“I waver between despair – because I see that the changes just aren’t happening fast enough – and hope when small wins are made,” says one sustainable finance head in Asia.

Another in Europe says: “Management is fed up with initiatives, but we are woefully insufficient in speed and scale relative to what science is telling us, and to where we need to be.”

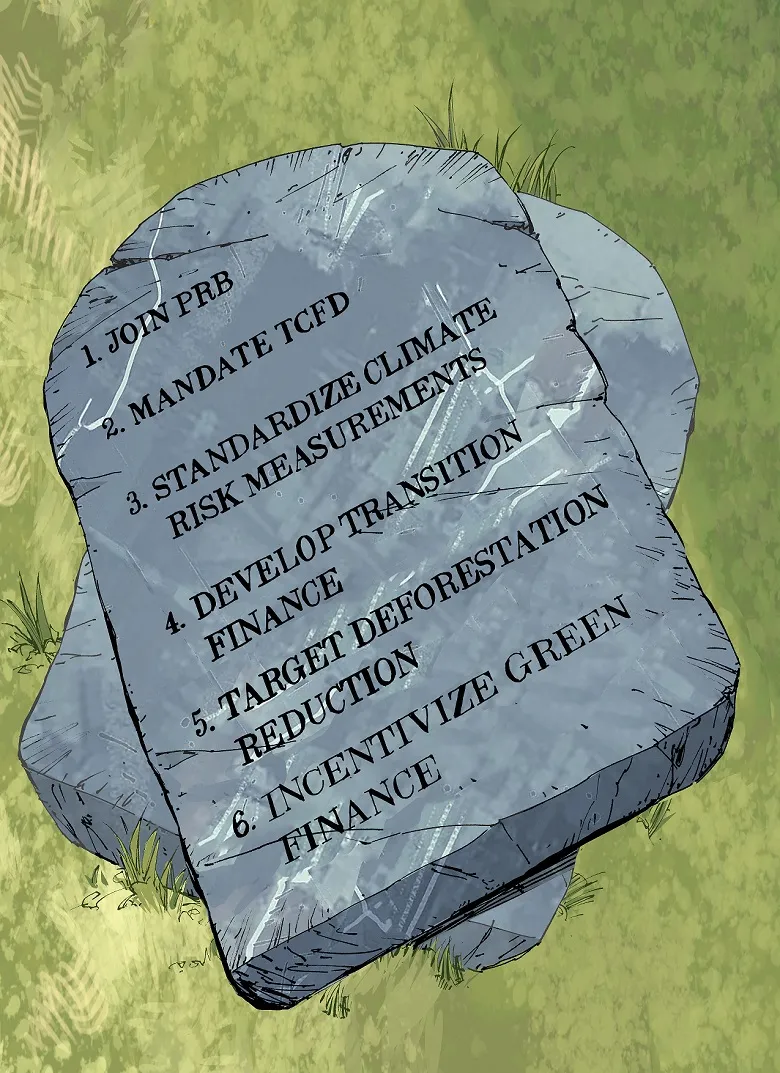

SIX WAYS TO FIX SUSTAINABLE FINANCE |

| 1. Join the PRB |

| 2. Mandate TCFD |

| 3. Standardize climate risk measurements |

| 4. Develop transition finance |

| 5. Target deforestation reduction |

| 6. Incentivize green finance |

“We’re just not moving the needle,” says a counterpart at a US bank.

A North American peer comments: “At banks where very little action is being taken to transform the core business to one that finances sustainably, there’s a palpable feeling of loneliness. Those that work in sustainable finance understand climate change in a way that maybe their colleagues don’t and they know that their institutions are part of the problem.”

Behind the initiatives and impressive numbers that spin a convincing tale of a financial industry redirecting capital away from environmentally threatening businesses towards those aligned with zero-carbon and deforestation targets lies the real story that the banking sector’s regional and global sustainable finance heads speak of away from conference panels and PR censorship.

They lament that, despite the attention it receives, sustainable finance is still a niche sector in the finance market.

That niche, while well-intentioned, is opaque and rife with disagreements, differing terminologies or the same terminologies interpreted in multiple ways. It is bogged down with pledges and initiatives, and hindered by a lack of agreed-upon measurements, standards and disclosure.

