|

IN ADDITION |

|

Santander’s bet on Latin America goes back a long way.

“When we started investing in Latin America, between 20 and 25 years ago, it was with the idea that the region would [at some point] have superior structural growth to Europe,” says José Antonio Alvarez, chief executive of Santander Group, after welcoming Euromoney to the bank’s sprawling campus-style HQ on the outskirts of Madrid.

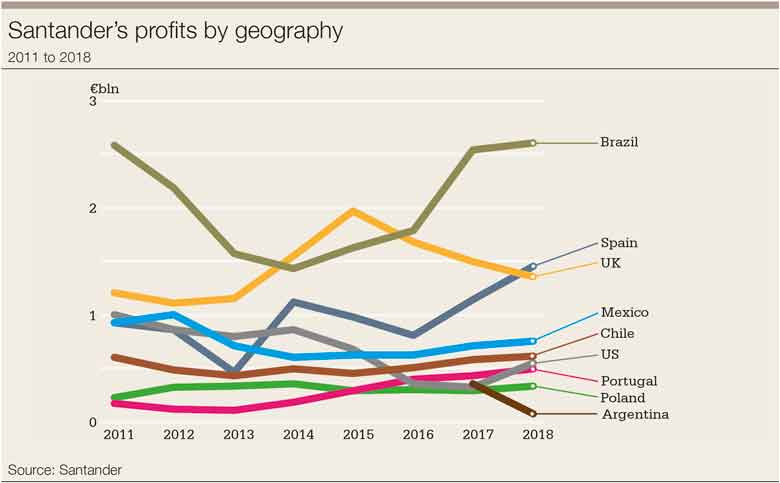

That time has come – and how. In the last four years Latin America has surged from contributing 35% of total underlying attributable profit in 2015 to 41% in 2018 – and that figure will likely continue to climb.

And it’s not just a relative outperformance caused by weakness elsewhere. Total attributable profits grew to €4.06 billion from €2.72 billion during this time – and that growth came despite sharp falls in Latin America’s currencies. Imagine what will happen if the bank continues to grow and these currencies hold their own – or even appreciate.

“We expect to grow faster – much faster – with double-digit growth in local currency in Latin America,” says Alvarez. “In Europe we can grow 2% to 3%. And more than that means winning market share, which is difficult to get.”

In late January, Santander Group revealed a strong performance for 2019, in which Latin America again more than offset weakness in Europe: profits in Brazil were up 4% year on year, while in Mexico, profits were up by 42%.

Latin America is all about structural growth for Alvarez. He points to the fact that across the region, between 40% and 60% of people are typically still without current accounts; and he says that digitalization is accelerating financial inclusion as banks can serve lower income sectors at a lower cost.

In Europe, he adds, the leverage of the countries’ financial systems is anywhere between 130% and 200% of GDP, whereas in Latin America it can be as low as 30% and as high as between 60% and 70%.

José Antonio Alvarez, chief executive of Santander Group

“I don’t know exactly when, or at what pace, but it makes sense that the gap in the GDP [between the regions] will close over time – this was our expectation when we invested in Latin America,” he says, pointing out that while “about 70% of our balance sheet is in mature markets, and only about 20% is in Latin America, our profits are already almost 50/50”.

And Alvarez doesn’t believe Latin America will only be the engine of growth over the short-to-medium term. He draws similarities with the maturation of the banking system in Spain, when it shifted from a banking system characterized by low volumes, high spreads and high cost of risk.

“The evolution to higher volumes, lower spreads and a lower cost of risk is normally the sweet spot for banks. It’s the journey [that is most profitable]. When the market becomes mature, it’s all about efficiency; when you are emerging, it’s all about risk. When you are in the middle, it’s the sweet spot.”

How long will that journey take?

“My experience in Spain was 25 years,” Alvarez says. “It was a great journey, and we took advantage of our home market’s structural growth to generate plenty of excess capital – we went from fifth-largest bank in Spain to one of the largest in the world. We took this excess capital and invested in Latin America. Now it is Latin America’s turn to drive [Santander’s] growth.”

