More than 2,000 institutions participated in the 2026 Euromoney Financial Institutions Survey, including 574 non-bank financial institutions (NBFIs) that completed the payments and/or liquidity management pathways.

The survey was conducted between 26 January and 5 April 2026 and asked respondents to share their priorities, outlook, primary cash management providers, and assessments of those providers across product capabilities, technology, and client service. The results informed the ranking of 30 banking providers globally, across four regions and six Asia-Pacific markets.

The distribution / use / publication of MarketMaps or rankings requires the express permission of Euromoney – please contact Arun Ghudial for additional information. For any queries on methodology, data packages or bespoke benchmarking reports – please contact Ana Voicila.

Additional results from other streams of this survey will be published in the upcoming weeks.

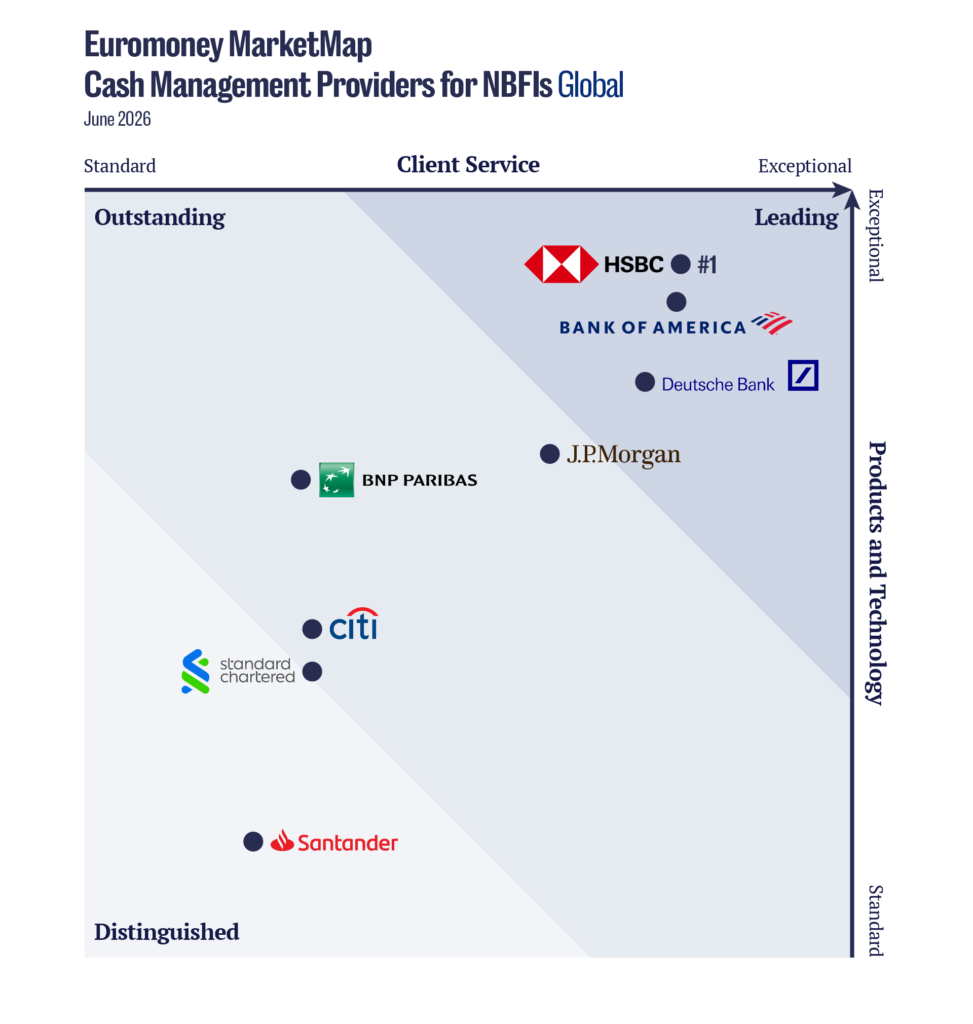

Top ranked cash management providers for non-banking financial institutions

The global rankings highlight a group of providers that combine strong relationship management with increasingly sophisticated digital capabilities.

HSBC leads the market through its integrated coverage model, global connectivity and highly responsive client service. Bank of America stands out for its service culture and continued innovation through CashPro, while Deutsche Bank is recognised for its transaction banking expertise, advisory approach and cross-border capabilities. J.P. Morgan continues to differentiate through technology leadership and investment in next-generation infrastructure, including blockchain-enabled payments. BNP Paribas is recognised for its institutional client coverage and execution strength, while Citi’s integrated Services model combines cash management, payments and securities services into a unified proposition. Standard Chartered earns recognition for its network across Asia, the Middle East and emerging markets, while Santander’s strength lies in deep local expertise and regional connectivity.

Across the market, success increasingly depends on combining trusted relationships with digital innovation, real-time connectivity and treasury automation.

