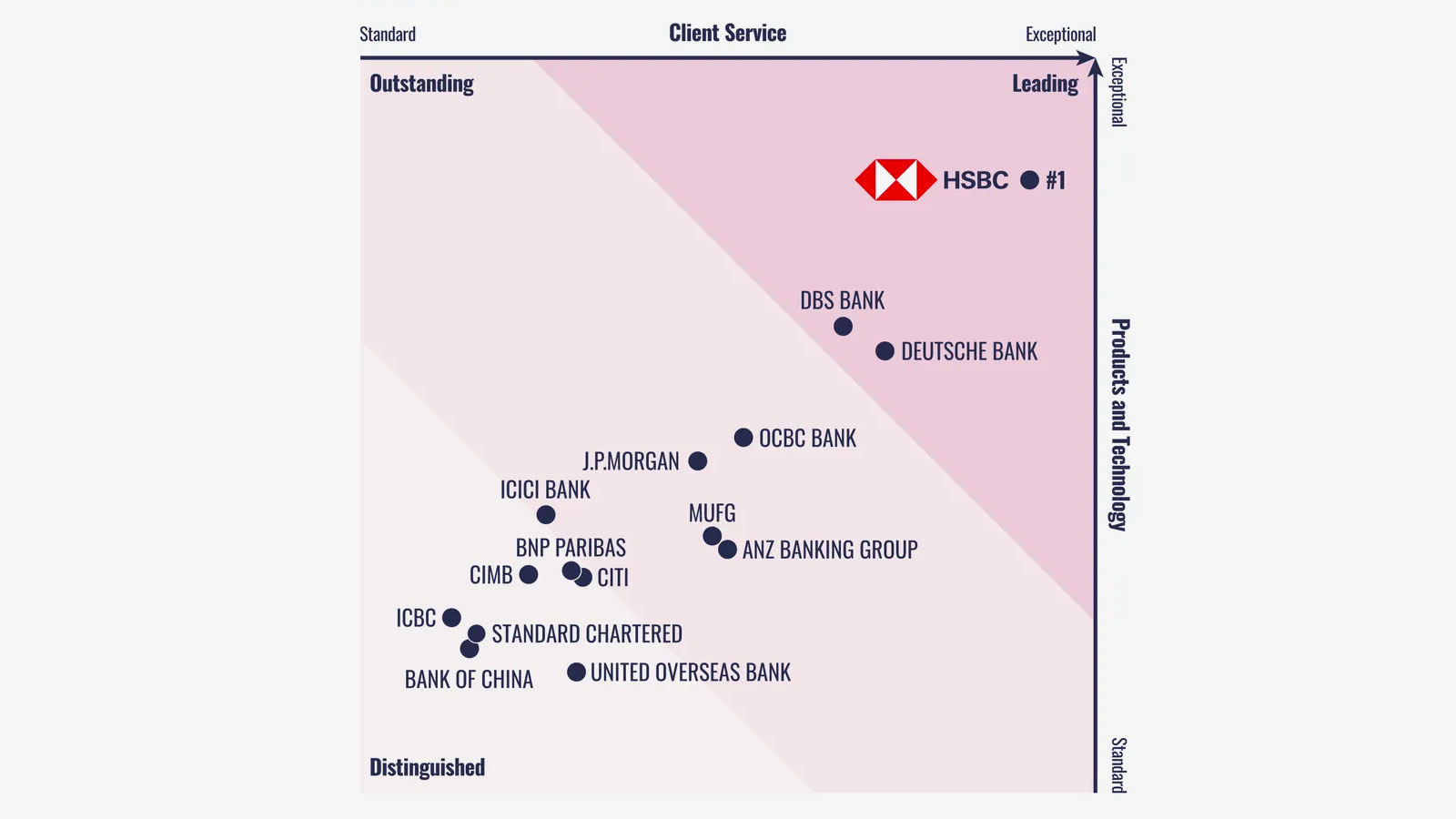

FURTHER READING

Euromoney’s cash management survey 2023 reveals that the percentage of respondents who currently have an application programming interface (API) into any of their cash management providers did not change this year – a halt after several years of growth.

While individual banks point to increased adoption, most agree that the market is being held back by the absence of uniform interfaces.

