|

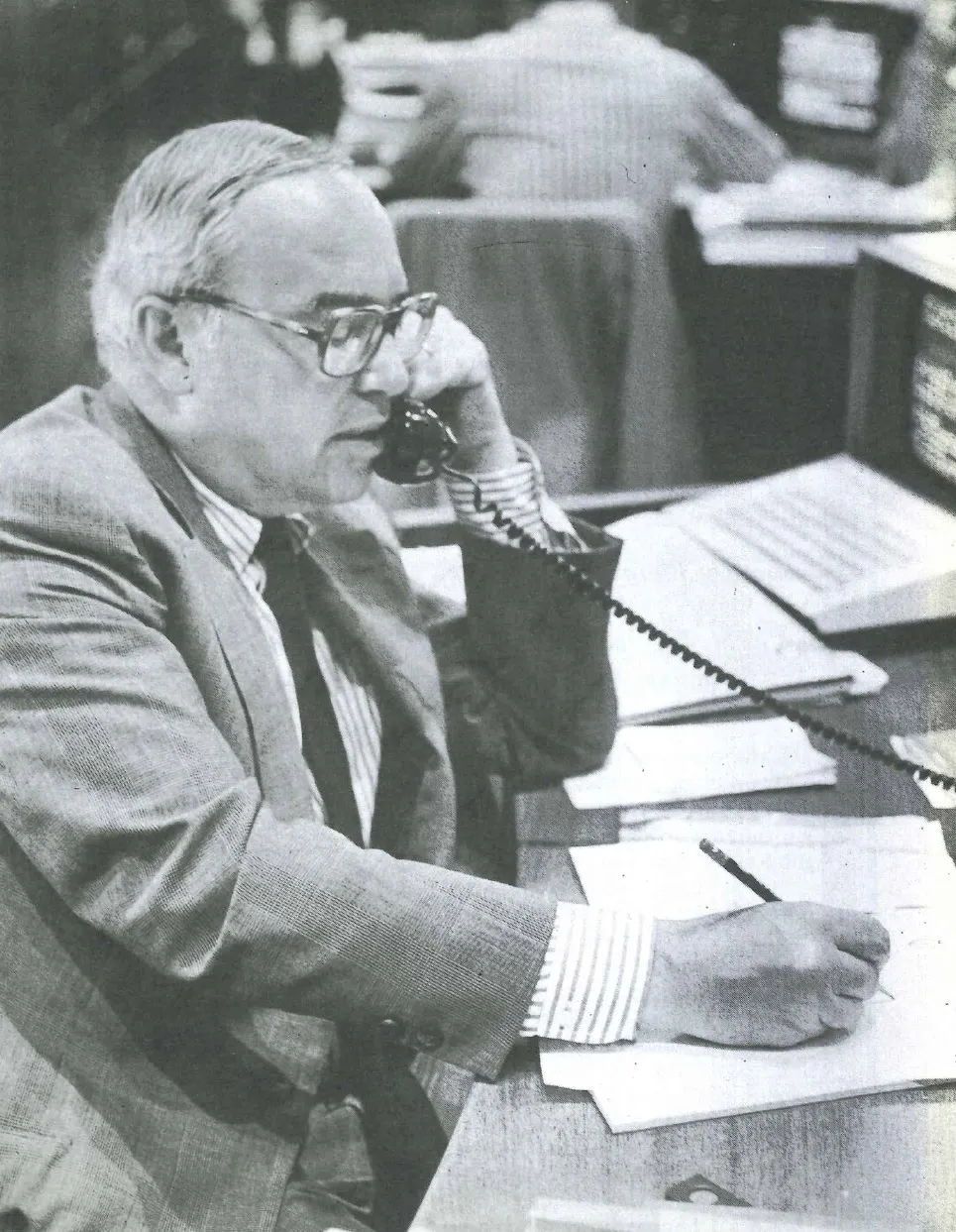

At the end of what is probably the most famous trading room in the world sits the world’s most famous trader: John Gutfreund, managing partner of Salomon Brothers, a portly, restless figure who, like a vigilant bear, stalks the corridors between the trading desks in the vast trading expanse that is known as the Room.

Characteristic cigar in hand, he doles out advice to individual traders, some of them partners, always with an ear cocked to the noise level of the Room, gauging the mood, minute by minute, second by second, of the biggest capital market in the world, and responding instantly, with characteristic conviction and snap, to its movements. It is this instant ability to read the mood of the bond markets of the world, and the US bond market in particular, that has made Gutfreund’s reputation not only as a trader, but as a dealmaker and a strategist.

Where his colleagues at the top of other Wall Street houses might start from the top and work down, Gutfreund starts from the bottom and works up; Salomon’s bond deals stem from Gutfreund’s vantage point in the Room, from his knowledge of, and feel for, markets. This is what gives him and his partners an instant awareness of how an offering will sell. They are not always right, but they are more often right than wrong, a fact that became important to the Euromarkets over three years ago when Salomon brought its big-buy, precision trading into the international markets, when it opened its Eurobond trading operation in London.

|

Soon practically every Eurobond trader was paying tribute to its professionalism. Had many of them been Wall Street houses, they would have known what to expect, because Salomon Brothers’ professionalism in the trading business had brought it, with almost devastating success, into the issuing business at home, first into municipal issues where competitive pricing is all, and (more slowly than one might expect) into corporate financing, where relationships matter more.

