|

|

IN ADDITION |

|

There is an uncomfortable acceptance in Philippine business right now. People will tell you, conspiratorially, that they did not vote for firebrand president Rodrigo Duterte; that his extrajudicial killings of suspected drug dealers are abhorrent; that insulting former US president Barack Obama was unnecessary and counterproductive and that his strong-man image jars on the world stage. But here’s the thing: bank share prices are up, profits are growing and customers are happy. For all the political noise, business is good for banks in the Philippines.

“Fundamentally, there seems to be a generally positive outlook for business,” says Fabian Dee, president of Metrobank. “A lot of us are quite bullish.”

Metrobank has good reason to be. In February, it reported full-year consolidated net income for 2016 of P18.1 billion ($520 million), with fourth-quarter earnings up 3% year on year and record levels of total assets, deposits and total loans. Revenues for the year were up 16% on 2015.

Metrobank is not alone. At BDO Unibank, the biggest bank in the Philippines, net income for 2016, at P26.1 billion, was up 4.3% year on year and total resources (a term used locally for assets) by 14.5%; non-interest income shot up by 30.3% in a year. Bank of the Philippine Islands saw full-year net income climb 20.9% from 2015 to P22.05 billion, with every important metric up and non-performing loans down. And at Land Bank of the Philippines, 2016 brought double-digit growth in both assets and deposits, with net income up 2% for the year at P13.6 billion.

|

|

|

Alfonso Salcedo Jr, Security Bank |

“We are seeing momentum across all segments, from retail to wholesale,” says Alfonso Salcedo Jr, president and chief executive officer of Security Bank. The bank is a mid-tier success story whose growth and model attracted the attention of Japan’s Bank of Tokyo-Mitsubishi UFJ, which invested P36.9 billion in April 2016. Its 2016 full-year net income after tax, at P8.55 billion, was up 11% year on year.

Why are banks excelling when political risk in the Philippines, in terms of volatility and headline shocks, has not been greater in a generation?

Part of it is structural. “Our national growth is being driven by the demographic dividend,” says Salcedo. “The median age is 23.”

Metrobank’s Dee believes it also comes down to a renewed sense of public safety.

“What the general business community sees in Duterte is that he has a track record,” says Dee. “He’s quite frank in saying: ‘I am not an expert about the economy, but I will create an environment where it is safe so business can grow for itself.’”

There is a sense from ordinary people in Manila that crime has come down. One Manila taxi driver proudly tells Euromoney that nobody has tried to stab him in almost a year.

“You don’t have people standing by the sari-sari stalls [convenience stores] harassing you on your way home,” says one banker. “And that has encouraged a lot of people, that maybe things are safer, so their plans for expansion have come in. The trajectory of our loan portfolio is improving as we speak.”

It helps that ‘Sonny’ Dominguez, the finance minister, has largely been left to his own devices to guide the economy and that soon-to-retire central bank president Amando Tetangco is one of the region’s best and has been able to maintain his independence.

Dominguez has focused on improving tax collection and has been open about his eight-point economic plan that he distributed before even taking office. It includes a commitment to infrastructure spending, education, land registration and the removal of the 40% ownership cap for foreign companies.

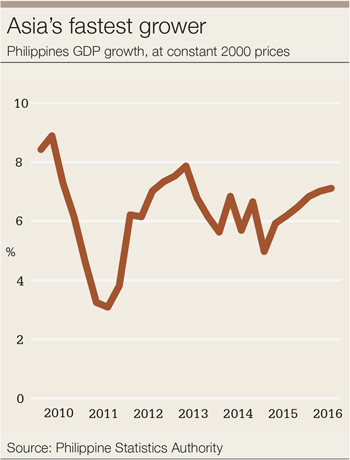

Dominguez is stewarding an economy that grew at 6.8% in 2016, among the best growth rates in the region, although it is hard to credit that entirely to a new government only nine months into its administration. The economy has also been helped by relatively benign weather, leading to a strong harvest and good productivity in the agricultural sector, which in turn has meant more purchasing power for farmers and others in the provinces. That has flowed through to retailers and from there to construction and logistics.

|

|

|

Fabian Dee, Metrobank |

“The emergence of business expansion in the countryside has created growth for local employment,” says Dee. “We are seeing less migration coming from the provinces and get the sense that people are taking advantage of opportunities that are closer to home.”