And it is not just revenue growth. The whole bank is relying on the region’s already strong profitability to drag the group towards its stated medium-term return on equity target of between 14% and 15%, from 2018’s 12.1%.

Last April, Alvarez told attendees of the bank’s London investor meeting that the biggest single factor that will take the bank to this target will be a “reweight to Latin America” – more than its plans to boost US profitability or for efficiencies in Europe or capital efficiencies.

Santander’s Latin America business already generates 19% ROE – compared with 11% from its home market of Spain, 9% for the UK, 12% for Portugal, 13% for Poland and just 8% from the US. Alvarez believes the region’s medium-term sustainable ROE is between 20% and 22%. But is that realistic?

Brazil performance

Santander’s recent growth in Latin America has mostly been a Brazilian story. Brazil contributed nearly double the amount to the group as Mexico, Chile and Argentina combined (€2.61 billion against €1.46 billion) and alone contributed 26% of group profits.

However, until recently and like all the non-domestic retail banks in the country, Santander had struggled to make its investment perform. Some competitors, such as HSBC and Citi, simply gave up and quit.

Santander, always larger than those banks in Brazil but also a long way from the country’s top two private-sector banks, Itaú and Bradesco, stayed. But it didn’t thrive, becoming the second bank for many Brazilians because it lacked the ability to cross-sell to existing clients and the physical presence to build new customers.

But then the market began to come to Santander. First with the withdrawal of those international competitors, then with the scaling back of the public-sector banks and finally through the unleashing of digitalization that has enabled Santander to build large numbers of new customers without a corresponding ramping up of its physical infrastructure.

As well as growing retail customers in the country – the foundation of the bank’s business plan – it also began to convert its clients into primary customers. And then into loyal customers (the definition of this was supplied by Hector Grisi, chief executive of Santander Mexico: customers who keep an account balance, have bought between two and four products, and have carried out between three and 10 transactions in 90 days).

Between 2016 and 2019, the number of loyal customers grew by 42.6% (from 3.67 million to 5.23 million), according to the bank. External data corroborates that shift in Brazil.

I tell my bankers every single day: ‘Bancomer can receive money just by opening the door. We can’t do that. We need to go out every single day with a knife in our mouth and get what we can.’ – Hector Grisi, Santander Mexico

A 2019 report from UBS found that Santander Brasil’s Net Promoter Score (NPS) – a key metric used by analysts to show banks’ competitive brand positioning – had improved the most in the preceding year. The bank’s NPS improved by 23.6% (although it still lags its private-sector competition).

Perhaps more importantly, however – given the bank’s focus on digital banking – is that its customers (among those of the established banks) reported that they are the least likely in the country to switch accounts – a probability of 2.43 out of five just beats Itaú at 2.46, as well as Bradesco and Banco do Brasil, at 2.55 and 2.57 respectively.

The bank’s improvement in fortunes in Brazil is often described as starting in 2016 with the appointment of Sergio Rial as country chief executive, but the improved momentum can be traced back as far as 2014 when it conducted a tender offer for its Brazilian-listed subsidiary, believing it had put in place a growth strategy that would outperform the market.

In April 2014, Santander offered to buy back the 25% of the bank’s shares listed on the Bovespa (now B3) for R$15.31 ($3.74) – a 20% premium. That was accepted by investors who owned 54.6% of shares, taking the bank’s holding of its Brazilian operation to 88.3%.

The same year, the bank also made the strategically important acquisition of payments company Getnet – a product it has aggressively and successfully used to get both small and medium-sized enterprise and consumer bank accounts.

The bank’s view on its growth from 2014 was shrewd. From about R$12.50 a share when the tender offer was made, the share price has risen steadily and on December 2, 2019 closed at R$44.48, very nearly a 250% increase.

As Alvarez outlined in that London investor day, in the three years between 2015 and 2018, Santander Brasil increased its ROE from 14% to 20%, grew the number of its digital clients 2.6 times and the number of loyal customers by 65%.