Only in the last two or three years has Salomon convinced corporate America that it is more than a bond house. Though Wall Street has long since (perhaps grudgingly) acknowledged its professionalism, many of the major American corporations have yet to grant it the status of a Morgan Stanley, although the house now includes some of the world’s best dealmakers, including its Chicago-based partner Ira Harris and its bouncy mergers and acquisition specialist, James D. Wolfensohn. It also numbers Dr Henry Kaufman, probably the best judge there is of US interest rates, as a partner; important, because US interest rates are the air that Salomon Brothers breathes.

“The whole nature of Wall Street is changing; it’s becoming more institutionalized and professional”

From the moment that markets open to the moment they shut down for the night, John Gutfreund’s presence dominates the Room. But long before markets open, and long after they close, Gutfreund has been at work, presiding, for example, over the 7.30 partners’ breakfasts at which deals are hatched and strategy planned. A visiting European banker described it as “a crucible, where the man [Gutfreund] sparkles with ideas. Twelve hours later, he’s as fresh as ever.” The man’s energy and bounce is legendary.

This is Gutfreund’s first year as managing partner of Salomon Brothers. He took over from Billy Salomon, a likeable, charming man who was reputed to be less abrasive than Gutfreund, in April of this year.

Gutfreund does not like to be called abrasive, still less dictatorial. There may be some truth in those comments, but Gutfreund is too complex to put a label on. He’s genuinely hurt by these criticisms, because he feels they’re not accurate, and Gutfreund has a passion for accuracy. His greatest joy is to watch a deal done elegantly and successfully. His greatest fear is probably one of missing great opportunities because he is too bound up with the immediate business. That impels him to look constantly outwards from the Room, and it is probably the main reason for his recently acquired intellectual fascination with the commodity markets.

On a sultry summer’s day in New York, Gutfreund retired to his office, just off the Room, to spend the morning talking to Euromoney Editor Padraic Fallon, in the first full interview that he has given. The issues ranged from Salomon’s business to Gutfreund’s private philosophy, his style of work and his views on politics — he was among those airlifted to Camp David to put his views to President Carter, during the fateful policy rethink.

It’s been said that you’d trade the furniture if you’d nothing left on your books. Is trading still the key to Salomon Brothers’ strategy?

It is the bedrock expertise upon which we have built a fairly broad business. But we might not be trading the same items as formerly. “Furniture” might be gold pieces, silver pieces, grains, futures.

We’ve heard about Salomon Brothers being on the edge of the Wall Street Club of elite investment bankers. Do you consider yourself to be a member of the club, Or are you like Groucho Marx who said: “I don’t want to be a member of the club that would have me as a member”?

For good or bad, we are totally members of the club and have been for some time, but the club is no longer a club in the classic sense. It is not where members choose each other and their offspring and where their families are automatic members. The whole nature of Wall Street is changing. It is becoming more professional, more institutionalized and more oriented toward achievement in a highly competitive climate. In the future, it will not have the pleasant clubby atmosphere and all that suggests, the personal values, the pleasant amenities, and the deals among gentlemen. Being almost 50, I guess I shall miss what I recall of that, but I believe the other side of it is that intellectually I shall have a challenge for the last part of my business career in running something that is more like a corporation.

You, probably more than any one man, have done more to change that pleasant clubby atmosphere for the more professional, institutionalized one.

You give me too much credit.

As a house, you have done just that.

Salomon Brothers as a house did not change the club. We joined it and the way we did was by our aggressive merchandising and trading techniques. We took what we deemed to be appropriate risks to place ourselves in the investment banking community. Historically in the US the secondary market firms — the trading firms — were very different from investment banking firms, and although investment banking firms from time to time had to engage in the secondary market, they fundamentally left it to brokers and strongly-capitalized dealers like us.

The bond houses.

Yes. In the convergence since World War Two, the US went institutional in every way, pension funds, mutual funds, and State and local retirement funds. The Federal system institutionalized many aspects of American life. With hesitation and considerable dragging of feet, Wall Street has followed along.

|

I think they will become more and more isolated. There will be times, when, due to good fortune, acts of God and chance, people will do very well. I think we shall continue to be a highly-compensated industry in one way, and that is because we are in the money business and in a risk business. The question is whether the large institutions that will dominate Wall Street in the future will have in their grip these very high earnings. My suspicion is that they will not. I believe that we shall have more uniform quality, fairly high standards, much like a law firm.

Are you glad about that, sorry about it, or mixed?

I am mixed and sorry. I am glad for the challenge, but the most interesting element is how to retain the very bright entrepreneurial people who have sought where the action is and where the large money is to be made, and who may now feel that when they reach a certain point that they can do better on their own. They would rather set up what is presently called a boutique, or a small shop, or go their own way. I worry about that, because it is a real challenge. Conceivably, we may not be able to meet this one because large complex institutions do not necessarily lend themselves to keeping the brightest stars. Sometimes, there is too much conformity required of people. Sometimes, there is too much of what goes on in the legal profession — that after the third year one will get $X per annum, after the fourth year it will be $Y per annum, and in the sixth year one will become a partner. It is like tenure. Tenure has the effeet of atrophying a great institution. I am afraid of that and I want to avoid its happening. Recognizing the dimensions of a problem is a large step toward its solution.

How can you stop it happening?

So far, the whole idea for me is to maintain us as a medium-sized firm, to offer the challenge of great progress in terms of new markets and new skills necessary to maintain our position. There is no question but that there is enough to fill the “book” for the next 10 years in these terms.