In an unheard-of turnaround, construction companies in Davao and other provinces are beginning to import people from Manila, after decades of human movement in the other direction.

But it is not all good. The biggest complaint in the Philippines is much the same as it has been for at least the past two decades: the infrastructure bottleneck.

The Benigno Aquino government appeared to have a handle on this, philosophically at least, setting up the Public-Private Partnership Centre in Manila in 2010 as a central coordinating and monitoring agency to facilitate PPP projects across the country.

“The previous administration focused on ensuring that governance and transparency were in place,” says Jette Gamboa, head of the strategic planning division at Metrobank. “Unfortunately it took longer than anticipated to lay down the foundation for good governance in the bidding, evaluation and awarding process. In some cases it took longer to get the necessary approvals because of the additional steps that had to be taken.”

One banker puts it bluntly: “There has been very little infrastructure development in the last five years. The last government talked about it, but eventually it became a joke.”

The problem is that the new government, which came in on a platform of doing things differently, has not yet delivered. “The major negative rap on the previous administration was that it moved too slowly on infrastructure,” says Salcedo at Security Bank. “Duterte came in as a strong man who would get things moving, who would not worry about politics. But that has not happened, unfortunately. It has been almost nine months and I’m not aware of any major infrastructure project that is happening or is about to happen.”

A year and a half

During Euromoney’s visit to Manila, the local press said that the first awarding of a PPP under the Duterte administration would now be next January. “Next year! It’s March! So that will be one and a half years of the administration before the first PPP is awarded,” says Salcedo.

One change of approach to the PPP model was to move from the bundling of several projects together for a single bid under the Aquino administration to doing them individually under Duterte. The positive view is that it is easier to get those projects moving; the negative, that some of them are projects that nobody in their right mind would bid for, unless they were required to do so in order to win a more appetizing mandate along the way.

This is not, it is felt, a good time to be slow. Manila is abuzz with the promise of Chinese and Japanese money and a key element of Duterte policy has been to turn his back on the US – which he did under Obama, but which might prove to be a shrewd move, given a more US-insular Trump administration – and to court China instead.

There is a lot at stake here. “Over P300 billion in infrastructure projects comprise the six-year development programme of the Philippine-China economic cooperation pact to be offered to a visiting China senior official,” said Citi analyst Jun Trinidad on March 14 (the official he referred to being Chinese vice-premier Wang Yang). Two key railway projects will be the heart of it, but as many as 15 infrastructure projects are believed to be on the table.

But this takes the form of official development assistance (ODA), rather than the PPP model, and Trinidad wonders what this pivot in policy means for the future of infrastructure development. “We believe the ODA pivot signals the de-prioritization, but not abandonment, of PPP,” he says.

His impression is that Chinese development assistance feels a lot simpler to the government than private-sector negotiation. ODA is long-term funding, eases pressure on corporate balance sheets that would be strained by PPPs and moves faster, albeit with far less scrutiny.

“Despite the PPPs’ funding transparency, implementation delays can be encountered post-government bidding and awarding, as past experience shows,” says Trinidad. And the PPP process, he says, is “complicated by the need to tweak the design of the proposed infrastructure project to ensure the commercial aspect would be financially appealing to private bidders,” whereas Chinese development assistance is less prickly to commercial sensitivities because of the political benefits that accrue along the way.

The problem is that setting aside PPP funding in favour of development assistance has long-term implications for public finances. “The government may have to absorb the long-term debt needed to acquire the infrastructure project over the medium term,” says Trinidad. “We see the trade off in having sizeable prospective ODA debt is that it lifts the government debt ratio, raises the vulnerability of public finances” to a weaker currency and higher interest rates and “elevates the urgency to have a good tax reform package approved in Congress.”

The frustration in banking circles is that there should still be plenty of opportunity to channel Chinese and Japanese money into PPP structures if the right projects can just be hurried up and readied. After all, it appears Chinese ODA money is almost entirely to be allocated to the North-South Railway project that will connect Manila to the Bicol region of Luzon and a 2,000-kilometre railway project on the southern island of Mindanao (where Duterte comes from).

“The Chinese have the money, the Japanese have the money, but there are no project feasibilities,” says Salcedo. He believes that the issue is capacity for implementation; that many people have left the PPP Centre with the change of government and that replacing people with the right technical expertise to move things forward has been difficult. “The pivot idea was fine. The Chinese are ready – and I understand they are really ready – with their money. But it’s the absorption capacity.