It increased its share of the loan market by 110 basis points and improved its efficiency ratio by six percentage points. Investors and analysts now know the story, but Alvarez gives another perspective of its recent outperformance – that of historical underperformance.

“There’s another angle, and that is that after we bought the bank in 2007, [referring to the acquisition of Banco Real from ABN Amro – although the bank has had a presence in the country since 1982 and a large one since its acquisition of Banco Banespa in 2000], the integration took a lot longer than we were expecting,” he says. “By the time we had finished the full integration in 2012/13, we had lost market share, with the state banks being very active at the time.”

Santander’s senior management certainly believed in its ability to retake market share and grow the business following this belated integration. And it backed itself spectacularly with the 2014 tender offer. Now the bank has just completed another tender offer in the region, this time offering shareholders in Santander Mexico a 14% premium. That offer closed in the third quarter of 2019 and took its ownership to more than 90%.

What are the parallels?

“Our rationale is that our view of our subsidiary is much better than the market’s,” says Alvarez. “We did the same in Brazil. In Mexico, [we also] saw that we were able to put a premium over the existing share price, and [then] it’s up to the minority shareholders. In Brazil, it worked extremely well – obviously you need a big discrepancy and the same was happening in Mexico. I am not sure why in Mexico the market was valuing us at between seven times and eight times [our price-to-earnings ratio].”

Mexico’s turn

Last August, Santander appointed Grisi, previously chief executive of Credit Suisse Mexico, to lead the bank in that country.

As in Brazil, the bank underperformed in the years following its IPO (Mexico’s was in 2012, Brazil’s 2009). Will Mexico’s post-tender performance be reminiscent of Brazil’s share price performance since 2014?

One minority shareholder who spoke to Euromoney (and who didn’t accept the tender offer) says he thinks the ground has been prepared for a similar, if not necessarily as spectacular, share-price performance. For one thing, the bank’s $735 million-equivalent three-year investment plans ended in 2019, suggesting the efficiency and profitability ratios could spike north in 2020 and the coming years.

Grisi isn’t going to commit to tripling the Mexican bank’s share price in the next three years, but you get a sense that he also wouldn’t be surprised if it did so.

His demeanour – friendly, with rapid-fire delivery and a procession of clear target-orientated points – belies his investment banking background. Nevertheless, Grisi is clearly at home in retail, or rather universal, banking – Santander’s corporate and investment banking businesses in the region are an important competitive differentiator.

|

|

|

Hector Grisi, Santander |

“This is a bank that comes from the merger of four different banks: two were investment banks and highly concentrated on ultra-high net-worth individuals and large corporates; one state bank [Banco Mexicano]; and a merchant bank [Banco Serfin],” says Grisi. “So I ended up in an interesting combination: this is one of the most powerful franchises for corporates, but a very bad franchise for individuals.

“It was very unbalanced. If you compare [Banco Santander Mexico] to Bancomer, Banorte or Banamex then my mix of credit and deposits is very different to them. When I came in, my analysis was that I needed to grow in individual clients – and we have concentrated on that since I joined four years ago.”

That target is being achieved. Since 2015 the Mexican bank has increased its digital client base by 3.3 times, while the loyal customer bracket, which Grisi says is five-times more profitable than those that aren’t in this classification, grew 81% to 2.6 million in 2018. In the last year the bank has added 800,000 new clients.

The growth in individual accounts has also helped the bank’s funding costs. By ceding the individual deposits sector to competitors, it had given those banks an inherently lower cost of funding.

Grisi is working on reversing this.

“Bancomer funds 40% of itself through individual clients’ [deposits],” he says. “When I joined, 24% of our funds came through individual clients without remuneration – and now it’s up to 32%, but I am still eight percentage points below.”

In the third quarter of 2019, the bank increased individual deposits by 8.9%.

There is clearly still lots more to do to match the market leaders.

“I need three million more clients,” says Grisi. “Right now I have nine million active individuals, and I need to get to 12.5 million just to be in the same playground as Banorte and Bancomer.”

There is nuance below these big-picture numbers. Grisi doesn’t see all retail as equally valuable.