Despite many coalitions, they complain there is a lack of cohesive effort and an absence of commitment from key bank chief executives that is slowing progress down.

As the urgency of mitigating climate change and restoring the environment increases, frustrations are building. Those working in the sector say it is time to speak out and fix sustainable finance’s big problems.

That is what more than a dozen sustainable finance thought leaders at the world’s biggest banks have done with Euromoney over the last month. Their views are off the record, but they are heartfelt and spoken with conviction. They want these views to be shared with the banking industry and beyond.

A consensus is forming within this group around half a dozen key steps the banking industry could take that would fundamentally shift climate-change finance from hope to reality. But its leading proponents aren’t as confident as they might be that it will ever get there.

‘Just nonsense’

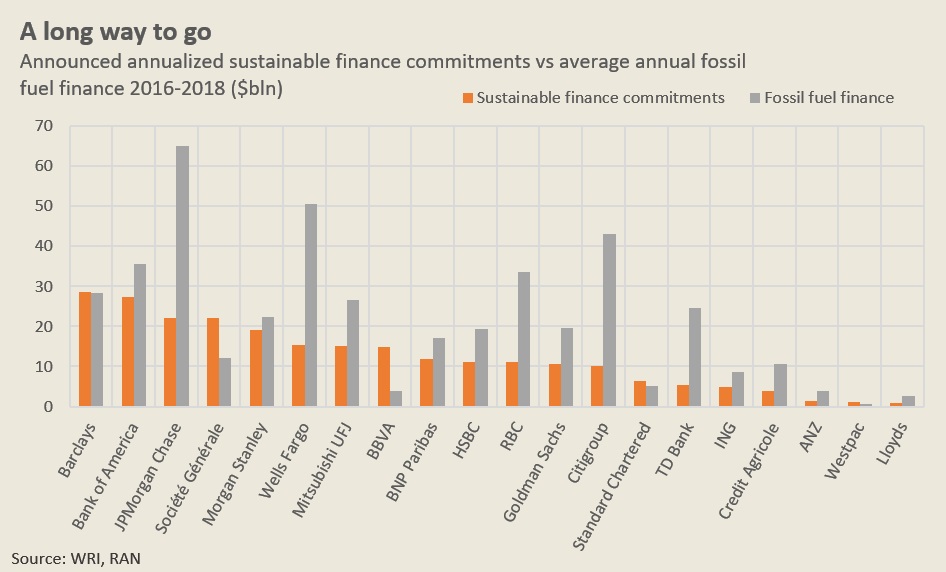

The numbers are certainly impressive at first glance. Of the world’s largest 50 banks, 25 have made public sustainable finance commitments totaling more than $2.5 trillion according to data released in October by the World Resources Institute (WRI).

JPMorgan Chase, for example, committed to facilitating $200 billion in clean financing between 2016 and 2025. Bank of America has committed to mobilizing an additional $300 billion in capital through its Environmental Business Initiative between 2020 and 2030. Societe Generale has committed to raising €100 billion in financing for the energy transition between 2016 and 2020.

|

|

As more banks have announced hundreds of billions in commitments over different timeframes, WRI was asked to shed light on whether such commitments are impactful; its findings were indicative of what many have suspected: there is little way of knowing.

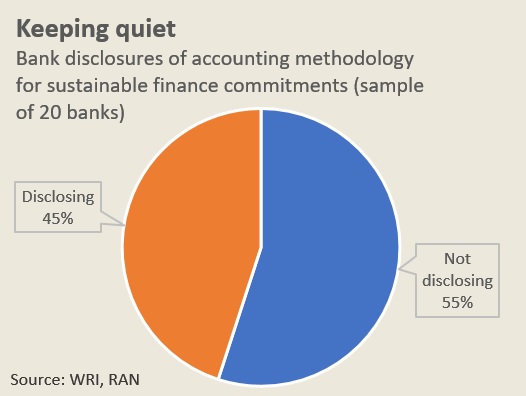

What WRI discovered was that 57% of the banks that have made commitments don’t publicly disclose their accounting methodology: Morgan Stanley, Bank of America, Crédit Agricole and Lloyds are among those cited in the data. And a third don’t even have plans to report on the progress of those commitments.