When you say “keep yourselves medium-sized”, what do you think of? Do you think of the number of partners?

I am thinking of the number of decision makers: partners, seniors, etc. We have now 2,000 people. That is minute compared with a bank or a major industrial company. Of those 2,000 people, we have in the neighbourhood of 500 to 600 decision makers. Even with 500 to 600 decision makers, a firm has to begin to develop some real structure. There is no way that I have enough time in the day to get the inputs from 500 people.

You’ve said that what you like best is tackling a complex problem. Why?

I like the idea of solving a problem that has many parts. That is precisely where we are now, in terms of running Salomon Brothers, because we have some very talented people here, and they do not necessarily agree on everything. It is like listening to the major economists. If one were to make a decision in the US and one listened to Milton Friedman, Arthur Okun, Walter Heller, John Galbraith and Lawrence Klein, one would never reach a decision because they have five different views, all centred in their own disciplines, all very bright. So how does one reach a decision? I do not mind that procedure, listening to the five of them and trying to put together what makes sense. I have that kind of thing here in microcosm, with people like Jim Wolfensohn and Henry Kaufman, who are very talented, bright fellows. Their judgement on every matter is not always the same. But they are experts on different things.

Presumably you listen to Henry Kaufman on economics and Jim Wolfensohn on deals?

I listen to Henry Kaufman on anything. In some areas he is truly perceptive. Jimmy is much more of a renaissance type, but he is not without very considerable negotiating skill. He has been an enormous addition to our firm.

It’s said that he came in here with a brief largely to be an administrator, but that he goes out and brings in deals — which is marvellous, but negates the original purpose. Is there any truth in that?

Let me ask you, when you marry, or when you develop a relationship with somebody, do you ever get what you expect? You get a lot more and a lot less. In the case of Jimmy we got a lot more. Jimmy’s original mission was to help organize our corporate finance and new business areas in a better fashion. However, to ask a man of his breadth and talent to do that, and to deter him from doing what he does most elegantly and successfully would not make sense. So what do we do? We have him do all of that which means he works far too hard, which is his style anyway, and over time we develop a cadre to take on some of the other chores with which he has been charged. But so far he has done everything that has been asked of him.

|

My suspicion is that I am already that way but do not know it. I give the impression of being very gentle and nice in some ways, but of being fairly abrasive in other ways. One of the problems is that I may not suffer fools gladly, but sometimes my judgement may not be all that good. There are areas in the business as things go on that are beyond my ken. There can be people with ideas that are ahead of me. That happens.

Are you receptive to those, or do you shutter yourself against them?

No, I think about them. One of my weaknesses might be that I would say “No,” and then I would have to think about it. For example, we had not been as progressive in understanding the relationship of futures and commodities to cash in the marketplace as we should have, and there are one or two young people here who saw and understood that. It is not an easy thing to understand. If one is dealing in the money business, the cash business, then the commodity business is something different. It is a matter of expectations. The money business is psychological, but the two are not in total synchronization because the leverage in the commodities business is a multiple of leverage in the cash business — which is a fascinating exercise. We in the United States have been so insular that we have not understood the need to think about what is at the centre of the universe. Is it the dollar this week? Or the Deutschemark? Or the yen? If one is centred in the dollar, and one is centred in stocks and bonds and commodities in the dollar, one then has to look at a world that may be centred in D-marks and D-marks securities, currency, the whole game. This is very exciting, and what I view as a great new horizon for business — if we can move ourselves quickly enough on the learning curve. But, once in a while, I have not been as quick as I should have been in listening and thinking.

But you are not behind your major clients in that. Your major investment clients are very familiar with stocks and bonds and other types of US investments, but perhaps they’re not alive to the other investment opportunities around the world. So why you more than they?

Because we are leaders. We are leaders in this industry. If I can contribute anything to the administration or to anything else, it is because I understand something about what is going on internationally in the world in relation to money. Not in relation to a lot of other things.

Will this thinking bring about some fundamental changes in the business?

It already has.

What name would you put to those?

The universe of our liquidity will be different from what it was. That is, it does not necessarily exist in the United States, or in Europe, or wherever. It can be almost anywhere. It is in Asia from time to time; it is in the central banking system. The US government market historically has been a very large numbers market and the foreign component of investments, mainly central banks, but also private parties, South America, Asian or whatever, was recognised only through the Federal Reserve statistics. We never accessed them directly. Now we do. Again, the pie was so big in the United States. The pie is still huge in the United States; however, the opportunity, the maximum way to capitalize on the opportunity is have the largest information base and to be able to use it. Foreign investment in the US and flows of funds are a very important part of that, but they have never been properly understood by the investment banking community. We are beginning to get to that. What that means is that my base intellectually should be not just New York, but London and Tokyo and wherever.

It is all one world, but, intellectually, does the international side excite you more now than the domestic side? You sit out there in the Room and you have a lot of domestic American capital market transactions coming across the screens. One would imagine that your focus would be on the domestic market, and yet your achievements don’t suggest that at all.

My mooring is to the domestic market, because it must be. When I deal outside of the Room, outside of New York, I must be as well grounded in the US market as is possible. At the same time I am very interested in the opportunities abroad. We have been very active over the last years in floating rate investment instruments. If you look at the attitude outside of the United States and the understanding of that, it has been a fantastic opportunity for us to import something that we did not really handle very well in the US.

Into the United States?

Sure.

From Europe?

From Europe.

That makes a change.

