By Benoit Desserre, global head of payments and cash management,

and Arnaud Pichon, international desk supervisor, at Société Générale

Source: Société Générale – Régis Corbet, 2016

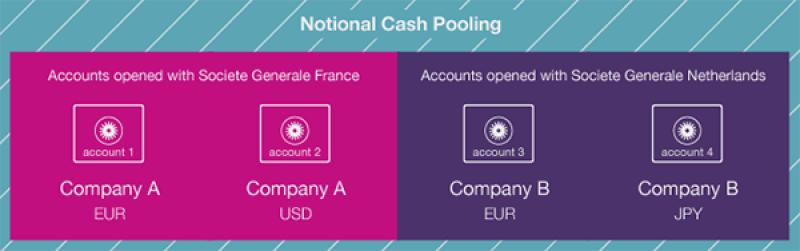

Notional cash pooling allows corporates to manage group finances from a single account, giving corporate treasurers a convenient, consolidated view of accounts that might be spread across a number of affiliated institutions, in different jurisdictions and currencies.

While it is not allowed in the US, it is popular in Europe and Asia as an efficient way for large multinational corporates to manage their balance sheets at a group level. It allows such corporates to offset their liabilities – including those of their subsidiaries – against their assets.

|

Source: Société Générale, 2016 |

But in driving through the increased transparency that is no doubt needed to make the financial system safer, Basel III has created an obligation for banks to report all the assets and liabilities of their clients separately.

This does not have significant implications for physical cash pooling. For notional cash pooling, however, where there has been no physical transfer of funds between currencies, it burdens corporates with significantly increased disclosures of their liabilities.

Where currencies are managed separately but as part of a single master account, the liabilities associated with each currency position will have to be disclosed, and have an equity capital allocation set against them, now often ranging from 11% to 13%.

For the banks offering notional cash pooling to clients – of which there are already relatively few – this is also likely to have implications for leverage ratios and liquidity coverage ratios. The number of corporates using this service is also relatively small, but the ones that do are among banks' biggest and most attractive clients.

Notional cash pooling for these clients can have a material impact on a bank’s balance sheet. In many instances the impact on leverage and the LCR will undermine the case for offering the service to specific clients. In practice it will likely mean some banks pull out of the business altogether.

|

Source: Société Générale, 2016 |

Yet regulation does not change the underlying need for corporates to efficiently manage their balance sheets. Notional cash pooling will still be attractive for clients with sprawling businesses, where the treasurer wants a holistic view of group finances. It frees the company from the need to manage FX positions in the market, which can be a significant cost in itself. It also removes the need for inter-company loans, and gives the group treasurer significantly more control over incoming and outgoing flows within the group.

It also provides significant operational flexibility. Cash pooling allows companies to operate in new jurisdictions without establishing relationships with local banks to provide local currency.

Notional cash pooling is all about efficiency: where a large and diversified group may require many treasurers around the world, it allows the function to be effectively centralised in one location, managed by a single treasurer.

So while some banks may step away from the business because it will be harder to make a profit from it, continued demand ensures that the product itself will survive.

Corporates must therefore prepare for disruption. But they should not be disheartened if their initial discussions with banks do not go the way they hope.

Arnaud Pichon, international desk supervisor at Société Générale, says: “The nature of the product means that while a client’s business might have a significantly detrimental impact on one bank’s balance sheet, it might have a much smaller impact, or even a positive impact, for another bank.”

A bank that has a lot of USD but little GBP on its balance sheet, for example, may reject a client that has most of its cash in USD, but welcome a client that has most of its cash in GBP. A bank with the opposite exposures may take the opposite view. Treasurers are therefore advised to speak to as many banks as possible, to find the bank with the best proposition.

Sustainable relationship

Cash management has traditionally been a sticky business, and corporates have tended to stick with their providers if they are happy with the service being provided. Changing providers requires considerable effort, so many companies will naturally prefer to maintain their current relationships.

Despite this, corporates must use the next two years to examine their current arrangements and ascertain whether they are sustainable. Even if their business is attractive to their bank today, any change of circumstances, such as a large acquisition, could dramatically change the viability of that relationship.

Benoit Desserre, global head of payments and cash management at Société Générale, says: “Corporates engaged in notional cash pooling today need a back-up plan. They should be consulting with their banks now to establish whether the service will be repriced or terminated, because in most cases it will be one of the two.”

There have been examples of banks walking away from the business in the past, demonstrating how disruptive this can be for their clients. Corporates should not wait to receive instruction that the terms on which the service is offered must change.

Instead, they should be actively consulting with banks, looking for a provider that is willing to offer the service at the best possible price.

Société Générale has traditionally been more active in physical cash pooling, intentionally limiting its exposure in notional cash pooling, despite having a full offering capability.

It will therefore not be forced to change the terms on which it provides the business to existing clients, unlike some of its competitors, and will continue to expand its activities in this area.