“I was an investment banker for a long time and I tend to see this as portfolio management,” he says. “We grow the portfolio that has the best return on RWA [risk-weighted assets] and ROE, and we tend to be very cautious in the portfolios that have higher delinquency and not-so-high ROE.”

At the beginning of 2017, Grisi decided to focus on payroll loans in the consumer portfolio; in the third quarter 2019 results these continued to grow, now up nine percentage points over the almost three years to 62.3% of the total consumer portfolio, while unsecured loans have fallen in weight.

The bank’s focus on mortgages is also consistent with its prioritization of secured lending. It has launched a new product, Hipoteca Plus, which enables borrowers to get lower rates by transferring other accounts to the bank that is now responsible for 73% of all new mortgages.

Santander also consistently leads in reducing its base interest rates. Its latest move was its November decision to go to 7.99%, the lowest in the market.

In total, Santander Mexico’s mortgage portfolio grew by 7.4% year on year in the third quarter of 2019, to Ps148.7 billion ($7.92 billion). The bank’s mortgage loans were affected by the run-off of acquired portfolios – excluding this effect, the mortgage portfolio would have increased 12% year on year, higher than average market growth.

While Hipoteca Plus brings in new primary banking accounts at the margin, Grisi is also using the bank’s long-standing and deep corporate relationships to get to that target of 12.5 million individual customers.

“I am going to give you the secret recipe that is not a secret,” he replies when asked how he will achieve his goal. “I am the second-largest bank for corporates, so when we have a company for whom we are the most important bank on the loan side, we say: ‘You need to reciprocate by giving me your payroll.’

“So I am getting all the payrolls from all these big companies – and that’s how I am doing [the growth in accounts] in terms of the bulk. And the same is true of SMEs. I don’t care if you only have 25 employees – if you want loans, give me the payroll.”

We are the obvious choice for multinationals for cash management and cash pooling and all these products – we have a presence in all these countries – José Antonio Alvarez, Santander Group

A lot of Brazil’s growth in individual accounts was also achieved through leveraging corporate relationships. However, in Brazil, corporates tended to auction off payroll business, so Santander used other products, notably the payroll business Getnet, to gain share.

It’s a lever that the bank also intends to use in Mexico. The bank is turning the Brazilian payments product into a global, multi-currency platform and Grisi, as head of Santander’s global merchant services business, is preparing to launch in Mexico in the first quarter of 2020 and then across the region before heading to Europe.

Santander has already been improving its performance in transaction services. The bank now has a 14% market share, up from 12% in 2015, but still below a natural weight of 16% from its share of the overall banking market. Meanwhile Banorte has 30% of the transaction services market compared with 22% of the overall market, which gives the competitor an advantage “as they get to see every single peso that goes through them,” says Grisi.

An important part of Grisi’s attempt to catch up with his two larger competitors has been the reorganization of the bank’s sales force.

“When I joined the bank, we were a completely product-orientated organization,” he says.

“It was a magnificently efficient selling army. And if the flavour of the month was mortgages, we would sell all the mortgages in the world. Then next month the flavour was insurance, and we couldn’t care less what was happening to the individual client. Our goal was to sell. We have changed completely to be a client-centric organization, where the client is the most important part of the bank. This has been a very important cultural change.”

Thus the bank transformed its corporate structure and reorganized responsibilities, including those of the top management. Strategic areas such as customer service, innovation, digital product development, middle-market and corporate banking were strengthened, and a chief of staff of the presidency role was created.

However, it would be wrong to think Grisi has tempered the bank’s sales focus on new business; if anything he has ramped up the aggression.

“It’s a continuous sales job,” he says. “I tell my bankers every single day: ‘Bancomer can receive money just by opening the door. We can’t do that. We need to go out every single day with a knife in our mouth and get what we can.’”

Grisi thinks he needs another 36 months to close the gap with his rival. This could be called ambitious, particularly as Grisi is under no illusions as to the competitive nature of Mexico’s banking sector, one he categorizes as fiercer than Brazil’s more consolidated market.