“These commitments are just nonsense,” comments one former sustainable finance head. “You don’t run a bank that way – putting out a notice that you’re going to finance $150 billion or something in renewables. Finance is driven by the credit people.

“I guarantee at monthly meetings these targets aren’t being checked. It’s just a number these banks know they’re going to meet because the renewables industry is growing. In addition, people doing the work in sustainable finance are often isolated from the boards making these sweeping statements.”

A sustainable finance head adds: “These targets are only set because banks know they will meet them. Banks are not going to say something radical. It’s also a distraction. The whole focus should be on real lending books, not this small portion of green financing anyway.”

WRI’s data also showed that 28% of those banks making a commitment don’t disclose the types of financing they include and those that do have wildly different approaches to sustainable finance.

“Definitions vary so widely that it’s hard to get a clear understanding of what is being done and impossible to make comparisons” – Giulia Christianson, WRI

HSBC, for example, includes asset management in its $100 billion sustainable financing commitment. JPMorgan’s $200 billion is specific to clean energy financing. BNP Paribas’ €185 billion targets the UN Sustainable Development Goals (SDGs). BBVA’s €100 billion pledge encompasses green finance, sustainable infrastructure, social entrepreneurship and financial inclusion.

“Definitions vary so widely around sustainable finance that it’s hard to get a clear understanding of what is being done and impossible to make comparisons,” says the report’s co-author, WRI’s head of sustainable investing, Giulia Christianson. She says WRI is engaging in a second round of research.

One area of sustainable finance that should be less opaque given the formal framework around it is the green-bond market, but even here impact is difficult to measure. While green bonds have been praised for bringing ‘use of proceeds’ into the debt markets, a study by the Climate Policy Initiative (CPI) released in November showed that it is not as transparent as some would like to believe.

Chavi Meattle, who co-authored the CPI’s report, the Global Landscape of Climate Finance, says that, of $53 billion in green bonds and loans tracked by the Climate Bonds Initiative (CBI) – widely regarded as the most thorough green-bond database – only $2.8 billion in annual primary investment for climate action could be identified in the post-issuance reporting.

It highlights “the clear disparity between total issuance and the amount of new investment that can be tracked within green-bond reporting practices,” says Meattle, and shows that “significant improvements are needed to ensure full market transparency and timely disclosure of use of proceeds.”

Making a difference?

Such findings throw shade on the idea that the green-bond industry is flourishing. The numbers would convince us that it is. For example, green-bond issuance is expected to reach a record of $250 billion this year, versus $170.9 billion last year.

But the real question is whether that $250 billion is financing new green projects that otherwise would not have been financed? Is it making a difference?

Sustainable finance heads are in agreement that the answer to both is no.

“Green bonds are a good development, bringing attention to finance’s role in the environment, but we need to be more honest about them,” says one banker. “Green bonds are just conventional bonds relabeled, re-batched and they are not moving the needle at all. If we want to tackle the climate emergency and drive the Sustainable Development Goals, we need to move capital to places of greatest change – to encourage that which isn’t getting funded to get funded.

“You need only look at the slim amount of green-bond issuance in emerging markets to know green finance is not helping a change.”

According to the International Capital Markets Association (Icma), emerging markets issuance accounts for about a quarter of all green-bond issuance to date.

“Are we truly creating additionality with green bonds?” asks another banker. “Not really. Let’s be honest that many of these companies accessing the green-bond market would have got funding for their efforts anyway, and they would have made those decisions anyway. Green bonds are not going to change the world.”

There is also the uncomfortable fact that set against traditional finance, green-bond financing looks small. Some $202.2 billion in green bonds and loans was issued up to October 22 this year, according to CBI, and one third of that financing was within the energy sector – $66.7 billion.

It is difficult to make accurate comparisons with the larger market but as a guideline, data from Dealogic shows the energy sector as a whole raised $555 billion in traditional bonds and loans over the same period – about eight times as much.

The same goes for sustainable finance more broadly. There is no accurate way yet of showing sustainable financing from banks versus brown financing, but WRI offers as a comparison banks’ sustainable finance commitments from last year – $292.3 billion – against Rainforest Action Network’s data on fossil fuel financing from the top 33 banks alone for last year – $654 billion – more than double.