Low sixes

“Even if we were to have infrastructure paralysis, we are still talking about growth in the low sixes,” says Salcedo. “But if you really want to make a dent on poverty levels you need to grow in the sevens to eights for a decade. And that will not happen if we don’t implement major infrastructure projects.”

Dee argues that even if implementation is slow, there is a greater willingness on the part of the new government to spend. “They are not afraid to run into deficit, which is a catalyst for economic growth,” he says.

That, in his view, is a trade worth making. “Everyone who comes through this airport says the same: ‘Imagine the possibilities if we fixed the roads, if we could get food to market faster.’ This country is 70% driven by household consumption.” Improved infrastructure, particularly outside Manila, would have a positive effect all over the economy, he says.

“As a commercial bank,” says Dee, “that is very good for us as most of our clients are in the middle market: SMEs, contractors, sub-contractors, distributors. It all leads to more purchasing power. There are so many ways we can benefit.” Around 55% of Metrobank’s distribution network is in the countryside, he says.

At Bangko Sentral ng Pilipinas, the Philippines central bank, governor Amando Tetangco thinks the PPP Centre gets a bad rap. Reading from a list, he claims that four completed projects are operational through PPPs, seven under construction, seven under procurement, and a further five approved, with 22 under various stage of assessment. “That’s the pipeline,” he says. “It has started to take off. It took a little time, but there are a lot of big companies that are looking to the infrastructure space and participating in its development.”

Tetangco claims that from January to November there was an increase of 46% year on year of government spending on infrastructure and other capital outlays, and that this in turn followed a 22.8% increase the previous year.

|

|

From Tetangco’s perspective, he is leaving a financial system in good shape when he retires in July. “During the fourth quarter of last year we clocked the 72nd consecutive quarter of uninterrupted GDP growth,” he says. “That means we have been growing since the first quarter of 1999.” At the same time inflation has been falling, from 6.1% in 2005 to 1.8% in 2016 – although it was 3% in February this year.

One of the most impressive numbers is foreign direct investment, up 40% in 2016, exceeding projections not only for that year but for the next one as well. “And most of that is going to manufacturing and logistics, or utilities like power, so I think it’s really laying down the basis for sustained growth in the medium term,” says Tetangco.

Portfolio flows have been volatile ever since Donald Trump took office and the Federal Reserve began to hike interest rates, but they have tended to vary from inflow to outflow from one month to another, rather than a steady departure.

“Looking at flows, both in the equities and the fixed income markets here, I would say that the portfolio investments that would have gone out anyway have already gone,” he says. “The investments that have stayed will mostly likely stay. They have a longer-term view.”

As always, remittances from overseas are an essential crutch to the economy and grew 5% last year, ahead of projections. Even business process outsourcing, the sector that was expected to be hit by a Trump presidency, grew by about 13% last year and is on track to continue to grow this year.

Financial inclusion is meant to be a government priority and banks are trying to find ways to reach further into the population. “You really have to penetrate the lower levels of the economy,” says Dee. “Financial institutions like us are willing to do our part, but sometimes there are structural and operational challenges in extending credit to that level.”

Rural banks and the informal sector do so, but some are trying to provide alternatives. “A major part of financial inclusion is making credit available to areas where access has only previously been informal,” says Security Bank’s Salcedo.

Security Bank has a platform it is expanding into this segment, “which will be able to reach out to that sector at rates that will make it worth our while, knowing the NPLs and the delinquencies that will come from that. It’s higher risk for us, but it will be lower rates than they are paying to the informal sectors.”

Security Bank has had the product for three years and is comfortable with delinquencies, but now plans to expand it “on a more meaningful scale.” The bank is also rolling out a small business portfolio, although at a cost; Salcedo says it needs to be at least 200 basis points over home loans to be workable.

“ The Philippine cycle on small and medium-sized enterprise lending is that you make money on nine out of 10 years, but once a decade you lose what you made in the other nine years,” he says. “You’ve got to be disciplined in pricing through the cycle so you are able to withstand it when you get hit.”

|

Farewell, Tetangco! So good they tried to change the law for him

Amando Tetangco took on the top job as the nation’s central banker in July 2005 under president Gloria Macapagal Arroyo. In the intervening period, he has lasted the full term of Arroyo and her successor, Benigno Aquino, and the first year of the latest incumbent.

