is being transmitted to the market. It also embodies the inherent contradiction in applying a pan-European resolution regime to banking systems that are in wildly varying states of health across Europe.

MPS, the 544-year old Tuscan bank, has a capital shortfall of anywhere between €0.6 billion and €3.5 billion in an adverse scenario, according to Credit Suisse analysis. When the European Banking Authority published the results of its EU-wide stress tests for 2016 on July 29 the Italian lender was far and away the most troubling institution in the mix.

In an adverse scenario it would actually record a negative common equity tier-1 ratio of -2.23%, down from 12.01% at the beginning of 2015. The ECB’s decision to write to MPS in early July demanding that it reduce its net NPLs from €23.5 billion to €14.6 billion over the next two years brought the situation to a head. It helped to explain the borderline panic that gripped the market before the rushed announcement of another rescue deal for MPS, which has already been bailed out twice, on the same day that the EBA results were made public.

The extra pressure applied to the situation by the ECB has not gone down well in Italy’s banking community.

“We have a problem,” states Giovanni Sabatini, general manager of the Italian Banking Association (ABI). “It is the legacy of the most severe and prolonged crisis after the Second World War in Italy. But we still are able to manage the problems with our own resources. The pressure from the supervisors to see the NPL problem solved in the shortest time possible makes the solution more difficult in the present market conditions.”

Sabatini believes the focus on dealing with NPLs is prejudicing Italian banks compared with their counterparts elsewhere. “It is a bit irrational. There are other sources of systemic risk in the European banking sector not being addressed with the same vigour,” he claims.

“The level of derivatives and level 3 assets is a problem that historically has been a major source of systemic crisis, but this is not being addressed in the same way. An NPL is a credit. You know the debtor is probably insolvent, but there is collateral so you can estimate the value. Where you have exotic instruments where the value is based on an internal model and you have to dispose of it quickly the value is probably zero.”

The standout culprit in this regard is Deutsche Bank, which held derivative risk exposure amounting to €55 trillion on its books in April 2016.

At the end of June, the IMF identified the German bank as the most important net contributor to global systemic risk, followed by HSBC and Credit Suisse. “In particular, Germany, France, the UK and the US have the highest degree of outward spill overs as measured by the average percentage of capital loss of other banking systems due to banking-sector shock in the source country,” it said.

It is perhaps easy to understand why Italian banks feel so beleaguered.

Italy’s prime minister Matteo Renzi has been quick to take up this theme. Speaking at a news conference on July 6 he said: “If this non-performing loan problem is worth one, the question of derivatives at other banks, at big banks, is worth 100. This is the ratio: one to 100,” he claimed.

However, sympathy in the market can be hard to come by. “Italy is a big problem,” says Ruparel. “The Italian banking system is bloated, inefficient and tied up in local politics. It must be reformed.”

Another London-based banker reckons that any comparison to problems elsewhere will not help Italy’s case. “It is wishful thinking to believe that the situation at Deutsche Bank will in any way impact the thinking on Italy’s banks,” says the banker. “People may not like derivatives but they are assets. Deutsche Bank is deeply uninvestable but its situation is not as bad as that at the Italian banks.”

There is also broad support for the ECB’s tough stance with MPS. “The ECB is looking at this quite dispassionately. It is not making the problem worse – it is taking reasonable steps,” says Etay Katz, a partner at law firm Allen & Overy. “Sometimes firesales are the only solution to give some prospect of health. The ECB is not being hasty.”

JPMorgan and Mediobanca put together a two-stage private-sector solution for MPS to counter the Siena-based lender’s long-anticipated terrible stress test performance. Firstly, the €9.2 billion-worth of bad loans that the ECB has demanded the bank dispose of will be moved off balance sheet into a separate special purpose vehicle. The SPV will then securitize the loans by issuing around €6 billion senior notes, covered by the GACS programme, a €1.6 billion mezzanine tranche to be taken by rescue fund Atlante and a €1.6 billion junior tranche.

MPS is derecognizing the bad loans at 27c, but as Eoin Mullany, analyst at Berenberg Bank in London, points out, the cost of the guarantee on the €6 billion senior notes means that their actual value will be less than this. “Given the sizeable execution risk involved in this deal and the negative read-across to the other Italian banks, we do not see this as a watershed moment for Italian banks and we would be selling them into any strength,” he warns. Mullany calculates that the MPS deal implies that Italian banks need to take additional provisions against their bad loans of a further €45 billion.

