Equities have experienced high volatility since May when the Federal Reserve first hinted it might start shutting down the flow of US treasury purchases, which have helped to power capital flows to emerging markets since 2009.

The main global index for emerging market equities, the MSCI EM index, is down 6% in the year to December 17, but remains far above the lows seen in May and June as many markets have recovered large chunks of the losses they sustained. The index trades at around 10 times earnings, compared with 16 in 2008, 15.3 in 2010, 10.3 in 2011 and 12.6 in 2012.

Analysts say this year’s correction could sow the seeds for a modest pick-up, based on the bullish view that the market is now accustomed to tapering, amid hopes the Fed makes clear the curtailing of asset purchases will be a prolonged process conducted in small steps.

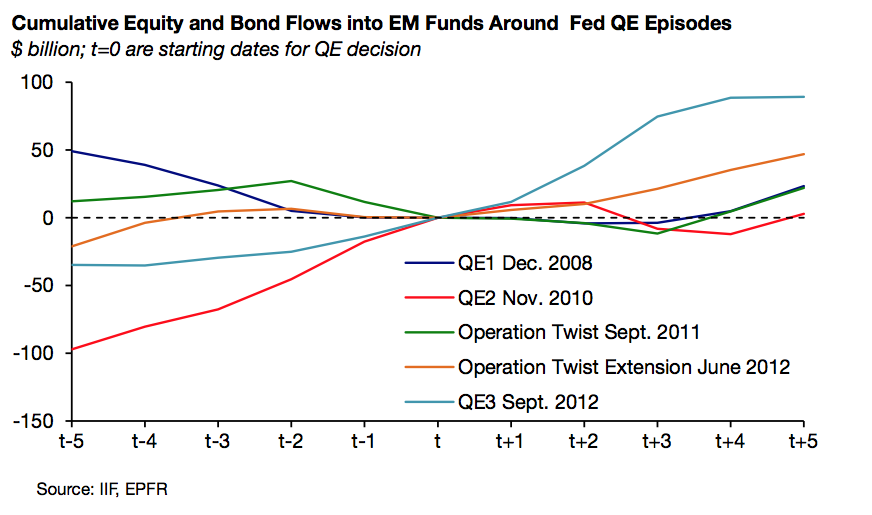

|

| Source: IIF |

Differentiation is likely to continue in 2014. As foreign investors scrambled to liquidate their investments, stocks tanked and capital outflows wiped as much as 20% off the value of some currencies, such as Indonesia’s rupiah. But with investors starting to focus much more on the underlying economies in expectation of higher borrowing costs, a small number of emerging markets, mainly emerging Europe, bucked the rout. Stocks have posted double-digit gains year-to-date in Latvia, Estonia and Lithuania, which also saw its currency gain 4.4% against the dollar. Poland’s WIG Index is up 7.3% year-to-date and the zloty is up 2%. After reaching dizzy heights in June/July, the Korean won heads into 2014 with a 1.2% gain. Vietnam’s Ho Chi Minh Index posted a massive 27% gain.

Other markets were patchy, but held their own: Russia’s MICEX Index is up 4.5%, but the rouble is off 8%. South Africa’s Top40 Index is up 16% and Malaysia’s KLCI Index gained 13.3%, but both currencies depreciated. The Philippine Composite Index is 4.3% higher this year after surging 20% in the first five months, but the peso has not kept pace, losing 7.3%.

“I think as we move on from the tapering stage what it means for EM is that we’re not going to be in this risk-on, risk-off cycle, or see such high correlations,” says Tim Dingemans, portfolio manager at North Asset Management. “A lot more differentiation is going to be the theme that’s going to make a real difference to how people get involved in emerging markets next year.

“That will bring back the value in studying what real interest rates are, what’s happening to the current account, is there a budget deficit or surplus, how big are the reserves, and the outlook for inflation. Depending on what those parameters are doing I think the differentiation across the different emerging market countries will become much more pronounced.

“That couples in with emerging markets becoming less of a credit trade and country specifics becoming much more important. So you’ve got the issue of Fed tapering and trying to get rate normalization back and evolving EMs, working together.

“Clearly there are countries that are still credit trades – Nigeria, Argentina, Venezuela – but the Polands and Koreas are not. So people will look at what are the ‘terrible five’ [Brazil, India, Turkey, South Africa, Indonesia], but the ones with twin deficits are clearly more vulnerable. But if some of those countries can show they can get on top of the issues and start to begin to address what’s causing those problems, then they might do well during the year.’’

Dingemans says heavy outflows of flightier money in the second half are being counterbalanced to an extent by global investors continuing to increase their allocations to EM, stickier investors like US west coast money, and domestic pension funds and other domestic investors.

Outflows from EM equities have picked up again recently. Data from EPFR Global show investors pulling money from EM equity funds for seven consecutive weeks till December 11, exceeding outflows from bond funds. In the week ended December 11, equity fund outflows hit $1.95 billion.

Cumulative net redemptions from equities funds since the end of February have now reached more than $42 billion.

The sell-off is not just related to tapering and worries about a stronger dollar and how EMs with large current account deficits will finance those deficits in the face of higher borrowing costs. It is also a reflection of the reappraisal of EM growth, with significant downward revisions of growth over the past two years.

“This year hasn’t been seen as the one-way bet that it’s probably been seen as over the last four years, or 10 years,’’ says Stuart Culverhouse, chief economist at Exotix in London. “But that’s not to say that this interest will not be renewed. If Fed tapering is priced in and the impact is not going to be as disorderly as this year, global growth is picking up with the US economy and the EM slowdown may be over, according to IMF forecasts, then maybe we’ll see a renewal of inflows next year.’’

EM secular growth might now be reasserting itself. The IMF forecasts emerging market growth will accelerate to 5.1% in 2014, up from 4.5% this year, driven largely by EMs across Asia, although the figures are downward revisions from earlier in the year.

“The upside potential for emerging markets has always outperformed the downside corrections that we’ve had over the last 20 or so years’’ says Peter Lowman, chief investment officer at Investment Quorum.

“So if you were an investor at the moment looking for perhaps a slightly riskier asset class to buy and you had a five-year time horizon, emerging markets just might be an interesting area to play on a fundamental standpoint.

“From a macro standpoint you’ve still got issues – headwinds like the tapering effect and probably a stronger US dollar. So short term it’s quite different and for these reasons we’ve lightened up on EMs this year in favour of developed markets.

“There is some value being seen in EMs, but I wouldn’t be surprised to see them drift back a little bit further over the next few weeks with events coming up like tapering and deadlines on the budget bill and raising the debt ceiling.

“It’s a difficult call when you look at EMs because you get contaminated with the big four [Brazil, Russia, India, China] which are getting close to being emerged into fully developed markets. Is there value there? Growth isn’t too bad still in those EM countries and of course they have some very big companies now in those markets – market leaders – that are very good quality companies with good, strong balance sheets. In this environment one should probably be having a look at those markets.”

Lowman concludes: “Next year will depend on market sentiment and whether investors grasp the nettle and say emerging markets have had a tough year, let’s put some money to work there and perhaps take some money out of a market that’s done exceptionally well in 2013.’’

|

|

| Source: IIF |