|

|

The continuing push towards technology in payments and cash management can create the impression the move is being driven by the demand of the users. The results of the Euromoney Cash Management Survey 2017 suggests this is not the case.

This year, with the support of Deutsche Bank, we have gone back to the 2017 data to uncover the interesting trends in the underlying data. The survey recorded 4,695 responses globally from the financial institutions (FIs) and non-financial institutions (non-FIs), giving a comprehensive overview of a year in treasury. In each of the qualitative categories, a respondent may assess up to three providers and the editorial/service priority sections are not compulsory but have between 70% and 80% completion rates.

Results from both the FIs and the non-FIs show strong parallels in their opinions and expectations on the products and services they are offered, and crucially, where these expectations are falling short.

|

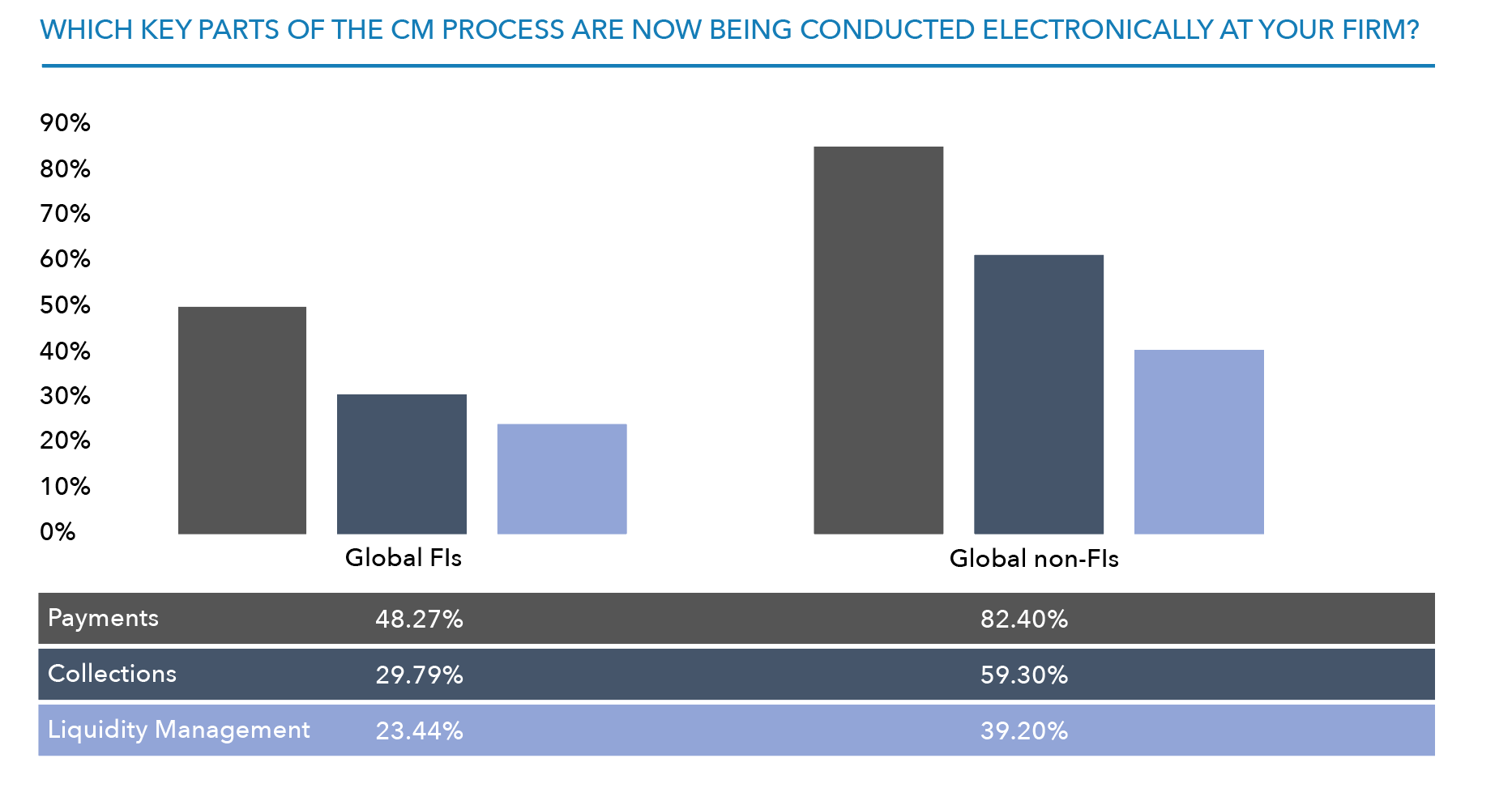

While banks invest huge sums in updating their cash management platforms, is this something their customers actually want? The survey indicates that the only area of cash management strategy that is now being conducted electronically in significant numbers is payments – global FIs recorded 48%, while non-FIs saw a massive 82% of respondents stating they are conducting payments electronically. With the proliferation of digital payments methods, from Swift messaging to faster payments, this number is not a surprise.

