It’s our turn to add to the Fischer-for-Fed chorus, following news the Israeli central bank governor is stepping down on June 30.

Other than Mark Carney, Bank of Canada governor and Bank of England governor-designate, there are few central bankers whose reputations have grown in the crisis era, with the market consensus decreeing Fischer has been consistently ahead of the monetary curve since he was appointed in 2005.

|

| Fischer. Source: Reuters |

Although Fischer’s mandate has recently been diluted, the Bank of Israel is unique since monetary policy decisions are made by the governor alone, which means Fischer deserves any credit or blame for the monetary stance since 2005. The former IMF deputy managing director’s astute policy moves, pre- and post-Lehman, has boosted his status as a hugely respected economic soothsayer, whose pronouncements are observed globally – transcending the influence of the $240 billion+ Israeli economy.

Firstly, Fischer – Euromoney’s Central Bank Governor of the Year in 2010 – helped to shield Israel from the storms emanating from the US syndicated loan crisis between July 2007 and March 2008, stepping up acquisitions of foreign currency reserves and embarking on quantitative easing through the purchases of long-term debt.

Secondly, when Lehman collapsed, Fischer insulated the economy from the global storm by weakening the currency, ensuring the export sector was not demolished by an uncompetitive shekel.

Thirdly, on October 6, 2008 Fischer cut Israel’s benchmark rate – one day before monetary policymakers in the US, UK and eurozone coordinated their interest rate cuts. Fischer then cut the rate to a record low of 0.5% by April 2009 and embarked on an aggressive bout of quantitative easing.

Lastly, in January 2012, Fischer cut rates – again anticipating monetary loosening globally – as he rightly judged growth fears would outweigh inflation concerns.

Monetary philosophy

Aside from BoI’s ahead-of-the-curve monetary stance, Fischer’s long-standing academic and real-world pronouncements on the power of communication to buttress market confidence echoes Carney and the Fed’s recent embrace of forward-rate guidance.

In addition, Fischer’s tenure at the BoI and academic research on the flexibility of an inflation-targeting regime – taking into account supply-side shocks – have fed speculation that he has implemented nominal GDP targeting in Israel, a stance that swims with the emerging transatlantic monetary tide. (Indeed, Fischer, like Carney in his capacity as Bank of England governor-designate, has also broken new ground by becoming an Israeli citizen in order to lead the BoI, underscoring the global free-market in monetary policy labour.)

More generally, as an Israeli policymaker – an economy that straddles the fine line between developed and emerging status – he understands the impact of Fed policy on foreign capital volatility and exchange rates, providing a rare global dimension to Fed policy. (A perspective that would no doubt be viewed more favourably in Sao Paulo and Beijing than in Washington.)

His tenure would obviously intensify the debate over the legitimacy of activist central banks at a time of so-called global currency wars, while possibly signaling the US’s willingness to engage with the question of the role of international monetary cooperation to address global imbalances.

In sum, Fisher’s intellectual pedigree, on-the-money policy moves and failed IMF leadership bid – laying bare his pent-up global ambitions – mean Fischer deserves to be in the running, alongside Federal Reserve vice-chairman Janet Yellen.

|

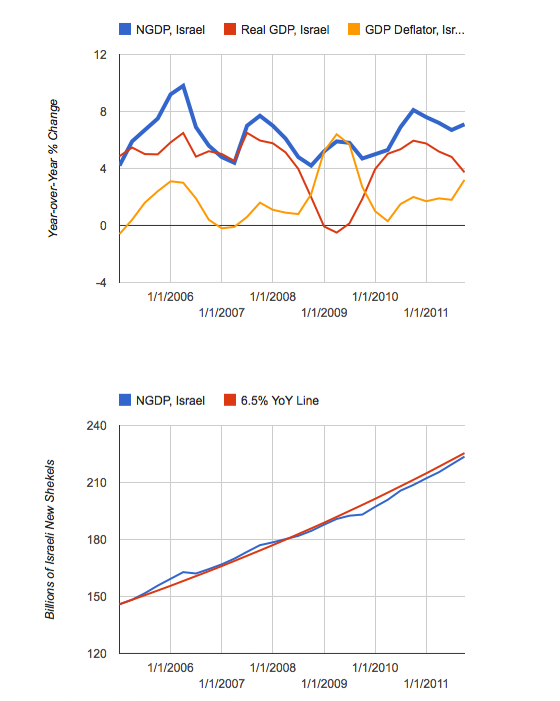

| Source: Evan Soltas blog |