A string of higher fixings in USDCNY in the first half of this month, weaker-than-expected Chinese economic data and recent comments from a People’s Bank of China (PBoC) official that the currency is reaching fair value have raised concerns that the renminbi-appreciation story might be coming to an end.

The changing perception that USDCNY is seemingly no longer a one-way bet has become evident in the forwards market. The USDCNY one-year non-deliverable forward (NDF) has gone from pricing in 1% appreciation at the start of the year, to now pricing in depreciation of about 0.2%.

Despite lower fixes in the past few days – including a record low on March 23 – visual inspection of the USDCNY daily fix does suggest that the appreciation trend that began in late 2010 might have broken down.

| USDCNY reference rate has strayed outside 18 month range |

|

| Source: ANZ |

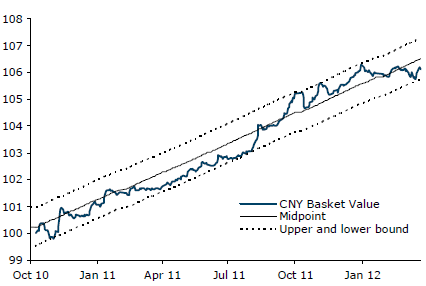

However, Khoon Goh, senior FX strategist at ANZ bank, cautions against calling an end to the renminbi-appreciation trend by just looking at USDCNY, given that the renminbi is managed against a reference basket comprising currencies of all its main trading partners. The PBoC does not publicize the composition of its reference basket but estimating the CNY reference basket – comprising USD, EUR, AUD, JPY and KRW – ANZ finds that the CNY has been appreciating at an annualized rate of 4.4% since October 2010 and stayed well within the central bank’s estimated policy band, despite higher USDCNY fixings.

The lower USDCNY fixing in recent days has resulted in the reference basket recovering towards the midpoint.

| ANZ CNY reference basket has traded within a narrow band |

|

| Source: ANZ |

Renminbi volatility set to rise When Chinese premier Wen Jiabao recently announced a lower-than-expected GDP growth target of 7.5%, concerns of a slowing Chinese economy added to the bearish sentiment for the renminbi.

However, ANZ considers Chinese slowdown fears to be overblown and has not altered its above-consensus GDP growth prediction of 9% in 2012.

The Australian bank says despite a lower official growth target, political incentives at the local government level to achieve strong growth remain in place.

US growth momentum and receding fears surrounding the eurozone debt crisis have also added to stronger external demand conditions, and rising imports of processing materials in February could also indicate a rebound in exports in the next quarter.

While ANZ’s stronger-than-consensus growth outlook reinforces its view that renminbi appreciation has further to go, the bank is not alone in predicting rising volatility in the currency.

“We could be undergoing a regime change whereby the PBoC not only controls the pace of appreciation but also allows for increased exchange rate volatility,” says Goh.

That’s probably because the PBoC wants to prepare Chinese firms, financial institutions and residents to better cope with exchange-rate swings ahead of expected further capital-account liberalization.

David Pavitt, head of EM FX trading at HSBC, considers the PBoC’s emphasis is now on internationalization rather than appreciation, and the wider movements in daily fixing point to greater volatility in both the NDF and the offshore spot market (CNH).

“It seems that [the PBoC] is looking to get the renminbi to trade much more like every other currency does, and it wants the market to get used to that,” says Pavitt. “I wouldn’t be surprised if we see a widening of the intraday trading band.”

“If the market gets used to the way spot USDCNH is trading at the moment – and it is doing so pretty quickly – USDCNH spot could soon trade with similar levels of volatility as EURUSD.”

In the options market, USDCNH 1 year at-the-money implied volatility fell more than 25% in February from close to 4.5 to just above 3.00, as rising corporate supply far outweighed speculative demand for volatility. USDCNY options displayed a similar pattern and derivatives traders who spoke with EuromoneyFXNews earlier this month said implied volatility was likely to find a base at those levels.

Implied volatility in both the NDF and offshore CNH have recovered modestly in March; though remain well below the levels witnessed at the height of the appreciation trade in the autumn of 2011. For investors with a longer term view, the current levels of China vols offer an attractive buying opportunity for those expecting a rise in volatility.

| USDCNH vols still close to 5 year lows |

|

| Source: Bloomberg |