“Last year we organised a client advisory board,” says Philippe Penichou, global head of sales, wholesale payments and cash management at Societe Generale. “The theme was innovation and APIs, and it was quite interesting that of the 12 international treasurers in the room, only a few had implemented APIs.”

Penichou acknowledges that this low level of awareness could be down to the fact that APIs are assessed at cash-manager rather than corporate-treasurer level within organizations.

“However, our discussions with the treasurers who had adopted APIs, as well as with clients in other forums, revealed that wider adoption was being slowed by the need to deal with multiple different interfaces,” he says.

Ole Matthiessen, global head of cash management and head of corporate bank Asia Pacific at Deutsche Bank, refers to corporates being stuck in a holding pattern while they wait for standardization – including protocols and formats – or focus on solution-specific APIs such as account pre-validation.

“The limited readiness of enterprise resource planning and treasury-management service providers to fully integrate with the APIs of even major global banks, the slow progress of standardization initiatives, and the decision process of multinational companies to invest in API-based real-time use cases are some of the drivers of slower API integration,” he says.

“However, with the strong progress made across the market – including further API pre-integrations with treasury management and ERP systems – we anticipate adoption of APIs to increase. Once API bank connectivity and functions for real-time treasury become available out of the box within the large treasury-management and ERP systems, they are likely to cross over into the mainstream at an accelerated speed.”

The right direction

Infrastructure providers, regulators and industry forums have programmes in place to drive harmonization, explains Matthiessen.

“Initiatives such as the Berlin Group [a pan-European payments interoperability standards and harmonization programme], Swift’s setup of an API infrastructure based on pre-defined protocols and formats, and most recently the endorsement by the G20 of a roadmap to enhance cross-border payments are all moves in the right direction,” he says.

Eva Bueno, global head of cash management at Santander CIB, adds the absence of native support for mainstream enterprise software – including ERPs – to the list of factors holding banking APIs back.

Manish Kohli, global head of global payments solutions at HSBC, suggests that “the slowdown across the broader industry may be further attributed to early adopters of APIs having slowed as they look to define their future API/real-time payments strategy as part of broader transformation projects.”

Simon Kaptijn, director cash advisory and structuring at ING Transaction Services, reckons the slowdown in adoption could also be fuelled by the turbulent geopolitical and economic climate, as well as the slow initiation of a second wave of corporate adopters who need to contract third-party vendors to support integrations or investigate possibilities.

APIs are widely adopted across Asia, whereas they are used much less extensively in Europe

Philippe Penichou, Societe Generale

Growth in corporate-to-bank APIs remains in its early stages of adoption because of IT spending constraints due to the global macro situation, suggests Patricia Arvanitakis, global head of cash management at Crédit Agricole-CIB.

“It has been harder for treasuries to get the investment approved to roll out APIs for all kinds of use cases and some providers have left the market,” she says. “In Europe, a lot of corporates are waiting to see a strong push from their ERP providers and/or bank partners.”

Once integration to a particular platform is completed, additional customers can benefit from these embedded banking services without the need for additional development or integration.

“When clients connect directly to bank APIs, there is cost and effort for the client to complete the integration,” says Philip Panaino, global head of cash, transaction banking at Standard Chartered. “This can be a hindrance to those who may not have the skills or resources, hence embedded multi-banking platforms where clients can have more of a plug-and-play experience are where we see growth.”

Euromoney’s survey found that Latin American companies were most likely to have an API into any of their cash management providers. However, Penichou at SocGen says Asia is where the regional disparity is most acute in his experience.

“APIs are widely adopted across Asia, whereas they are used much less extensively in Europe,” he adds.

Kohli at HSBC agrees that clients in the Asia-Pacific region were early adopters of APIs for cash management and, following accelerated growth over recent years, Apac remains the region with the greatest interest.

“We are seeing the highest demand for our payment and account enquiry APIs in markets such as Hong Kong, India and China,” he says. “The UK has also seen demand for cash management APIs increase recently.”

In addition to solid growth in Hong Kong, Singapore, India and China, Standard Chartered is seeing growing demand in markets such as the UAE, Uganda and Kenya, as well as clients in Europe and the Americas connecting via third-party platforms, the bank says.