But there are other things that we can import. In the banking world, because we were so insular, and because of regulation, which is an excuse, we did not have to innovate. That is what has been the excitement about Europe. The Eurodollar, which is really the world dollar market outside of the United States, has been an enormous opportunity and great challenge. Those dollars will be around for a heck of a while, and we want to get our share of them in terms of transactions.

|

Gutfreund on politics |

|

You were one of the people who went up to Camp David recently. What advice did you give President Carter? What did he ask you? He asked each of the people to represent his views, or questions, or thoughts. I went with a group of economists, and I listened to them. Many of them were very elegant and expressed themselves forcefully, oftentime convincingly, but with totally opposite views. I felt very sympathetic to the President. I had never been to Camp David before. It’s a credit to the country in the way it is managed and in its character — what we would call rural, simple, properly maintained. It is not a lavish rich man’s castle. The style appeals to me. I suppose that reflects my liberal democratic tendencies. The simplicity of it? Yes, the simplicity of it. And the style of the meeting was proper, broad- ranging, comprehensive. My views on de-regulation and my views on economic matters are truly not very profound. But they’re probably practical. They might be. Unfortunately, my strength is short range and my expertise is in the money business, and the money business is mainly a matter of confidence. It is a psychological game. The long-range planning that a President has to do is something else again. It seemed to me, although I am not awed, that it is presumptuous to go there cavalierly and attempt to provide answers for all the problems. Do you not feel that the long-range planning that the President has to think about at the moment is more to do with getting re-elected than with solving the energy crisis? One does feel, looking at the President and his job, that his advisers would tend to lead him toward the fact that votes are counted, not weighed. But one has to take a longer view. I think the President has been agonizing and attempting to do that. He is what I would call a good American Christian and his values are the values that all of us in this country have inherited. The pragmatics of politics make us fall into a compromise system of life that is pretty difficult. I did not have many suggestions. I had more questions than suggestions. What were your main questions? I see the country going from crisis to crisis, and making decisions at the time of crisis, which is a very poor way to have to run anything. For example, there is not much question but that it may take a number of years to get the small-is-beautiful thesis through to the American car-buying public. As a consequence, the automobile industry, up until this last gasoline crisis, has been faced with the American public’s demands for a large car. So I tend to be unsympathetic to a crisis where every car owner is moaning about not being able to get gasoline when he is driving a car that gets eight or 10 miles to the gallon and pays no attention to that fact. There is just no conceivable excuse for this irrationality. For decades and decades, energy has been very cheap in this country and the public has squandered it. The public has been indulged by cheap energy and as a result there has been no cost incentive over the past 50 years to improve the automobile engine in the US in terms of consumption. This is ridiculous. Did you tell the President that? That was approximately my message, but what I really said was very philosophic and that does not help somebody who’s running for election next year. It does help to know that people in the country still care about the values and that we cannot lose sight of them. Fundamentally, I feel that the politicians are always at least two steps behind the people. The speech that the President gave the Sunday after we were down there and the subsequent speech in Kansas City were more in response to the outside than previously. But then, unfortunately, the cabinet reshuffle was announced in very bald terms. If there had been a debriefing and a background it would have been much better. As far as the liberal Democrat goes, I am fiscally conservative. Socially I tend to be like any American. I feel we have had great good fortune, and that great good fortune is something that requires us to maintain a level of replenishing the system, contributing back. Have you ever felt that you would like to be in government? Every time I go to Washington I think, “My goodness, I could never handle that.” I would like to contribute but I really do not know, other than judgementally, what I can contribute. I am not a technocrat in any way. What can I contribute? Bill Simon came out of this house and he didn’t do a bad job. Bill did a very nice job. But Bill has a different sense of himself than I. Bill’s Bill. You sound a little uncertain of your own capabilities. Yes, that is correct. That is, those outside this business. I have no doubts about my ability to run this business satisfactorily. |

It seems that the Swedish issue is just another step along the road away from the traditional commission system in the bond market. Is the day of the big commission over?

No, none of those things changes overnight, because where there is some control over a domestic market it will be possible without question to maintain in certain countries. It will be possible to maintain those commissions – but in the long run they are bound to go. The institutionalization of the US market will follow in other more developed countries, and with that institutionalization it is not economic to have large spreads. Even now, for the last couple of years the spreads have been a myth in Europe.

To some.

Except where the infrastructure and indigenous scene permit the controlling of it.

Right. Where there may be captive retail clients.

But in the United States this situation has already developed. Here, too, the marketplace has determined that one cannot make that much. I think it is inevitable that this will happen in the other developed countries.

Do you see yourselves as a house that will hasten that process along?

That has always been a problem to me — the difference between being an innovator or someone who is attempting to destroy the fabric of what has been very good for us. Many would accuse us. I think we shall be very careful with whom we innovate, and how we innovate, and try to think of the consequences of our acts. In the case of Sweden, as I said, the international bond market is much more institutional and deeper than had been thought, mainly because all those dollars around the world are not necessarily in an enclave. Simultaneously, we have these spreads where the weakest underwriter will determine the margin on an issue by taking, 50, 75, 90% of the spread, or 100 or 150% of the spread, and re-allowing it. It is very difficult for me to figure out how we are to go from modern US syndicate practices to modern European syndicate practices without some dislocations taking place and without acrimony from time to time.

In other words, the Eurobond market is splitting itself into two. The investors are divided into retail or non-yield oriented clients, and the institutions which are yield oriented. And there are the banks that cater for each type of client. How will it develop from here?

