|

| Author |

|

|

|

Julia McKenny Head, Market Advocacy, Securities Services, Transaction Banking |

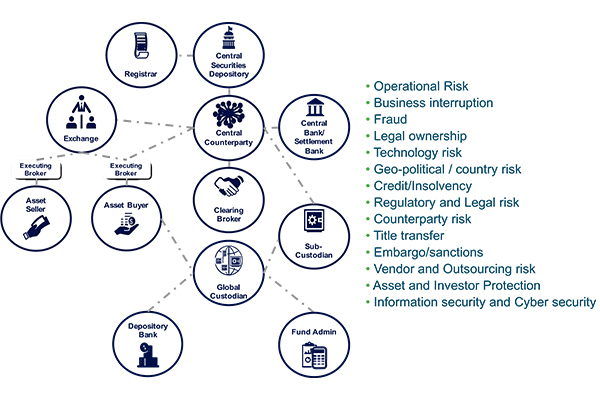

Despite the life cycle being seemingly simple it is complicated by numerous links and stages that are required and used and which often result in the higher cost of the service and the heightened possibility of risks and errors.

The point noted and discussed on the panel was that despite the risks being well documented(1), the question remained as to whether the process could be simplified for a less expensive, more aligned and overall enhanced outcome. And further, could this be done in the context of the current regulation? Post the various global health hazard’s headlined by Lehman Brothers and Madoff incidents, regulators globally were prompted to introduce various reforms (among them asset safety regimes and strict liability requirements on depositaries under UCITS V and the Alternative Investment Fund Managers Directive (AIFMD), European Market Infrastructure Regulation (EMIR) and Markets in Financial Instruments Directive II (MiFID II) and the Central Securities Depository Regulation (CSDR)) impacting securities services transactions. Hence the valid question of the ability to have an enhanced agile process within a web of global regulation.

|

| Figure 1: Overview of the participants in the Long Custody Chain |

Risk management – short-term thinking

Regulatory reforms have addressed the various risks in the custodian chain. Post-crisis reforms have resulted in widespread de-risking in financial markets. In securities services, the introduction of the above mentioned regulations have formalized several risk mitigating provisions in the securities transaction life-cycle and at the infrastructures facilitating the processes.

These regulatory initiatives, further enhanced through harmonization, bring about at the same time market efficiencies. EU-wide harmonization of securities markets is being developed through schemes such as Target2Securities (T2S), and it will become further embedded provided there is pan-EU agreement on the Capital Markets Union (CMU).

Similar efforts to streamline securities processes are also being made in West Africa (Economic Community of West African States), East Africa (East African Community) and the Gulf Cooperation Council (GCC) to create aligned market standards and cross-border harmonization in areas such as dual listings of securities and CSD/stock exchange connectivity. (2)

In addition, efforts to improve the ability to recover client assets have been encouraged and explored, and discussions continue on the viability to achieve greater asset protection through the creation of segregated account structures right down to the CSD level. While driven by the belief that this model offers greater investor protection over omnibus accounts, recent post-Lehman discussion questioned this with the industry view now somewhat resolved that segregated account structures add significant costs to transactional processes without the ultimate desired outcome of greater asset protection. (3)

To that end, risk mitigation tactics have not solely been the result of regulatory reform, but also industry efforts. Due diligence on sub-custodians by network managers is clearly evolving and becoming more standardized via work being undertaken in industry associations such as AFME (Association of Financial Markets in Europe) and the questionnaire (DDQ) which we are seeing becoming a recognized benchmark. The DDQ allows network managers at global custodians and broker-dealers to obtain answers to standardized questions seamlessly, giving them more time to conduct reviews on some of the more bespoke issues at their local providers.

Such efforts globally – driven by the industry and regulators – will help bring about greater efficiencies and minimize risk for the beneficial owner in the short term.

Looking through the crystal ball and a proposed future state

Identifying solutions and efficiencies to the risks recognized in the custodian chain which also stand the test of time, will be critical. The ideal fix would be to start by shortening the securities settlement chain and many are suggesting that technological innovation will play a key role. The question is how much of a role can it play. While Standard Chartered is assessing the various possibilities, here are some preliminary thoughts and views:

• Many in the industry believe strongly that the impact from technology is fragmented, isolated and not global. Others believe that it will not occur on their watch and that the status quo will remain. There are some who however have grasped the future state model as being a revised and digitalized phenomenon. This was a strong theme at the panel discussion.