JPMorgan, for example, financed $63.9 billion in the fossil fuel sector in 2018 – $18.01 billion was for oil, gas and coal companies expanding fossil fuel production or extraction. These figures offer some perspective on the bank’s average annual sustainable finance commitment of $22.2 billion.

Such comparisons irk bankers and their PR teams, of course. They will point out that pitting their public sustainable finance commitments against fossil-fuel financing is misleading; that within their financing to the fossil-fuel industry and other carbon-emitting sectors are deals that are designed to lower emissions or that offer ‘less worse’ scenarios – for which there is no rating spectrum.

Some bankers commenting on the Saudi Aramco IPO, for example, point out that the firm has the lowest emissions of any fossil fuel company.

“Environmentally, one could argue this is a firm we should be financing versus others given we will be relying on oil and gas for decades to come – although on the social and governance side there are some concerns,” says one.

Another banker on the deal points out that is unrealistic to expect banks to not finance oil and gas while viable alternatives have yet to be discovered.

Another former sustainable finance banker, however, says it is mere hypocrisy: “How dare those banks go all-in on the Saudi Aramco IPO – a $2 trillion fossil-fuel company with no transition strategy – if the same institutions publicly state to support net zero carbon emissions by 2050?”

“It’s the elephant in the room. We need to drastically rebalance portfolios away from fossil fuel” – Sustainable finance banker

A similar response is voiced by the growing number of non-profits that are highlighting the contradictions between banks’ sustainable finance initiatives and the continued financing of coal.

“Banks like HSBC, Standard Chartered and Citigroup pretend to be climate leaders, but in fact our research shows that they are still among the world’s top 10 lenders to coal plant developers,” says Heffa Schuecking, founder of environmental and human rights non-profit Urgewald, which tracks coal financing.

“HSBC, for example, has a policy to stop providing direct finance to new coal power stations – but with the exception of Indonesia, Bangladesh and Vietnam. Those countries combined account of one fifth of the world’s total coal plant pipeline. That’s not a non-coal policy.”

That what should and shouldn’t be financed in the fossil fuel sector is still being debated (despite scientists’ warnings that we have to reach peak emissions next year) frustrates many in the sustainable finance sector.

“It’s the elephant in the room,” says one sustainable finance banker. “We need to drastically rebalance portfolios away from fossil fuel towards sustainable sectors.”

And it’s not just fossil fuel financing that is the issue. Earlier this year, Amazon Watch highlighted banks’ roles in financing companies that are driving deforestation in the Amazon. Its report highlights billions of dollars of loans to beef, soy, timber and leather companies from banks including Santander, Barclays, JPMorgan and Credit Suisse that are exacerbating deforestation. Forests and Finance runs similar data for southeast Asia where the top forest-risk creditors are Maybank, SMBC and Mizuho.

Christianson says WRI’s research initiative shows the inherent difficulties of finding data on bank financing to sustainable projects versus environmentally damaging projects.

“While we don’t have the data yet to be able to ascertain with certainty where finance is flowing to overall,” Christianson says, “there is ample information for us to know that there is simply not enough being done. We need greater commitments, a faster transition out of fossil fuels and other harmful industries – and greater clarity.”

Message of hope

Despite the frustrations, those within sustainable finance are mostly hopeful that the financial sector as a whole is moving in the direction they prefer; and most agree that for now they can have the biggest impact by remaining within the industry.

“When I started in the role an activist friend said: ‘OK, you need to get them to stop financing coal, then palm oil, then LNG [liquefied natural gas] exports, then fracking, then weapons,’ and the list went on and on. I would be the least popular person in this bank if I led with that agenda,” says one head of sustainable finance. “It takes time to build a case and get the heads of risk and investment banking to engage in an educational process with you.

“Is the pace frustrating sometimes? Yes. Are there things I wish my bank did not do? Absolutely. Do I see change happening? Yes, and I also believe I can make more of an impact in transitioning finance sitting here than if I worked for many of the NGOs.”

“I am torn,” says another. “Having worked in the NGO sector I know that things don’t move any faster there. But if finance and banking doesn’t clean up its act, then no one will want to work here – certainly not millennials.

“It’s a difficult spot to be in. I understand many of us within sustainable finance are frustrated, but if we leave, then banks will move even more slowly. We need as many people fighting from within as we can get.”