In the long run, it is my suspicion that individual savers in Europe will be educated by the press as they have been in the United States. When savings rates were 5% in the US, and we deregulated and 6-month certificates became available at 9%, then the money in the savings banks went out one window and in the other window. It is my view that the same thing will happen in the bond market, and the same thing has to happen in time in Europe. People learn, and people who are smart enough to save money will know what terms are available. They cannot all miss all the newspapers, and investors in Europe cannot all believe that they should pay par when bonds are offered freely at 98½. How much do you read in any of the European publications about the investor’s rights, privileges, or what kind of a deal he or she gets?

Zero.

I think it is imporant, but I am darned if I should write that article. We are an institutional house. But institutionalization of funds will cause that to happen. So what we should try to do is to work out a system with self-regulation in Europe, of which we should like to be a part, where an underwriter makes reasonable compensation for his efforts, but where the investor gets a decent deal.

That will bring you head on with some fairly entrenched factions.

I would hope it won’t. I would want to be careful.

Because you haven’t been there too long?

That’s right. We are on very new ground, but I know I am right in the long run. The individuals are just not going to stand still for that. If they are allowed to invest, if the system encourages savings, they will not take 5% if 6% is available.

Is the Swedish issue more fundamental and more important to the bond market than, say, the EIB tender issue was?

I think it is more important from an investment banker’s view. The tender issue is a very complex matter. One of the questions about that tender issue was the minimum size. The logic of that – would you like to explain it to me?

I would say from where I was sitting that the European Investment Bank has got a pretty small staff and is not capable of handling a lot of applications for small lots.

The tender system in the United States has been tried a couple of times by Exxon in the municipal market, and the results were inconclusive. That is a disinterested remark. As a market grows, as the Euro world market grows, in whatever currencies, there is a place for underwriters, and they ought to be compensated — perhaps not as much as they were in the past, but compensated. I am not particularly partial to using our resources to subsidize an option that permits no profitability for us, so I have to believe, unless I can make a good trade, it is not the first priority. The first priority would be an orderly system of which I hope the Swedish underwriting might be the first item, whereby the issuer gets a fair deal and the investor gets a fair deal and we manage to receive some sort of compensation.

|

Gutfreund on running the business |

|

How can you run a business in the noise of the Room? It might seem difficult. But if one grows up trading on a street corner or in the midst of a pit, or in a large dealing room, one becomes acclimatized to the street sounds, the pit sounds, the trading room sounds, and one can edit out a great portion of them. Subconsciously, one will absorb many, many of them, and that is worthwhile because the information that one is asked to provide on a minute-to-minute basis is normally of the immediate market sort. If I am asked to make a decision of a policy nature, I would not choose to do it immediately unless it were a rote type of decision. I would think on it. I would probably consult better brains, and I would reflect on this counsel. Normally, policy and longer-term decisions are made after a lot of input, and very slowly. I am not always a quick study — I am a quick study in the marketplace, but I am not a quick study on changing policy. Sometimes policy changes because the tide is moving one way or another, and this is when one has to be aware and to think through why it is moving as it is. Yet you have a reputation for very snap decisions. I have that reputation, and that reputation is based only on market items, trading. After all, the role of an intermediary, an investment bank, is to be right at the moment. The really difficult job is for the borrower or the lender to make his decision. They have to live with their decision. We have to be right or wrong — for only a moment in time. The concern with us is the liquidity, because of leverage. We are a typical investment bank, highly leveraged. You must be, because you have a great name for big buys. Of any type of high-grade security where, in our judgement, there is liquidity. Keep in mind that our orientation is more toward bonds — classically — than towards equities even though we are today a major factor in trading large blocks of equities. The reason is that bonds, if they are not worth 9% on the current market, may be worth 9½%, or 10% or 12%, and we can assess the odds against the risk factors. How many institutions in the world will buy a telephone bond? If one is in a telephone bond, a Treasury bond, or a UK bond – if one is wrong at 9%, somewhere between 9, 10, 11 or 12% one can sell them. The odds are always against, but that is the nature of the game. But when you start to talk about equities, the more speculative bonds, medium-grade securities, then it is a different question, and a problem. A stock can be worth zero. With a bond, a high- grade bond, normally the interest rate and the currency value will determine what it is worth. Which do you enjoy most — the deal making, or the administration, trading or a mixture? I enjoy watching a deal, whatever the deal is, done superbly. I like to see something work really well. Do you like to dot the Is and cross the Ts? I like to see our judgement vindicated. In our business, normally one would make an intellectual commitment, and then it becomes a financial commitment. When one makes it, if it is a sizeable commitment or a new type of commitment, the world vindicates it. The marketplace is a judge and a god in that circumstance. For example, this last Swedish deal. We made a judgement there, and it was interesting. I do not know whether it is forever. It is much too soon to judge that kind of thing. But in terms of technical skills and judgement at a moment in time we accomplished what we desired. That gives me great pleasure. Administration is not as exciting, but clearly it is essential. How much time do you spend out of the country? Not that much. Maybe 5% of the time. Not an enormous amount of time really. Do you think that’s enough? The first year of being a managing partner, I felt that I had to be available in New York. I would like to travel more. I enjoy meeting bright people. One of the privileges of being in my job is that from time to time I meet bright folks. What mistakes have you made in the business? Most of the fundamental mistakes were on the people side, elevating people beyond their ability, beyond their competence, beyond their willingness to work. Running a partnership is different from a corporation. With that as an excuse, I have probably made more compromises than I should. Those compromises might not have been in letting us continue bad practices in terms of how we had run various departments of the firm. I have tolerated too much inefficiency which has sapped some of the energy. It is very hard to turn that around because inevitably one has to make that harsh decision and to say: “I am very sorry, no.” |

You opened your Eurobond trading operation in London in 1976, and that looked a very professional operation, but it looked as if you were initially more determined to show that you were doing it professionally, and profits might have come second. Is that a misleading impression?