Asia remains one of the most dynamic and competitive markets for institutional cash management, driven by growing cross-border investment flows, regulatory complexity and increasingly sophisticated treasury requirements. The rankings highlight a diverse provider landscape where global connectivity, local market expertise and digital innovation all play critical roles.

HSBC emerges as the leading provider, recognised for its integrated coverage model, cross-border capabilities and strong client service. DBS stands out for its API infrastructure, digital innovation and responsiveness, while Deutsche Bank is praised for its automation capabilities and operational efficiency. Citi continues to leverage its extensive international network and ability to deliver consistent service across multiple jurisdictions. Standard Chartered is recognised for its relationship strength, competitive pricing and deep presence across emerging Asian markets.

Across the region, institutional clients increasingly favour providers that combine strong relationship management with digital capabilities, automation and seamless support for complex cross-border treasury operations.

Domestic rankings

Europe remains one of the most sophisticated markets for institutional cash management, shaped by deep capital markets, extensive cross-border activity and evolving regulatory requirements. Treasury teams are increasingly focused on liquidity visibility, operational resilience and technology as they prepare for structural changes such as the transition to T+1 settlement. The leading providers are those that combine network strength, digital innovation and specialist institutional expertise.

Bank of America ranks #1 among European NBFIs, recognised for its relationship management, digital capabilities and connectivity to the Americas. HSBC is praised for its client-centric approach, responsiveness and API capabilities, while Deutsche Bank stands out for its advisory-led model, transaction banking expertise and ability to support complex treasury structures. J.P. Morgan benefits from its integrated institutional franchise and technology investments, while Citi is recognised for payments, liquidity solutions and international capabilities. Barclays completes the leading group, valued for its UK market expertise, client service and ongoing investment in payment automation.

The Middle East has emerged as one of the fastest-growing markets for institutional cash management, driven by expanding capital markets, rising cross-border investment activity and the growing influence of sovereign wealth funds, asset managers and private capital firms. As institutional treasury requirements become more sophisticated, providers are increasingly valued for their ability to combine global connectivity with strong regional expertise.

HSBC leads the rankings, recognised for its proactive client engagement, international network and digital capabilities, including API connectivity and automated liquidity solutions. J.P. Morgan is valued for its ability to connect operations seamlessly across major financial centres through a consistent global platform. Standard Chartered stands out for its cross-border capabilities and connectivity between the Gulf, Asia and Africa. Emirates NBD and FAB demonstrate the continued importance of domestic market expertise and strong regional relationships, while Citi is recognised for its global network, digital infrastructure and leadership in payments innovation.

North America is one of the largest and most influential market for institutional cash management, supported by the world’s deepest capital markets and highest concentration of institutional investors. In this environment, clients place a premium on reliability, execution quality, digital innovation and operational resilience.

Bank of America leads the rankings, recognised for its strong client service, proactive engagement and continued innovation through the CashPro platform. HSBC is valued for its highly personalised service model, digital capabilities and thought leadership, while Deutsche Bank stands out for its relationship-driven approach, competitive pricing and expertise in supporting international treasury requirements. J.P. Morgan continues to differentiate through its technology leadership and digital platform design. Standard Chartered is recognised for its dedicated relationship teams and ability to connect North American clients to growth markets across Asia, the Middle East and Africa. Citi rounds out the leading providers, praised for its global reach, digital banking capabilities and increasingly integrated approach across treasury, payments and custody services.

This is the second year when the Financial Institutions Survey is running separately from other piece of client satisfaction research. The study covers both non-bank financial institutions (NBFIs) and banks, across three key cash management areas: payments, liquidity and trade finance.

Given that in 2025 the study was ran as a study and both the methodology and question went through significant changes, no year-on-year comparison is added in the rankings. 2025 results can be accessed here.

For the NBFI segment, participants included a diverse mix of respondents from:

- Asset managers

- Broker-dealers

- Insurers

- Payment service providers

- Pension funds

- Wealth managers

These respondents shared detailed insights into their priorities, selection criteria and experience with providers. Each participant identified their top five providers and rated them on product offering, technology, and client service using a 1–10 scale (10 being highest). Responses are weighted by institution size to reflect market relevance.

To qualify for a regional ranking, a provider must be rated by clients in at least two countries within that region. For the global ranking, providers need to have been assessed across at least two regions.

Results are visualised in the Euromoney MarketMap, which categorises providers into three tiers:

- Leading, excelling across both service and solutions

- Outstanding, strong in one key area or for a specific client segment

- Distinguished, noted for quality across service or offering

Currently all Euromoney surveys are qualitative in nature, capturing client experience and satisfaction, rather than market share or transaction volumes.

This approach allows us to spotlight the providers that are truly delivering for financial institutions today – and shaping the future of institutional transaction banking activities.

Top ranked cash management providers for NBFIs

How does the ideal NBFI banking partner look like? One that combines strong relationships, modern technology, global reach, domestic market expertise and a broad product set. For providers, the challenge is not excelling in a single area, but delivering consistently across all of them.