This week provides much ammunition for the monetary orthodoxy that fear global markets are dangerously on Fed life-support in an era of central bank-backed capitalism.

On Wednesday, Fed chief Ben Bernanke was at pains to stress the Fed will keep rates at historic lows for an extended period but said improving US economic data mean the Fed will trim its $85 billion monthly bond purchases by the end of the year.

This relatively modest – and far from unexpected – statement was enough to roil global markets.

“Markets are selling off because the US is improving,” said a glib Emad Mostaque, strategist at Noah Capital Markets.

The US dollar strengthened on the back of expectations of earlier-than-expected tightening of monetary conditions. The Indian rupee, Turkish lira and Pakistani rupee fell to an all-time low, the Polish zloty tumbled to one-year lows while other high-beta currencies, such as the rand, also received a bloody nose. The bearish bulls have stopped capitulating. In fact, Thursday was as bad as the dark days of the October 2008 crisis with a historic 9 standard deviation move across 5-year swaps in Mexico, Hungary, Poland, Turkey, and South Africa, which are the largest local FX markets, aside from Brazil, outside Asia, according to ITC Markets, a data provider.

EM FX has been the biggest loser, followed by local rates, credit markets and finally equities, with the latter seen as relatively cheap before the most recent Fed-driven sell-off.

In other words, emerging market (EM) investors received a rude awakening on Thursday morning: the era of extraordinary monetary accommodation in the US is slowly coming to an end, with profound consequences for real rates in EMs, local credit and foreign exchange markets.

How EMs deal with this latest stress test could influence asset allocation strategies for years to come. In the words of Société Générale: “The moves in global emerging markets have already been severe, but there is considerably more pain to come.”

The stakes are high – in part, because of the road portfolio investors have travelled during the past five years.

From spring 2009, as central banks sought to ward off deflation with unprecedented liquidity injections, foreign investors have loaded up on EM stocks, currencies and credit in tandem with the liquidity-fuelled global risk rally.

The justification for this portfolio shift was the oft-touted rationale: stronger growth prospects, attractive returns relative to financial repression in the west and strengthening credit metrics.

The risks that clouded the EM outlook were ostensibly Janus-faced. On the one hand, liquidity from G7 central banks ostensibly threatened to destabilize domestic financial markets and trigger export-damaging currency appreciation in the currency wars.

On the other hand, markets also feared a disorderly wave of capital outflows in the event of a global economic shock and the prospect of tighter G7 monetary policy.

While a synchronized and disorderly sell-off in EMs have unnerved investors in recent years, central banks have mercifully hitherto come to the rescue.

For example, as the eurozone sovereign debt crisis intensified in the second half of 2011, banks withdrew funding in international markets, and global deleveraging gathered pace. Local currency bonds sank into the red.

Inflation-targeting central banks, principally in Latin America, had to cut interest rates given weakening domestic demand. In a volte-face, the Brazilian real and renminbi weakened and capital controls were loosened. However, the European Central Bank’s (ECB) provision of eurozone banking liquidity in December 2011 and resolute promise to shore up the euro stemmed the free fall.

While valuations looked stretched in EM hard currency bonds, EM bulls argued further flows in that asset class, equities and credit, more generally, were on the cards, citing stronger economic fundamentals and growing strategic inflows from real-money investors.

After all, according to fund-tracker EPFR, net inflows to hard currency and local currency EM funds since the second quarter of 2009 to-date have been sizeable but not obviously unsustainable at $58.4 billion and $84.4 billion, respectively.

This time it’s different

However, as the fateful refrain goes, this time it might be different. Speaking to Euromoney’s Emerging Markets last year, Carmen Reinhart, senior fellow at the Peterson Institute for International Economics, summed up the market stampede into EM recent years:

“I’ve seen this movie before. An extended period of stable, low interest rates in advanced economies has been coupled with a terms-of-trade boom for commodity exporters in Latin America. Cycles, by definition, go up and down, and yet this cycle, by and large, has continued from the spring of 2009.

