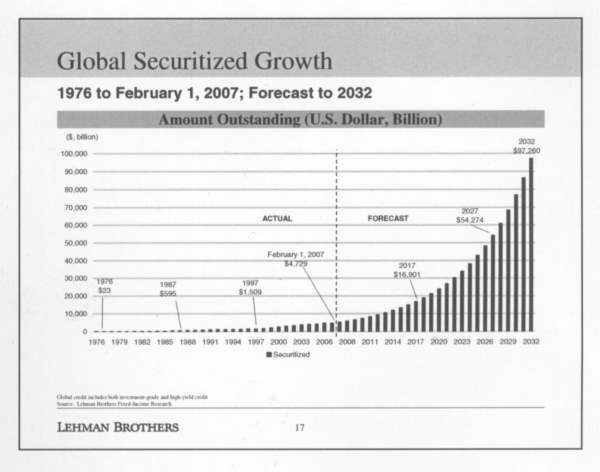

On page 17 the bank produced a chart confidently predicting the uninterrupted growth of global securitization from February 1 2007 to 2032. There was to be a smooth and steady increase in issuance from $4.7 trillion in 2007 to $16.9 trillion by 2017, $54.2 trillion by 2027 and an eye-popping $97.2 trillion by 2032.

|

In reality, net global securitization issuance slumped by 79% in 2008 and has struggled to regain its pre-2007 momentum ever since.

Lehman certainly knew that trouble was coming, and listed possible catalysts for “the crash of 2009” (it was only one year out on that one). It asked: “When is the next bank run?” (Answer: just seven months later with Northern Rock). Top of its list of triggers for a hypothetical run was a devastating terrorism event or maybe an energy price hyper-spike.

In actuality it was the complete evaporation of wholesale bank funding that did it. Lehman did call the risk of a massive housing correction (ranked number three), but what really killed the market – the drying up of excess liquidity – only came in at number six, behind a far-more-likely eruption in inflation.

On page 42 the bank laid out its recommendations for 2007: heavy exposure to ABS, overweight CMBS, minor overweight MBS. It predicted a modest outperformance of MBS in 2007 but did state that it was cautious on the effects of the US housing downturn on gross origination and liquidity.

Most alarmingly, however, it declared that Hybrid ARMs (the sub-prime US mortgages that triggered the global financial crisis of the last five years) would outperform fixed rate MBS.

You have to feel for Lehman’s clients. Its investment recommendations for ABS made for even scarier reading given what happened next: go for pure subordination, they said. Buy leveraged super senior tranches, buy market structures that benefit from market volatility such as ABX CPDOs and bespoke CDO squareds of managed single-A ABS CDOs and the triple- and double-B tranches of ABS CDOs. Ouch.

It is easy to be wise after the event; hindsight is a wonderful thing. But the now-defunct US bank is really testing our sympathy towards the end of the report: “Rating agency reactions – signal or symptom?” it asked. Stating that rating agencies spot problems early but take action gradually the bank then declared: “In ABS, superior surveillance infrastructure make rating agencies better placed to spot underperformers early.” Errr…discuss?