No, that is exactly correct. We had been studying the European market for many years, and we decided to allocate some talented people, in our judgement. We brought a fellow named Bruce Carp on the scene. I must admit there was some question among my partners who asked how we could allocate somebody as good as Bruce to London, and we indicated that in my judgement if we did not go the right way it would not be worth doing. What I meant by the right way was that we would attempt over time to establish ourselves in the world market with the same credentials that we had used in the US, to build on the same base, the base being marketmaking expertise. We found receptivity, but fundamentally we ran into a windfall because we had a favourable market for part of the time; we were very lucky. However, that is one of those things that can go either way.

But it’s not so favourable now.

I have enjoyed my first year as managing partner because it has been a difficult one, and I tend to thrive on adversity. When it is a good market, everyone makes money. I would rather have a market that tests our mettle than one that is all one way. When the (Eurobond) market went down, we had a very interesting problem because we tried to trade it as you trade the US market and we found that the shorts were almost uncoverable. Things went into the deep freeze. Whether in Germany, in Switzerland, or wherever, people in the Eurobond market do not realize losses; they hold to maturity. They are like banks, and the mentality and the attitude of the universal banks, and some of the merchant banks who co-mingle functions, were not what we are used to in the US. It left us perplexed. But, initially, a benign market helped us. When the market receded we decided to remain in it, but we also decided that we had best do something to protect ourselves and run it a little more rationally, because fundamentally we were picked off on odd lots, asked to short difficult issues, and so we began editing, maturing and improving our efficiency.

Is it still a serious problem digging out bonds?

We were able to dig them out, but the shorts were not attractive because the yield relationships were way out of line and the market had not reached the US level of willingness to trade.

So what strategy did you form from that?

Prudence.

Does that still apply?

We are adopting the same attitude in Europe that we have in the United States, which is concentration on the liquid items, the high-grade issues, the large issues, the ones of which we have some understanding, that may trade back and forth. The exotica we cannot afford.

But you keep track of the ones you placed?

Our system, based on our US system, is moderately good. We understand a little better now where bonds are placed and what brings them back into the market again.

Who are the premier world institutional investors in the Eurobond market now?

The largest are the central banks, the state-owned banks, the very large multi-national banks, the largest domestic banks in the countries of the world, the insurance companies. We are not as knowledgeable yet as we might be about the self-administered pension funds. The savings institutions are less open. As far as the public goes, I know nothing other than what I get secondhand about what the individuals in Belgium or Italy do. That’s not significant. I believe that the world market continues to grow, those myths about little pockets of great retail monies will begin to be put into perpective, because inflation causes the number of money units to rise. The emerging investment pattern of great complexity is the cross-market in which investors move into different currencies and different quasi-indigenous markets — that is moving into the US market or into the Japanese market or into the Dutch market, or the German market, or whatever.

On an everyday basis, are the American pension funds finally beginning to get more interested and more aggressive about investing overseas?

There is no question that it is happening, but slowly. The flow of funds is still toward the US. But it is very important because it is another service, from my point of view, that Salomon Brothers can provide. You know, a great many European merchant banks and universal banks are constantly coming over here to solicit the US institutional market. It started in equities. That is where the relationships are. But now it is broadening into the bond market. For example, we do a fair amount of business outside of the United States in equities in indigenous markets. It is not something that we publicize a great deal because it is not a high-profit business. It is small, but it gives us some sense of relationship with our confreres in those markets. It is nice to be able to give business to a bank in Holland, or in France, because of the real reciprocity which is very important to our business. Banks should relate back and forth. The relationship between merchant banks, and the US investment banks around the world, and the universal banks, and the US investment banks, has a long way to go.