“And therein lies the danger: markets might come to the same conclusion that this time it’s different and treat the inflow of capital as a permanent feature of the brave new world.”

Could the warning by Reinhart – co-author with economist Kenneth Rogoff of the ground-breaking study of global boom and bust cycles This Time is Different – hold true? Could rising US real rates, on the back of an ostensibly improving US economic prospects, trigger a disorderly adjustment in emerging capital markets, or even a sudden stop?

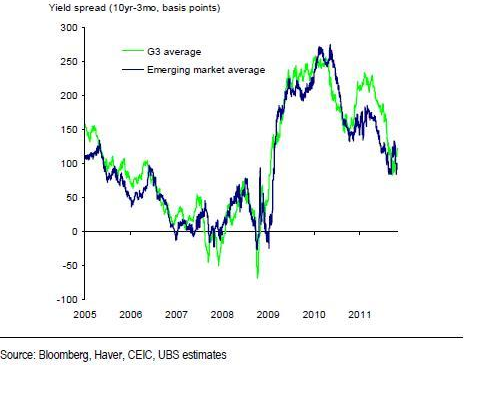

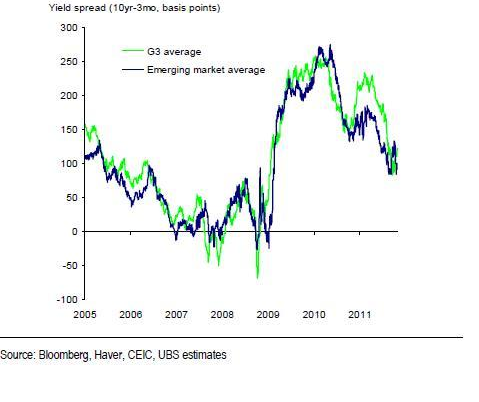

After all, as these charts lay bare, EM yields are synchronized with the aggregate G3 interest rate, if the past seven years are anything to go by, as growth and inflation trends correlate amid rising globalization.

In short, rising US yields mean monetary conditions will tighten in EMs, argue analysts.

Morgan Stanley reckons real interest rate hikes in EM are inevitable due to endogenous factors – weaker current-account support and fewer pools of savings – and exogenous shocks: weaker capital flows from the US and a stronger dollar.

As Euromoney has noted, rising US Treasury yields will challenge returns from hard currency EM debt while a stronger dollar will eat into returns from local currency bonds.

However, the macroeconomic fallout could be severe. Morgan Stanley says: “The effect [from rising US yields] has been to raise real rates in EM, dampen the ability to generate credit growth and create downside risks to growth, inflation and asset prices, thus mimicking the classic effects of a tightening of EM monetary policy.”

While the ability of central banks, from South America to southeast Asia, to loosen interest rates in the post-Lehman era heralded their newfound ability to shape domestic credit conditions, the old-school image of an EM central bank – one that is forced to pro-cyclically hike to defend currencies – predominates.

Indonesia and India are being pushed into a tighter monetary policy than is desired, citing currency weakness, while the speed of currency sell-offs and the rising of front-end rates indicate the prospect of rate hikes from Mexico, Turkey, Hungary and South Africa, among others, notes Morgan Stanley.

This is far from inevitable but the broader risk is clear: EM central banks have less policy flexibility than assumed.

Already, growth expectations in the Bric economies have unexpectedly taken a knock during the past year, injecting fears that the structural economic prospects of the world’s growth engine are weaker than expected.

Russia’s economic outlook for 2013 was recently revised downwards from 3.4% to 2.5% by the IMF. Brazil’s IMF forecast remains unchanged from its April projection of 3% but a recent Barclay’s report is more bearish, projecting growth in 2013 of 2.3%.

India is expected to grow 5.7% this year compared with the 8% to 9% of its heyday, while the World Bank revised its forecast of Chinese growth in 2012 downwards from a December 2012 projection of 8.4% to 7.7% in June.

The prospect of capital volatility at a time of deteriorating growth, tighter monetary conditions and higher leverage in the Bric economies should serve as a wake-up call for investors and EM policymakers.