In Santander’s global report, the bank gives Mexico’s 2018 ROE as 20%, but that’s under Spanish GAAP – under Mexican accounting rules, the bank’s stated ROE in the third quarter of 2019 was 16.6%.

“My competitors are over 20%,” says Grisi. “For me, my competitors are Banorte and Bancomer. And those two guys are still way over me. Banamex are below me, but I don’t care about them.”

Grisi may not be judging Santander against those banks in his rear-view mirror, but he keeps an eye on what they are doing all the same.

“We used to have a banking system with very unified growth, but if you look at credit growth up to August 31, then everyone is all over the place,” he says. “You have HSBC growing at 22% – they are buying market share. Scotia is growing about 15% to 16%. We are growing at around 7.5% and Bancomer at 4.5%, Banamex is less than 2% and Inbursa is flat. It tells you that everyone has a completely different view on what is happening with risk.”

The poor performance of the economy is also a factor, with credit demand falling along with GDP growth. Grisi says he will need help from an improving macroeconomic environment if he is to hit his goals, but he is positive.

“I think we will see growth picking up in the fourth quarter [of 2019]. I am on the bank’s credit committee that meets every single week and so I get a sense of what is happening, and I think it is starting to pick up a little bit.”

In the cloud

Latin America’s growing profits should help the whole bank increase its ROE to the medium-term target of 13% to 15%. But it is also helping in other areas. Alvarez agrees that part of the bank’s planned increase in the ROE of the European operations will come through digital functions increasingly being developed elsewhere for global application.

“In some sense, yes,” he replies when asked if Latin America’s growing tech role will help European profitability. “In the IT world, we are going from having an IT centre per bank onto a journey of having global platforms developed in the cloud, which will eventually serve all banks.”

Alvarez says digital and cloud development will occur “where it is most efficient”. And Mexico would appear to be competitive: as well as leading the development of the globalization of the Getnet product, Grisi tells Euromoney that Mexico is developing a new global app.

Alvarez also notes that sometimes acquisitions might be the quickest and most efficient way to bring global cloud-based products online – and points to the bank’s November 2019, $450 million acquisition of SME trade and FX platform Ebury as a good example of where acquisitive growth makes sense.

This raises the prospect that banks operating in multiple jurisdictions could be able to generate cross-border economies of scale.

Previously cross-border efficiencies have been difficult to realize. But if global banks can create global digital platforms and then spread the cost of the IT development across the countries of operation, it would present a competitive cost advantage over large, single-country banks.

There are also some products that work at scale regardless of country of origin and so therefore offering capacity globally will also offer an advantage.

Alvarez says Santander’s journey to achieve such global efficiencies isn’t “a one-shot thing, it will take three to four years” to come online. Nevertheless it’s an interesting potential shift in competitive advantage to global universal banks that have in recent times been suffering with the weight of new global capital and compliance regulations that penalize global systemically important banks.

However, Alvarez is careful not to overplay the potential cost efficiencies.

“It will depend on the business,” he says. “In some, such as payments [those cross-border cost efficiencies] are 100% clear. The cost per transaction is a business of scale – the lower the transaction cost, the more competitive you are – it’s purely industrial production. How much does it cost you to produce one transaction?

“And we are working with sunk software costs – the more transactions you put in the system the lower the costs. There’s a clear advantage.”

Alvarez says products that are virtually global commodities – he cites credit cards as an example – will reap global economies: “But when you go to mortgages, for example, then it still probably goes country by country because it is a legal product.”

Meanwhile, Grisi says Mexico demonstrates both local and global approaches. It is taking the lead on some global, cloud-driven initiatives but still innovates locally. For example, it has developed an app for the Mexican market called Santander TAP, which enables users to make payments through social media accounts.

It was launched in April and has reached 200,000 clients, with an average transaction size of Ps400.

Moving to core

When will Latin America stop being Santander’s engine of growth and become its core? Is it just a matter of time?

