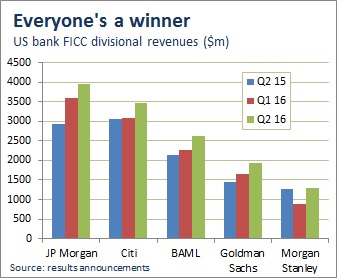

Reporting results in late July, the big-five franchises turned in more than $13 billion of revenues from their FICC divisions, up 16% on the first quarter and 22% on the previous year.

JPMorgan reported the biggest year-on-year increase despite starting from almost the largest base, its 35% jump taking revenues to a shade under $4 billion. The bank conceded that this had followed a “weak” second quarter in 2015, when it had been trumped by Citi in fixed income (see chart). JPMorgan was back on top this time around, however, with Citi generating fully half a billion dollars less fixed-income revenue than its rival.

|

JPMorgan’s business was more than three times that of Morgan Stanley — which was an outlier in view of its paltry 2% year-on-year gain, from a base that is by far the smallest of the five. Morgan Stanley CEO James Gorman sometimes gives the impression he would prefer people to stop talking about fixed income at all, although the bank’s eye-catching move to cut 25% of FICC headcount in December 2015 ensured that wouldn’t happen.

But the latest result is unlikely to cause him to lose much sleep. The bank doesn’t break out the profitability of individual product lines, but with headcount slashed by that extent and revenues fractionally up, the figures speak for themselves.

All the banks posted double-digit revenue increases from the first quarter of the year (see table), although Morgan Stanley’s outsize 49% jump was a function of a particularly terrible previous quarter, where its revenues fell by more than 50%.

But a few other things were pretty much universal across the five franchises. Credit was broadly up from the first quarter, as was mortgage business, as spread products – including securitized products – benefited from a tightening in US Treasury bonds. Municipal bonds did better for the same reason. Rates franchises were up compared with the previous quarter and the previous year. Commodities was better, helped by oil moving steadily from $38 to $48 a barrel.

Currencies presented a more mixed picture, however – up at some banks but down at others. One determining factor was how active a firm’s clients had been in positioning themselves in the first quarter, but differences in the precise client mix at different franchises also probably played a part.

All firms reported that the UK’s June 23 referendum on membership of the European Union, resulting in a decision to leave, sparked volatility and volumes in its immediate aftermath.

|

From that perspective at least, Brexit was a positive for all five franchises, although Gorman provided perhaps the most bittersweet assessment of the opportunities thrown up by the vote, noting that while the outcome was “suboptimal”, it did provide the bank with a live stress scenario in which it could demonstrate that its systems were able to run smoothly, allowing clients to access the market. Like others, the firm’s FX business was helped by the additional volatility and volumes in the days around the vote itself, but CFO Jonathan Pruzan noted that “one or two days does not make a quarter”.

Goldman Sachs sent out a similar message, saying that it had been able to be on the front foot with clients as a result of its careful preparation. More notably, CFO Harvey Schwartz said the firm had seen an uptick in market share during the peak of the Brexit volatility, which might have reflected the competitive environment as other firms restructure businesses.

Paul Donofrio, CFO at Bank of America Merrill Lynch, also identified a competitive opportunity, arguing that the bank had increased its relevance with clients through the episode, by showing that it would “be there when they need us most”.

JPMorgan CEO Jamie Dimon’s sore throat had led him to take a back seat in his firm’s results Q&A session with analysts, until coaxed into speaking by CLSA’s Mike Mayo, who wanted to hear from him directly on Brexit. He was typically bullish, pledging his commitment to UK and European clients, adding that if it ended up costing a little more to serve the firm’s clients, so be it. “I am not really worried about it.”

Word on the Street

The sentiment on the week’s conference calls was, for the most part, punchy and confident. JPMorgan was firmly on top, with CFO Marianne Lake focusing on the firm’s ability to meet client needs and provide liquidity, even in the wake of the Brexit vote.