However, even that scenario paints a benign picture – one that bets Fed’s monetary adventure will be unwound in a gradual and stable fashion, and in a way that is well communicated to markets.

Sudden stop

If a miscalculated monetary gamble from the G3 roils markets for an extended period, could there be a sudden stop in portfolio flows to EMs – and who is vulnerable?

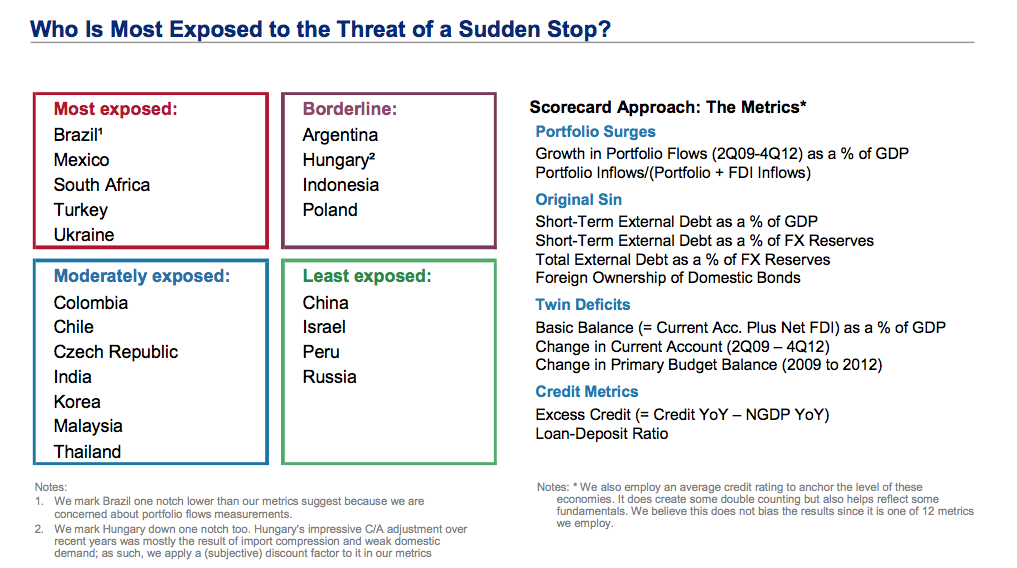

Morgan Stanley analysts have identified those EM economies that are, in theory, most exposed. The framework takes into account economies that have experienced a surge in portfolio flows in gross, rather than net, terms, where domestic credit growth has outpaced nominal GDP growth, as well as current-account and fiscal deficits.

The following chart makes for sobering reading:

In other words, irrespective of a country’s growth outlook or the strength of its policy arsenal to combat a market storm with foreign-exchange reserves, Brazil, Mexico and Turkey are included in the most exposed list.

The Latin American CEO of a large eurozone bank on Thursday summed up market sentiment in comments to Euromoney: “I have just had a meeting with [Alexandre] Tombini [Brazilian central bank governor]. He is worried about derivatives and corporate leverage.”

Indeed, with Brazilian corporates adding $100 billion of external debt since 2008, protest-ridden Brazil is exposed to substantial macro volatility, according to this model, even though it is a net creditor to the tune of $370 billion of foreign-exchange reserves.

In other words, a tightening of US monetary conditions raises the spectre of a sudden stop of capital flows to EMs, which could cause substantial volatility in the larger markets, though a balance-of-payments or fiscal crisis akin to the 90s is unlikely.

Morgan Stanley analysts make a sobering conclusion: “The latest episode of weakness in EM should serve as a ‘wake-up call’ for EM policymakers. Not only do they have to improve their external balance sheets, but they also need to introduce structural reforms and bring back the productive dynamic.

“Any less, and the ride could be quite bumpy for EM.”

Even if the Fed’s exit is well handled, the macroeconomic impact for EM could be profound – because of rising real rates in EM – and not because recent expansions in the ECB’s and the Fed’s balance sheets have been used to finance trades in EMs directly.