After MPS’s NPLs have been moved off balance sheet, the bank will launch a capital increase to be underwritten by JPMorgan and Mediobanca, together with Goldman Sachs, Santander, Citi, Credit Suisse, Deutsche Bank and Bank of America Merrill Lynch, who have signed pre-underwriting agreements. That deal, which will be extremely dilutive, is expected before the end of the year.

Renzi has a big personal stake in the MPS rescue, hailing as he does from Tuscany. He was mayor of Florence from 2009 until he was elected prime minister in 2014, and his family chose to remain in that city rather than move to Rome on his election.

“For Renzi, it is more important to save MPS than to win the referendum,” says one banker, referring to Italy’s constitutional referendum scheduled for later this year.

“One thing that Renzi fully understood is that he didn’t want to have people standing in front of a bank like they did with Northern Rock,” says Michael Immordino, partner at White & Case in London. “The last time that happened in Italy was 1939; it isn’t a good precedent. Whatever he did, he did not want people to feel that their deposits were not being respected.”

Although an MPS rescue has now been scrambled, it is far from a done deal. The sheer volume of NPLs involved mean that this will be a stern test for the new GACS scheme – and the rights issue that is slated to follow the securitization.

“Depending on the discount on offer there will be appetite for the GACS guaranteed notes. The riskier pieces are being taken by Atlante, and the market has a lot of capacity,” says Immordino.

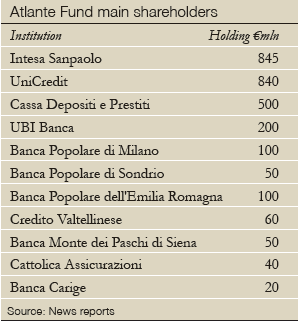

The Atlante (or Atlas) Fund was set up in April this year, partly as a solution to the failed listings of Banca Popolare di Vicenza and Veneto Banca. It is a €4.25 billion five-year, closed-end fund managed by Quaestio Capital Management, 70% of which can be invested in bank equity and 30% in NPL junior and mezzanine tranches.

Appetite for the notes will be tested by the first bank to use the GACS scheme, Banca Popolare di Bari, which announced a €140 million deal on August 12. It has moved a €480 million portfolio of bad loans into a special purpose vehicle for a price of €148.2 million, or 30.9% of gross book value. The bank has applied for a government guarantee on the €126.5 million senior notes. There is a €14 million mezzanine tranche offering 600bp and an unrated €10 million junior tranche. The transaction, which is also being arranged by JPMorgan, has been in the works since March. As Euromoney went to press none of the senior notes had yet been placed.

Price crucial

If the markets learned anything from the financial crisis of 2008 it is that securitizations are only as good as the assets that back them. So NPLs may not be the ideal collateral for a €10 billion deal. However, Katz at Allen & Overy emphasizes that the technique should simply be viewed as a mechanism to enable state support to be fed into the system, rather than as a standalone solution in itself. In Italy, the involvement of the Atlante fund at the junior and mezzanine level and the guarantee at the senior level are there to mitigate concerns over asset quality.

“This is using securitization as a mechanism to effect small, privately placed transactions to willing buyers of NPLs using the Atlante fund,” says Katz. “It is a way to effect the sale of the assets. A way for the state to facilitate a solution.”

Nevertheless, the price at which bad loans are transferred from bank balance sheets into securitization SPVs will be crucial. Pucci at PVE questions the maths behind the bumper MPS pool, which is split roughly half and half between secured and unsecured loans.

“A level of 30 cents for the NPLs in the MPS portfolio is a blended price, which means they are assuming around 10c for the unsecured loans and around 50c for the secured, which is hugely optimistic,” he points out. “At the end of December the BOI [Bank of Italy] reckoned the recovery rate was around 37c to 40c on the euro for secured. So if you look at the true recovery price after the collection fees it would be something close to 30c plus 10c. The recovery value should therefore be around 25c not 30c. Twenty cents on €27 billion is about €5.4 billion. So the true amount of money that the SPV will collect will likely be €5.4 billion not €9 billion, which means that there is €3.6 billion missing,” he claims.