He has seen the global financial crisis come and go and yet has shepherded the Philippine economy through a period of unbroken quarterly growth that has lasted the whole of his tenure. And when he leaves in July, he will still be popular.

“It would be impossible,” says Security Bank president and CEO, Alfonso Salcedo Jr, “to admire him any more than I do. He is a top-notch person.”

Tetangco is as unflappable as ever as he takes a seat at a boardroom table to reflect on the economy whose stewardship he is ready to hand over.

What’s the secret of stability? “The first important element in this equation is focus,” he says. “One has got to be focused on the mandate of the institution, which in our case is the maintenance of price and financial stability, conducive to the balanced and stable growth of the economy. Everything you do should be consistent with that mandate.”

He also raises the importance of independence. Bangko Sentral ng Pilipinas (BSP) gained its separation from the government in 1993, its charter enshrined in law and, despite some grumbling about it by Duterte from time to time, nobody perceives a threat to its independence today. “Independence and credibility are two sides of the same coin,” Tetangco says. “Independence promotes credibility; credibility fosters independence. And that’s important.”

Other key considerations have been a well-articulated policy framework. For BSP on the monetary side, this means principally targeting inflation and on the banking side, adhering to global financial reforms – keeping pace with things like Basel III, while also ensuring there is sufficient supervision to stay on top of compliance. “Things are changing very fast,” he says. “So one needs to be able to detect emerging trends and see how they will impact the domestic economy and financial system.”

Over the last decade, he has watched his peers in developed markets create all sorts of monetary policy tools, but emerging Asia (having done its tough restructuring after the Asian financial crisis) has not needed to resort to them. In fact, despite both the current political noise and the geopolitical contortions during his tenure, the Philippines looks remarkably stable: low inflation, climbing payroll, a doubling of import cover, a halving of external debt to GDP and a banking system whose non-performing loan ratio among the universal commercial banks has fallen from 8.2% to 1.4% (around Singapore’s level).

Asked about the greatest challenge he has faced, he is clear that it was the global financial crisis. Not just the sky-rocketing credit spreads during the eye of the storm, but the subsequent search for yield and the consequent capital flows into the Philippines.

“So that complicated monetary policy, because suddenly you’ve got this significant amount of liquidity that is not internally generated but has come from offshore. Our economy isn’t large enough to absorb that kind of liquidity, and you have to deal with it.” Doing so had an impact on exchange rates, interest rates, credit and domestic liquidity.

“The conventional response of raising interest rates to deal with too much liquidity didn’t work anymore. When you raise interest rates, you just get more liquidity,” he says.

If Tetangco has a reputation of reasonable calm, his country’s new president does not. There is an extraordinary amount of political noise affecting the economy..

Asked about this, Tetangco smiles. “The first thing is to question in order to clarify what has been said. You have to focus on the actions, not on the words. The advice for foreign investors is to see through the noise and look at the macroeconomic fundamentals, which remain strong.”

Duterte is clearly an admirer of Tetangco, however. Upon learning that Tetangco was coming to the end of his second term, the legal limit, he offered to change the law in order to accommodate a third term. Tetangco will not be drawn on this, but Euromoney understands he was indeed approached, but indicated that two terms was enough.

“I think,” says one senior banker in Manila, “He would have been mad to take it. Crazy. If he did, it would have been to serve the country. But he has already done that for 12 years.”

Consequently the industry is somewhat fearful about what comes next. Most hope that the successor comes from within, probably Diwa Guinigundo, a deputy governor on the monetary stability side, or Nestor Espenilla, another deputy governor but more involved with bank supervision.

As for Tetangco, he’s off. “I’ve always said, the first thing that I’ll do on my first day of retirement is to wake up late and look forward to an unstructured day,” he says.

He will travel, spend more time with the family, play golf and all the classic answers that come with retirement: “But I think I will continue to be a watcher of economic developments, particularly on the financial sector side. Being in the central bank for 43 years, that’s going to be very difficult to shrug off.”

After a break, he is thinking of doing something in an NGO, “particularly in the financial inclusion space,” he says. And he has no fears for the health of his institution. “BSP is ready for a leadership change. Twelve years is long enough.”