The answer to that depends on the definition of what constitutes being a core business. But for simplicity’s sake, let’s define it as providing 50% of profits, regardless of the amount of capital deployed elsewhere. On this measure, there is still some way to go.

Santander’s executive chairman, Ana Botín, recently committed to Mexico providing 10% of group profits in the next few years. This seems practical and achievable. Assuming those two percentage points are not diluted elsewhere in the region, that would take Latin America to 43%.

Some analysts, such as UBS’s Philip Finch, have been asking if Santander Brasil’s earnings have peaked; he wrote a report with that question as a title in early 2019. Certainly its ROE looks toppish. In the third quarter of 2019, Santander Brasil reported 21.2%, which meant it remained in between the local firms Itaú (23.5%) and Bradesco (20.5%).

The bank also announced that it sees ROE remaining around the 21% level despite initiatives such as a new business called Ben that targets aggressive growth in Brazil’s R$230 billion-a-year employee benefits business.

It projects 2022 revenues for Ben of between R$8 billion and R$10 billion.

Santander Brasil also plans to win market share in the strategically important agribusiness sector. It targets a 10% share of the $355 billion revenue industry in 2022 – up from its 5.67% market share of 2019’s $306 billion revenue.

Brazil wouldn’t need to grow more profitably to increase its participation, given the lower ROEs in other Santander businesses.

“We can keep growing share in many spaces in Brazil,” says Alvarez. “For example, we are still far from Itaú and Bradesco in SMEs and we are growing nicely there. We are market leaders in the CIB [corporate and investment banking] space, and we can continue to grow market share there – we offer a unique combination being an international bank in Brazil.”

Alvarez says the bank is benefiting from strong if volatile south-south trade flows and has generated a powerful network effect by placing CIB throughout the region.

“We are the obvious choice for multinationals for cash management and cash pooling and all these products – we have a presence in all these countries,” says Alvarez.

Chile is another strong performer in the region. However, it has less obvious ability to grow its attributable contribution from 6% because of the market’s limited size and its present political and economic difficulties.

Sadly, the other big bank in the region, SantanderRio in Argentina, also faces a difficult challenge to growth; although it’s recent attributable profit (€84 million for a 1% contribution) sets the base comparison at a low level for new chief executive Sergio Lew.

Santander also has a bank in Uruguay and operations in Peru and Colombia.

But the lion’s share of organic opportunity seems to lie with Brazil and Mexico. That could be enough to take the region to above 50% in terms of attributable profit – and it is worth noting that the region has done it before. In 2011, Argentina, Brazil, Chile and Mexico combined to generate 51% of Santander’s total profits, though that peak was short-lived.

It was caused by a unique combination of a cyclical collapse in other markets (Spain, for example, fell from generating €2.9 billion in 2008 to just €929 million) and the Latin American results were boosted by the region’s sky-high currency valuations as it enjoyed the full effect of the commodity super-cycle.

This time feels very different. The region’s performance is coming from strong and sustainable business in resilient economies. If anything, the currencies are undervalued today. And the region offers internal diversification that will help with the undoubted bumps that will come along: Mexico and Brazil are both strong drivers for Santander but are otherwise largely uncorrelated. Chile is stable. Argentina and the rest remain pretty much all upside.

If Alvarez is right, Santander’s Latin America bet 25 years ago could be about to pay off for the next 25 years.

Is rock star Rial calling the tune?

Speak to competitors in Brazil and they will quickly praise chief executive Sergio Rial as the mastermind of Santander’s rise in Brazil, which has seen it break the dominance of Itaú and Bradesco.

Rial has risen too, taking on an expanded role as head of Santander throughout South America in April last year. He’s now talked about as a future leader of Santander Group.

Rial, who declined to be interviewed for this feature, seems to be revelling in his rock-star reputation. At a recent ‘Santander Brasil Day’, he zip-lined over 40,000 employees dressed as a futuristic soldier, complete with black helmet and shining red lights, to get to the stage.

Sergio Rial

Landing with a torch in his hand that had just been passed to him by Luiza Helena Trajano, chairwoman of department store company Magazine Luiza, he addressed the hall: “I am flame! Are you flame?” a reference to Santander’s logo.