JPMorgan had a disappointing quarter in the same period last year, so this year’s increase was in part a normalization. Lake said the performance was broad based, with rates, currencies, emerging markets, credit trading and securitized products all doing well; rates was particularly strong, she said. Higher client flows in primary and secondary, driven by a recovery in risk appetite as a result of a more stable environment, helped drive the momentum from March into the second quarter.

Lake was reluctant to give analysts a definitive take on seasonality or what she thought the firm’s run rate ought to look like, although she said the last quarter was “not a bad place to start”.

At the opposite end of the spectrum in terms of scale was Morgan Stanley, which has appeared at times over the years to have had something of an existential debate around its fixed-income franchise. It’s clear this frustrates Gorman, who commented drily to analysts that FIC appeared to be the topic of the day, the year and the century. He thinks markets overreacted to the underperformance of the business from the middle of last year and into the first quarter of this year – and he argues that competitors have also cut fixed-income headcount over time, just not as much all in one go.

He says he is resourcing the business for a $1 billion quarterly run rate – it made $1.3 billion in the second quarter. Realigning the staffing level to fit that was one of two decisions he made relating to FIC at the end of 2015. The other was to generate efficiency through bringing all of the bank’s sales and trading businesses together. He wasn’t expecting instant results from that, but said that perhaps the synergies were starting to show. Either way, he wasn’t shocked by the quarter’s result, but then he wasn’t shocked when the firm was doing $500 million a quarter either.

On specific products, CFO Pruzan said that spread tightening had helped the credit business, and securitized products in particular. Better energy prices helped put that sector on a sounder footing, which helped the bank’s commodities business. FX was helped by Brexit-induced volatility.

One obvious worry from a sudden reshaping of a secondary franchise is the extent to which it might affect a bank’s ability to play in primary. But Pruzan resisted any notion that Morgan Stanley’s cuts in FIC were now translating into a poorer performance in debt underwriting, which showed a year-on-year drop of 35%. He argued this was quarter-specific, with “a couple of events” where the bank was out of the financing by virtue of advising on the M&A sell side.

Citi didn’t dwell much on the fixed-income business when discussing its numbers with analysts, although CFO John Gerspach had one interesting piece of analysis in relation to it. Currencies were one of the drivers of increased revenues, and Gerspach thinks he knows why. He told analysts that his firm now makes more than 40% of its rates and currencies revenue from corporate clients, a proportion he reckons is higher than at competitors. He sees that as “a differentiating advantage and one that provides scale and stability to our fixed-income platform”.

As at other shops, spread product did well compared with the first quarter, although it was down year on year.

A slightly defensive take came from Brian Moynihan, CEO of Bank of America Merrill Lynch, who wanted to tackle “head-on” the question that he said many customers had of whether the bank needed to change its global markets business, and especially the FICC area. He said fixed income was a good business for the bank, generating good investment banking fees as well as being an important part of the global markets platform, which posted one of its most profitable quarters in the past five years. The 12% year-on-year increase in global markets revenues was driven by FICC, which was up 22%.

CFO Donofrio slipped a hint of lyricism into his commentary, declaring that “customers and clients were able to live their financial lives better” in the quarter because the bank’s global markets division had delivered for them in challenging market conditions. Improvements in rates, currencies and client activity helped to drive macro and credit.

Moynihan’s desire to be up-front about fixed income was either redundant or did its job perfectly. Analysts barely mentioned the business – Morgan Stanley’s Gorman must have envied that.

There was little defensiveness at Goldman Sachs, although the firm did caution that the environment for FICC remained challenging amid low rates and client activity. Schwartz talked of a more normalized backdrop for the provision of liquidity compared with the first quarter, helping to boost results in credit and mortgages. And better market conditions led rates to perform better. Currencies was down from a solid level of client activity in the first quarter, and commodities fell slightly.

The business at Goldman has also seen cuts in staffing, with Schwartz saying that areas of the firm “that have hit heavier headwinds”, such as fixed income, went beyond the usual annual 5% in Goldman’s latest staffing rejig. But he shrugged off pressures from any shift in the market towards electronic trading. Clients still needed the services that Goldman offered, and they still needed them from Goldman.