|

Gutfreund on his own time |

|

The Bawl Street Journal had a very nasty crack about your outside interests. Do you live, eat and breathe this job? Frankly, I was surprised at that because it totally lacked foundation. No, I don’t. I work very hard. I like working. But my outside interests are really quite substantial. I am on the board of the college where I chaired the finance committee for a number of years. In the last 10 years I have only missed one board meeting. I am executive vice president of a major philanthropic hospital in New York, a voluntary hospital, and have been for a number of years. I have been, and still am, on the board of the New York Public Library and serve on committees there; chairman of the Forty-Second Street New Development Plan, which is an urban new development plan; treasurer of the Jewish Communal Fund in New York; and a trustee of the Federation of Jewish Philanthropies in New York. Without my outside interests I would not be a very good banker. So anybody who thinks of me as totally involved in the office is wrong. I am a moderately private person so I don’t seek to advertise my outside interests. I do not impose them on my associates. However, I have encouraged my partners and senior associates who have benefited from some of our affluence to give something back to the communities in which they live, besides their taxes. So you will find now amongst my partners that, whereas a generation ago we had less of this voluntary civic service, we now have a number of partners who serve on the boards of major universities and colleges, and do a great amount of civic good work. This is for two reasons. One is that it’s good for them and the second is this is a very insulated business. One’s judgement can only be as good as one’s breadth, do you disagree with that? Not at all. My job is to maintain and to run this place well, but I have been involved in the theatre and know what is going on in the world of the arts and care very much about that part of my life, too. Your 7.30 working breakfasts are legendary, internationally as well as domestically. Is that where most of the policy decisions are made and where you do most of your deals? I am a morning person. I like to get up early and I think better in the morning. That is why the breakfast meetings suit me. I always feel that I am fresh then. What time do you get up? Six or 6.15. As you get older, unfortunately you learn that you do not need ten hours sleep each night. I can also have a session from four to seven or eight or nine o’clock. The strange thing that I find, even at my age, is that if it is an interesting discussion, and it is a complex problem, then that is what I care about most. You are not a member of any of the exclusive clubs, such as the Bohemian? No. The priority has been to make Salomon as efficient as possible. One can always join a club. You wouldn’t find it intellectually stimulating? I would. I like to talk to people. But there is not enough time in the day. Frankly, I spend a lot of energy here. On weekends, I hopefully take some time to myself, play tennis and see my children. But you do work at weekends as well. For example, this weekend is to be a working weekend. I shall have all day Sunday, as well as Saturday afternoon and evening. I frankly do not work beyond my capacity. In other words, if I am tired over the weekend or I want to go home, I go home. I just turn off. I am not compulsive about work, or about money, so it is not a big difficulty. The one thing I would hope over the next few years is to be able to have more time to talk to people, to learn something, to be able to sit back from the business a little, to be a little more removed from the day to day happenings. I interfere less at Salomon Brothers and I am less involved with individual transactions than you would think. |

Who do you admire among the international banks?

Hopefully having friends all over the world, two or three anyway, one has to be very careful in answering that sort of query. The Deutsche Bank is a very impressive institution. It is impressive, despite its great size, both in footings and in personnel, because you can deal on a person-to-person basis with a number of very able folks. To me that is the great test. In other words, it is like dealing with the Bank of America, with whom we deal in the United States. I am impressed that you can get decisions and that you can be dealing with somebody who is very competent. That is the great test. Fortunately for me, it is still something of a people business. So those people with whom you do business and whom you like are those whom you would favour. We have two or three friends in Sweden who are very nice. They are not the biggest banks in the world but they are professional and we deal with them on those terms. We have some very impressive acquaintanceships in the UK.

Who would you single out there?

I would be loath to single out. Warburg’s is excellent. We have done some wonderful professional trading with Hambros — NMR is excellent.

Which banks would I pick in France? In addition to Banque Nationale de Paris, Crédit Lyonnais and Société Générale, I would say Paribas is a great private bank.

You rank high in the US in negotiated Securities, competitive offerings and private placements. Where can you go from here?

Looking ahead requires discernment. We have always been very strong in the public utility area. What we have attempted to do is broaden our services and relationships in the industrial area. You have to look at your client base and you have to consider their size and evaluate the effort/reward ratio. Even with spreads diminishing, can you, with the variety of services you sell, carve out a good business? Just as Merrill Lynch and E.F. Hutton diversify in the selling of different products at retail, whether it be money funds, or stock funds or bond funds, insurance, or housing, so we are attempting to determine the future needs for our services among corporations in America, which we believe would be valuable to our clients overseas as well. Our profession is in the ability to deal with them — bankers’ acceptances, Treasury Bills, CDs, fund management, whatever. The other important area of growth in the US is in the burgeomng mortgage market which is turning into a securities market.

You went into underwriting those mortgage securities when the debt agencies would not even rate them. Why?

Because underlying it all, what we were doing was to buy Federal credit. They were guaranteed by agencies of the US government. The rating did not matter. Liquidity was the key there, and there is still a large differential in the rate of return offered to investors in the mortgage market as opposed to the conventional bond market. But that will narrow in time. That is a fascinating area of business to me because we are innovating almost weekly on that. Keep in mind that fewer firms do not mean less competition. It means that the spreads have driven people out of business, so that your professionalism is absolutely vital. The final area is the financial futures market and the commodities market.

Do you see yourself getting into that in a big way?

As we understand it, there is no question but that the rest of the world knows that their particular currencies may not be forever. We thought the dollar was forever. We saw no need to balance our risk, to diversify our own portfolio. Tonight and tomorrow we shall be meeting with our partners for a weekend briefing on financial futures. One of the problems about such a briefing is that we do not want everybody jumping off immediately afterward thinking they are ready to trade futures. We want them to understand better what is happening in the market place. It is terrible to be marketmakers, as we are, and not to be able to understand instantly the new forces that are moving us about. Intellectually, attempting to understand better is what is great.

|

Gutfreund on his reading |

|

How do you keep in touch around the world? What do you read? Every morning I read The New York Times fully. I read The Wall Street Journal. I read a lot of our in-house news systems. Among publications: I read your publication; Business Week I find myself watching every week; The Institutional Investor is like a people magazine which I read with interest; I read the London Economist irregularly; I like it. The Financial Times of London I read irregularly but I like it. I read probably a couple of books a week. A variety. Business books? Not really. Just light reading. Last night I was reading a book on commodities. It was dull. But that is not usual? No. I’ve just started a new book. It’s a novel, called Sophie’s Choice (William Styron). I have some friends in the publishing business and I get sent a fair number of books. When I was in prep school I thought The Fountainhead was great. That’s 30 years ago. I don’t read much business philosophy. It doesn’t mean anything to me. And I really don’t particularly enjoy business books. I am struggling with The Education of Henry Adams, which I bought again, it’s a book by a strong feminist which I find interesting. I often read two or three things, and if I am tired I will read a novel. I read on planes. If I am tired I read light books, and if I am not tired I read more serious things. There is an enormous amount of informational material which is produced here in this firm. Jim Wolfensohn demands in-depth briefing books on our clients and I have to read them. |

And who is to do the briefing? Do you understand it well enough to brief your partners?