• Of all the disruptors, blockchain or distributed ledger technology (DLT) is likely to have the biggest role in disintermediating and simplifying or shortening the custody chain over the next few years. Much of this change is likely to occur firstly in emerging markets which do not have CSDs or CCP infrastructures and are unrestricted by legacy technology.

• A report by Allens Linklaters projected organizations could save between $11 billion and $12 billion by cutting settlement times and reconciliations.(4) In an industry that is under severe cost pressure, such savings would make a huge difference. Market participants such as Australia Securities Exchange (ASX) have leveraged blockchain technology to make improvements to its CHESS system for equity clearing and settlement, and it is unlikely to be the last.

Blockchain development is obviously a potential answer to risks in the securities world, but implementing such new regimes often comes with their own price – new unknown risks. The Linklaters paper highlighted, and it seems that the industry would agree, that investors tend to be conservative to whom they entrust savings and finances to, and this is certainly true of the custody safekeeping securities services world. Trust and the demonstration of it will be the key requirement for digitalization. (5)

In an environment where cyber security is now a systemic risk with regulatory focus, end investors require assurance that new technology is tested, trusted and safe from external hackers and confidentiality is of key concern under data privacy laws – blockchain and ledgers must be ready and prepared for the challenge.

Addressing these issues will require industry and regulatory collaboration to ensure technology risks are managed and costs are not driven up for the end user.

So, what is the solution?

In order to recognize and implement robust solutions, we need to identify the core problem. That propels the next question as to whether the foundational processes of securities services actually need changing to become more economical and to address the newfound risks in today’s markets. As noted, reforms such as asset safety measures are assisting and while these schemes will fortify the industry against immediate challenges, they will not place the industry in the best and most efficient position for development and progression over the next 10 or 15 years.

For custody to withstand this longer-term transformation, it must reform itself. This means firstly accepting that the custody model needs to change and that traditional services will increasingly be digitalized. Technologies such as blockchain are being implemented and assessments are being trialled in various operational lines. Once risks of the technology are clearly defined, and guarded against, it is inevitable it be unleashed onto the broader more global community. This inevitable change will happen on my watch. It is time to start to assess and consider what this means.

(1) ISSA – Inherent Risks within the Global Custody Chain

(2) See ‘Africa Regulatory Reform: The State Of Play’ Standard Chartered Paper on harmonization and regulatory reform in Africa

(3) ISSA – Inherent Risks within the Global Custody Chain

(4)Allens Linklaters – Blockchain Reaction

(5)Allens Linklaters – Blockchain Reaction

About the Author

|

| Julia McKenny |

|

Euromoney and Standard Chartered will be running a series of webinars on securities services. The next will be ‘The fight against cyber crime in financial services: how prepared are you?’ on September 26. Find out more.

|

Disclaimer

This material has been prepared by Standard Chartered Bank (SCB), a firm authorised by the United Kingdom’s Prudential Regulation Authority and regulated by the United Kingdom’s Financial Conduct Authority and Prudential Regulation Authority. It is not independent research material. This material has been produced for information and discussion purposes only and does not constitute advice or an invitation or recommendation to enter into any transaction.

Some of the information appearing herein may have been obtained from public sources and while SCB believes such information to be reliable, it has not been independently verified by SCB. Information contained herein is subject to change without notice. Any opinions or views of third parties expressed in this material are those of the third parties identified, and not of SCB or its affiliates.

SCB does not provide accounting, legal, regulatory or tax advice. This material does not provide any investment advice. While all reasonable care has been taken in preparing this material, SCB and its affiliates make no representation or warranty as to its accuracy or completeness, and no responsibility or liability is accepted for any errors of fact, omission or for any opinion expressed herein. You are advised to exercise your own independent judgment (with the advice of your professional advisers as necessary) with respect to the risks and consequences of any matter contained herein. SCB and its affiliates expressly disclaim any liability and responsibility for any damage or losses you may suffer from your use of or reliance on this material.

SCB or its affiliates may not have the necessary licenses to provide services or offer products in all countries or such provision of services or offering of products may be subject to the regulatory requirements of each jurisdiction. This material is not for distribution to any person to which, or any jurisdiction in which, its distribution would be prohibited.

You may wish to refer to the incorporation details of Standard Chartered PLC, Standard Chartered Bank and their subsidiaries at https://www.standardchartered.com/en/incorporation-details.html.

|