This should be of particular interest to those lower down the capital stack of the deal. Taking mezzanine or junior risk in the trade will not be for the fainthearted.

“The securitization route poses a number of challenges, particularly for a very large and varied transaction, starting with the time it takes to produce reasonable quality data in a priceable format,” says Sulger at AnaCap. “And many equity investors, where the capital is most needed, will require their own extensive review and would typically want to be more involved in asset-level analysis from the outset.”

There are 67 investors in the Atlante fund, many of which are other Italian banks. A second fund has now been raised to focus on NPL purchases.

So far, appetite for the second fund among Italian investors is unclear. In late July, the country’s industry association for pension fund managers, the ADEPP, announced that it would support the second fund, but by mid-August three of its member funds had declared that it fell outside their investment parameters and they would not be participating. Even so, by August 8 the second Atlante fund was believed to have raised €1.7 billion.

Sabatini tells Euromoney that the pension funds are being short-sighted. “Long-term investors should review their investment policies to take into account the zero-rate environment and in order to be able to offer a decent return to their investors. They should also accept some more risk. In the past, when government bonds were able to offer positive returns, it was easy to have a low-risk policy. Today if you wish to offer positive returns ,you have to accept a higher level of risk.”

The pension funds’ caution is, perhaps understandable. “If you do the maths, even the mezzanine tranche of Atlante has a very high risk of not being repaid,” claims PVE’s Pucci.

Drop in the ocean

The need for capital in Italy’s banking system is such that even if the second Atlante fund is closed successfully, it will only be a drop in the ocean of what is needed to fix the system.

“As widely discussed, Atlante seems inadequate as a systemic solution including many other banks, as it looks like Atlante may use all their capital on only a few banks,” says Sulger.

The first fund has already been severely depleted by the rescue of the Banca Popolare di Vicenza and Veneto Banca listings; on July 29 it committed to the €1.6 billion mezzanine tranche of the MPS deal.

By any measure the €5 billion capital raising proposed for MPS is ambitious. Most investors and bankers that Euromoney spoke to doubt it can be done.

“It looks very unlikely that the capital raising will be possible,” says Ruparel. “How much do they want to link the fate of the better banks to the worse banks by persuading them to invest in them?”

Pucci at PVE again emphasises that the impact of incagli is being underestimated at MPS. “Whoever puts money into MPS is not putting money into a good bank,” he says. “There are still €27 billion incagli loans so the €5 billion rights issue will have to be used to absorb more losses.”

Mullany at Berenberg calculates that the cost of increasing coverage on MPS’s remaining NPLs to 40% from 28% will be €2.2 billion; increasing the coverage on the sofferenze still held by the bank from 63% to 67% will cost €1 billion and that the deconsolidation of bad loans and equity spin off will require a further charge of €1.6 billion. So that takes care of €5 billion quite easily.

The JPMorgan plan was not, however, the only one on the table for the stricken lender. Andrea Orcel, president of the investment bank at UBS, also put together a rescue deal for MPS that would have incorporated a change of management and potentially some form of bondholder bail-in, necessitating a smaller capital raise.

Orcel, together with former Italian industry minister and ex-CEO of Intesa Sanpaolo, Corrado Passera, wrote to the bank on the eve of the stress test results on July 28, proposing an alternative rescue. While this plan also envisaged the bumper GACS-guaranteed NPL securitization, it is understood to have proposed a smaller capital raise of around €3 billion, together with the debt-to-equity conversion, or voluntary bail-in, of some subordinated bonds. It is understood that the plan envisaged the voluntary bail-in of institutional investors ahead of retail buyers. The MPS board rejected the proposal.

While the last-minute UBS intervention injected yet further drama into a situation that had little need of it, the deal stood little chance against the JPMorgan scheme that was already on the table. The latter had the firm backing of the state lender Cassa Depositi e Prestiti (CDP) and was ready to go.

The UBS plan is also understood to have involved the ousting of Fabrizio Viola, MPS’s chief executive, with Passera taking over as his replacement. At the time this was thought to have weighed against it as Viola was highly regarded for doing a good job in very difficult circumstances, but on September 8 the board of the bank announced that he had agreed to step aside. News had emerged in late August that Viola and former MPS chairman, Alessandro Profumo, were under judicial investigation for false accounting and market manipulation associated with two derivatives trades and it seems that pressure for new management from JPMorgan and the other banks underwriting the capital raise pushed the board to act. As Euromoney goes to press no replacement has been announced, although Marco Morelli, ex-deputy general manager at MPS and currently head of BAML in Italy is believed to be frontrunner.