I hope we can do better than that. I understand it. We have spent months on it. But, fortunately, we have some young people who are a lot better informed than I, who have been working full time at it, who are not only available, but are pretty good, We could not depend on me to do that, or any of the other senior partners.

So what strategy do you think you might form as a result, or is it too early to say?

The strategy has already been formed. We are just responding to the world as it exists. How we will adapt it to our own uses is what is important.

That’s what I was getting at.

Adaptation — that is number one, how will it help us in our market making role for institutions around the world. Number two, when we can handle it properly, do we want to merchandize it for them? Or do we just want to use it as a device for ourselves? I can assure you if it is a good device for ourselves, we will not be allowed to keep it.

Who will stop you?

The institutions will demand that, as part of our service, we educate them in the same business, and then they will begin to compete in it.

You have a strong intellectual interest in futures. Why does it fascinate you?

Futures are a very difficult and interesting problem because they do not really have anything to do with the capital raising mechanism. Futures are a speculator’s dream. It is Las Vegas, or Atlantic City, or Monte Carlo. I worry about that, because the distortions, the aberrations they can cause in the marketplace are extreme. We saw this first in the securities business in equities, and in options. The commodities market and its relationship with the cash market is akin to atomic energy when we have been used to fossil fuels. It is dramatic. And it is not necessarily good. I am sure that there are central bankers wondering about it in Europe. We have not had the great public debate in the States on the subject. Again a crisis will cause that.

Can you see yourself going into commercial banking? Lending money, taking deposits?

It is not inordinately appealing. I could see us in certain aspects of trust banking, management of money, where we bring some expertise. There, too, historically we have avoided it because of a conflict with our clientele. But as our clientele begin to spread their wings into the private placement market and the commercial paper market, I do not really feel as totally inhibited as I once might have been. What aspects of commercial banking and trust banking we go into will depend upon our team’s view of the expertise we can deliver. If we can deliver a first-class product, I would not hesitate to compete head to head.

Does it irk you that there are still a lot of companies in the Fortune 500 who are not your clients?

That’s a myth. We are not identified as the primary banker to a number of corporations in the Fortune list, but we have a surprisingly deep and broad transaction relationship with many of them. Because we do not appear as the lead banker on the tombstone when they raise their $200 million does not mean that we do not have very deep relationships. If you were to go over the first hundred, I could discuss with you on a case by case basis where there are very significant relationships.

Is visibility important to you?

Visibility attracts business, so it has to be important. I would be foolish to ignore it. Would we like to be the primary bankers to General Motors? If we were the best people qualified to do it, yes. We may not be the best people for that mammoth. For example, AT&T is the biggest enterprise here and we are one of the three bankers to them. One of the interesting things — to toot our horn a bit — is that with the regulated industries, the utilities, and the municipalities where the best price and the best service are the decision points, we have done very well. The object now is to continue to move forward and have the corporations who are going through the same professionalization process that we are, recognize us on our merits and accept us as the fine people we know we are. And that is coming along. It really is not the most important thing. After all, if we can represent the United Kingdom, the Government of Canada, Norway, Sweden, Finland, Brazil, Venezuela…

And be an adviser to SAMA?

We are not an adviser to SAMA.

You’re believed to be.

Well, we are not.

Do you see the role of advising central banks and governments as something that you would like to get into?

I think it could be interesting for a period of time.

You grew up in an era of sound money. You built up your business in an era of relatively sound money. What impact on your psychology does a dollar that is depreciating faster than it has ever depreciated, with the highest inflation for 28 years, and a lot of doubt over the Administration’s capacity, have on your thinking?

If you are asking that question of me as a citizen, the inflation in this country is the major concern for all of us. Its whole nature is different from either the inflationary outburst following the end of World War II or the one during the Korean War. And unless it is reined in by the most strenuous effort, it could be a forerunner of serious problems. If you are asking the question of me as an investment banker and marketmaker, we have to adapt to survive. The developments that you have mentioned did not come about overnight. To a certain degree, they were well heralded to those of us in the business. My thinking for the past few years has been that we would have to diversify our risk. One way to accomplish this, in market making, is by changing around the components of our book. For example, our bonds and stocks denominated in other than dollars are not reconciled nightly into dollars. The variables — comparative interest rates, inflation rates, and currency values — are more important now in the relative pricing of assets. But, we have always known in this business that the only certainty is change, and change creates opportunity. These new instabilities with which we have to deal are also important to us because they obviously impact the capitalization strategies of our investment banking clients and the liability and asset mix of the commercial banks around the world who are very important to us.

What are the corporations going to do about it? They are not going to diversify their liquidity, high though it is, into other currencies, are they?

No, they are not. What they are attempting to do, philosophically, is to build capacity in terms of plant, in terms of expertise, that keeps apace of inflation. The values of currencies constantly depreciating has made the merger and acquisition market, the buying of assets around the world. The one thing that you do not want to remain in long is currency. You want to get into real assets. This impacts our business.

Do you sit in the Room because you want to be seen there?

I want to be accessible. It is very important in our business that all our senior management be easily accessible to our people, as well as to our clients and customers.