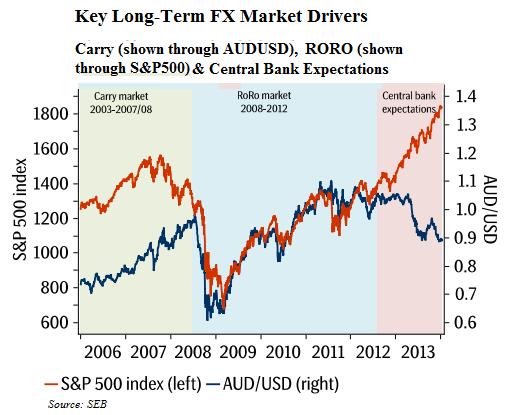

From around 2003 to the onset of the global financial crisis in 2007/08, the carry trade was the key driver for many in the FX market until the dramatically rising volatilities across the currency world made the funding side of the two-part trade hazardous.

At that point, risk-on-risk-off (RORO) strategies were the preferred weapon of choice for most dealers up to the middle of 2012, when developments at the US Federal Reserve, European Central Bank (ECB) and Bank of Japan (BoJ), in particular, served to refocus traders’ attention back on expectations for the monetary policies of the world’s central banks.

Now, though, with the Fed having begun to taper its quantitative-easing programme whilst the BoJ remains inexorably on the course of a 2% inflation target and a 3% nominal GDP rate – there has been no nominal GDP rise for 15 years – and a growing view the ECB might be about to embark on its own bond-buying programme, divergence in interest rates might herald the return of the carry trade as a dominant FX strategy, say analysts, although not necessarily before the next couple of years.

“Provided major central banks continue to ease monetary policy, they will probably also stop smaller central banks from taking steps to tighten monetary policy, as this would mostly subject their own currencies to further pressure to appreciate,” says Richard Falkenhäll, currency strategist for SEB, in Stockholm.

Consequently, he adds, the trigger for the next currency regime will most likely concern Fed monetary policy with a complete cessation of asset purchases and signalling of higher rates, which would also make it possible for smaller central banks to move ahead with tightening monetary policy as well.

“As the current regime is likely to continue until the Fed, or another large central bank, announces a more hawkish monetary policy, this will also cause rate differentials between currencies to widen, with several central banks probably remaining on hold for longer – such as the BoJ and the ECB,” says Falkenhäll.

“So, increasing rate differentials will improve the return on carry exposures eventually, just as they did 10 years ago.”

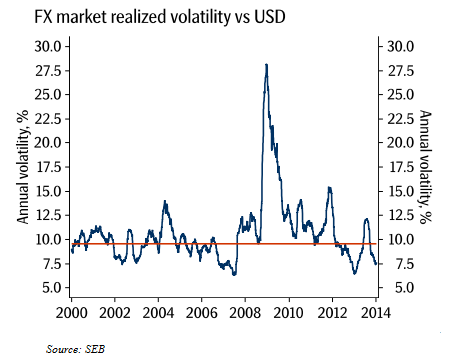

Having said this, for a prevalent carry trading paradigm to re-establish itself, FX volatilities need to be low enough to avoid wiping out the interest rate gain with currency losses, and in this respect there is some divergence in interpreting the headline volatility numbers.

In this respect, although FX volatilities have fallen substantially in recent years – on the surface to around pre-financial crisis levels (see chart below) – their trajectory is far from certain, given a range of metrics.

|

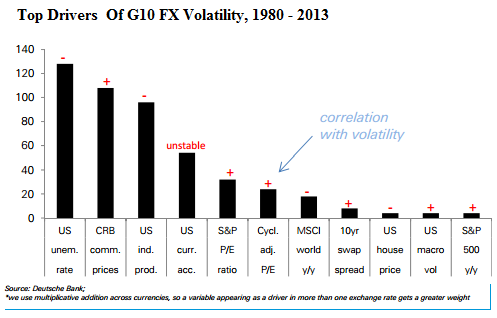

To begin with, says George Saravelos, currency strategist for Deutsche Bank, in London, only a limited number of variables do a good job of explaining realized volatility across most exchange rates, including the US unemployment rate, US industrial production, changes in commodity prices and equity valuations.

“Better growth or higher commodity prices lower volatility, but higher stock-market valuations are associated with higher volatility, and we also find that better current accounts in the US and Europe lower realized volatility, but the signal is unstable across other currencies,” he says.

These results make perfect sense, given that weaker growth is in general associated with higher policy uncertainty and investor deleveraging, which in turn should lead to higher volatility.

“This is in line with the ‘up the escalator, down the elevator’ characteristic of FX carry trades, in that carry crosses rally in a low-vol trend as confidence improves, but the unwind is sharper and more disorderly when confidence deteriorates,” adds Saravelos.

Nonetheless, says Ian Stannard, head of European FX strategy for Morgan Stanley, in London, there are signs that, overall, as growth is returning to the US, Japan and even China – 7.7% year-on-year GDP growth in Q4, whilst marginally lower than Q3’s rate, is still significant – so confidence in the market grows that rates will have to rise within the next two years or so, widening yield differentials.

This pattern is likely to be even more pronounced and to occur at a quicker pace if, as Deutsche Bank predicts, China’s growth surprises markedly to the upside this year and next, by 8.6% for 2014 and 8.2% for 2015.

“China’s export growth has followed growth in the US and EU economies very closely since 2008 and as those economies recovered in the second half of last year, so did Chinese exports,” says Michael Spencer, head of the bank’s Asia Pacific research, in Hong Kong.

“In fact, we estimate export growth has averaged 20% quarter-on-quarter Saar over the past six months, and sustained growth in the US and EU will take export growth in year-on-year terms much higher than we think most investors expect.”

In such circumstances, then, it would be reasonable to assume that some of the perennial standbys of the previous main carry trade era should come back into play.

In purely FX terms, the Swiss franc even now is still regarded as a safe haven of choice for many, despite the imposition of a floor in the EURCHF rate of 1.20 francs per euro, further boosted in its role as a funding currency by Swiss National Bank president Thomas Jordan’s reiterations that the SNB will maintain the band for its benchmark interest rate at 0% to 0.25%.

Perhaps the archetypal funding currency of all, the yen, is also likely to come back to the fore of the carry trading world, despite recent concerns over the impact of the increase in the consumption tax scheduled for April.

“With the US tapering under way, US yields should stabilize at a new higher level over coming weeks, giving investors greater certainty about the yield carry they will get in the US over Japan,” says Mark Astley, G10 currency strategist for Credit Suisse, in London.

“And, whereas long yields in other major countries have moved higher with the US, the unprecedented BoJ purchases along the yield curve have so far kept Japanese yields remarkably stable, with the 10-year still only yielding 0.70%.”

|

|

|