Few in the market expect the JP Morgan restructuring deal to be the last for MPS, and this only highlights the extent to which Italy desperately needs to find a way to get public funds into its banks.

“This is a hugely political topic because banks go to the core of sovereign powers,” says Katz. “They have a pivotal role in the economy and there are very intricate financial stability issues around the failure of an institution.”

Nevertheless he points out: “The BRRD has been an extraordinary success in European terms. All the signs are that it has been implemented and understood well within the policy intent. It has strengthened the discussion on the part of the investor community to better understand what bank failure looks like. There has been enormous progress since 2008.”

However, the core tenet of BRRD is that any form of state aid or resolution fund cannot be tapped until up to 8% of a bank’s total liabilities have been bailed in. The imposition of this regulation to a banking system such as Italy’s was always going to be extremely problematic; the condition of MPS has simply brought the situation to a head.

According to the IMF, the 8% capital requirement under BRRD would wipe out subordinated bondholders in most of Italy’s largest 15 Italian banks; for around two-thirds of them, senior bondholders would be hit as well.

Acharya, Pierret and Steffen have concluded that: “Even after including subordinated debt in a possible bail-in, banks in Germany, France and Italy still show shortfalls as a multiple of market equity and subordinated debt of above 1, implying that public backstops may have to be involved to achieve desired capital adequacy unless losses are passed on to non-subordinated debt holders.”

Tim Skeet, chairman of the bail-in committee at the International Capital Market Association, argues that legacy NPLs in Italy and elsewhere render bail-in rules on outstanding bonds inherently unfair. “Icma sent a position paper to the ECB in July last year pointing out that there are €1 trillion NPLs on weaker bank balance sheets across Europe and investors cannot be expected to bear this legacy loss,” he says.

“The dial needs to be reset to zero. It is not right to expect investors to carry the can for legacy problems.” The legacy problems in Italy are of such magnitude that if this case is to be heard anywhere, it is there.

“They didn’t really anticipate the complexity of this on a regional basis,” says Skeet. “There is a patchwork quilt of legal frameworks to work with. Full implementation of BRRD has been unrealistic from day one, but realism on this has now dawned.”

Ruparel at Open Europe says that the various applications of bail-in across Europe have only served to underscore how difficult it is to apply a single rule in very different situations. “There has been a huge variety in how banking crises have been dealt with across Europe so far,” he says. “If you look at Greece, Austria, Portugal and now Italy it is looking very patchy already and this further undermines it. You need to deal with problems before you go down the one-size-fits-all approach. With bail-in now in place it will be very hard to sort this out.”

Stripped bare

With hindsight it seems inevitable that Italy would be the jurisdiction in which the inconsistencies of BRRD’s bail in-regulation would be stripped bare. Not only does it have a dysfunctional banking system weighed down by bad debts, but it also has one-third of all bank bonds in the hands of retail investors for whom bail-in would be politically toxic. This is thanks in part to preferential tax treatment for bonds versus deposits between 1996 and 2011 (12.5% versus 27%).

“The resolution regime works quite well in situations with just one distressed bank in a healthy environment,” says Andreas Wieland, partner at White & Case. “In an environment where the whole banking sector is under stress, or to clean up legacy situations, it is a problem.” Italy is a poster child for both.

“This is where BRRD breaks down,” says Katz. “It isn’t going to provide the solution to an emergency situation for multiple institutions in a single country or across Europe. You are not going to get beautifully coordinated resolution in this sort of situation.”

What you are probably going to get is a monumental fudge in order to somehow get state funds into the system – simply because the prospect of anything else is too awful to contemplate.

The question is how this fudge is best achieved.

“Recent events have shown that the EC puts a high standard on BRRD,” says Wieland. “They didn’t buckle. They want to defend this and limit any intervention to particular situations. There are ways to support the recapitalization of banks under the resolution regime, but it only applies to viable banks. This is the dilemma – getting a private-sector solution is paramount.”