At one point, Rial even shouted in reference to the bank’s competition: “Who is it that should be afraid? Them!”

Meanwhile, Rial is taking Santander’s employee engagement focus seriously.

In a recent interview with local business newspaper Valor, under the headline ‘Rial personifies the cultural change of banks’, he explained that he sees a convergence of traditional banks and fintech startups.

The article also listed other examples of Rial’s personification of the bank’s brand (with photos): dressed as Charlie Chaplin at a bank talent show and wearing a real astronaut suit (with boots weighing 5kg each, Valor was informed) at a presentation for school children.

Obviously conscious of opening himself to criticism by such flamboyant behaviour – Valor describes a range of individual reactions from “inspiring” to “embarrassing” – Rial defends such actions as “provocations” to put employees in the headspace for innovation by recreating a childlike mind-set for curiosity.

“It has nothing to do with a personal ego-trip or desire to be the centre of attention,” he assured Valor.

Bankers outside Santander have recently begun questioning his current behaviour, mixing it in with praise. The constant brand championing to an internal audience and his aloof approach to external stakeholders (Rial led just one quarterly results call for 2016, 2017 and 2018 and none in 2019) leads to suggestions that “the Sun King is drinking his own Kool-Aid”, as one rival banker puts it to Euromoney.

The success of Rial’s aping of startup culture will be an interesting one to watch: usually eccentricities are indulged in those who create their own disrupting companies – less so among career employees assuming the leadership of established brands.

Ultimately if the bank’s rapid and profitable growth continues unchecked, then it seems likely that Rial’s theatrics will too.

A play on Emotion

Banking is a notoriously dry business. But Santander Mexico is looking to bring feeling into fintech with its Emotion Lab. Euromoney visited the office – close to the Santander Mexico HQ – which is designed to provide the look and feel of a fintech startup.

The Emotion Lab tracks customer interaction with the bank across a range of products and services. The bank mines this data to find weak spots in that interaction – for example, hot spots causing application processes to be abandoned or customer-service issues.

Hector Grisi, Santander Mexico’s chief executive, says the Emotion Lab has already provided material improvements: “Previously, we were closing 19 out of every 100 mortgage applications that were started – so you can imagine the customer acquisition cost of only closing 19%. Now we are up to 29%.”

Grisi says that Santander Brasil is going to copy the Emotion Lab to improve its customer service; this plays to an important point about Santander’s global strategy that often gets missed because it is hard to make explicitly through financial analysis.

In 2016, the bank introduced a radical new global remuneration policy at all levels in the bank. Now 60% of variable remuneration is evaluated against traditional financial metrics and targets, and 40% through results of engagement and employee feedback surveys that evaluate a range of corporate behaviours. Even 40% of group chief executive José Antonio Alvarez’s variable remuneration comes from collegiate scoring (across 60 questions).

Engagement metrics

In Latin America, this has been used to reinforce employee engagement metrics and the bank has focused its employee efforts towards being ranked as a “great place to work”. The improvements have helped recruitment and retention.

“Every time we open a job position, I want to have 100 CVs of people trying to get in here – it’s very important to have our culture, the quality of our people, have mystique in the market,” says Grisi.

But arguably more important is that it has improved customer service. The bank tells Euromoney that in the last three years it has increased its level of employee engagement from 75% in 2015 to 82% in 2018. It does not provide customer satisfaction data, though it seems fair to assume it maps in a corresponding direction.

Santander clearly believes the link is real, whether or not it has the hard financial data to prove it. Also, Alvarez says that while technology is important to build the number of customer accounts, employees remain the most important part in the customer experience.

“Customer satisfaction with digital tends to be very high… until they have a problem,” he says. “If there is a problem, then customers call contact centres to fix it, or if it’s more serious, then it’s face to face. This is where high value is created. Making a customer loyal happens [then], when things go wrong, [at the point when customers are asking] can [the bank] solve a serious problem?

That’s when customers feel they receive value, and that’s where we take care of employees.”