When considering other aspects of cash management services that have been conducted electronically the numbers fall far shorter than what was seen for payments. Collections come in with 29%, and liquidity management at 23% for the FIs, and 59% and 39% respectively for the non-FIs. The options available for the digitization of these services does not seem to be reaching the required standard to encourage greater levels of adoption.

Mobile capabilities might be something that banks are keen to develop, but according to the survey it would seem treasurers do not need it, and the actual quality of the service when available is poorly rated. Mobile capabilities were the second lowest-rated category of service priorities in the global responses of the non-FIs, and ranked last for the FIs.

Fintech services

However, one major theme that really stood out from the results was the use of services from fintechs. For the ‘Have you used a non-banking financial company (eg AliPay, PayPal) for any cash management services?’ question, both the non-FIs and the FIs gave incredibly close responses. Globally 88.8% of non-FIs stated they had not used their services, and 89.3% of FIs gave the same answer. While the banks worry about the fintechs coming to eat their lunch, the reality is that even the biggest names in fintech payments still have some distance to cover to get anywhere near the dining table.

Although the current outlook for fintech adoption does not look too promising based on these results, there is the potential for change. Asked about their future plans, 35% of global non-FIs respondents stated they would be very likely or likely to use non-banking financial companies in the future. The FIs responded even more strongly, with 41% stating it would be a consideration. Even if the institutions are not yet using these services, there is clear interest in what they could do in the future.

So what is holding them back? Treasurers are risk averse, so being a first-mover to use new technology may not be in their nature. With limited capacity, research into new technology may represent a use of resources they simply do not have to spare. Instead, they are looking for trusted providers to lead the way on the services they need.

Service quality

The survey points more towards the quality of the service being provided, rather than the products themselves, and this has the greatest bearing on how successful a company considers their cash management provider to be.

As the respondents may not be receptive to the latest technology, the competitive advantage seems to be found in the personalization of the service. In ranking the importance of services, both the global FIs and the non-FIs list the speed and quality of response to enquiries and the overall performance of the dedicated manager as the two most important factors. Furthermore, both also list the overall relationship with the bank among their top five priorities.

However, these services might not always be meeting expectations. The results of the qualitative survey showed services were among the lowest-ranked offerings. For some banks, this should be setting off alarm bells. Especially considering when asked ‘How many cash management providers are core to your operations?’ in the 2016 survey, only 17% of FIs and 31% of non-FIs stated they focused on one provider. However, in the 2017 survey, the numbers had shifted dramatically. Now, 41% of FIs and 52% of non-FIs have consolidated to one cash management provider. All the other results for the number of cash management banks used showed a downturn, suggesting a trend that is playing out internationally to reduce the number of providers used.

In total, 76% of FIs and 80% of non-FIs stated they had changed, added or removed a cash management provider in the past 12 months. And when looked at in relation to the results above, it seems likely that the majority of these will have removed providers.

Provider evaluation

The survey also indicates that a high number of both groups surveyed had decided to reevaluate providers after issuing a request for a proposal (RFP) in the last year – 58% for FIs and 57% of non-FIs. However, this does not necessarily mean the RFP is perceived as integral to the process. The survey results showed that not only were RFPs rated low in the terms of the importance of services, they were also considered to be of low quality when given.

Rather, the issuance of the RFP is a clear indication of intent to move or change providers, but in itself is not what could make or break the decision to move to a particular cash management provider. It would seem the request for proposal is just that; an indication of the interest and capability of the institution to meet the organization’s needs. What really wins the business is being able to demonstrate that the claims, from the quality of service to business understanding, will be carried through into day-to-day operations.

The continued need for a trusted partner

For now, treasurers are looking at technology as a secondary consideration. Yes, it is on the horizon, but their focus is on the road in front of them. They need reassurance that their bank is giving them a premium standard of care. Banks that achieve this are in a strong position to support their clients as a trusted partner during the journey into the digitization of their business.

Further results analysis

|

|

Euromoney’s Cash Management Survey 2017 further questioned respondents to gain insights into their specific needs and priorities on the services they were receiving. Respondents also had the opportunity to rank their services providers. Download the complete report below.