Alongside Lloyds and UBS, Nordea is the only large European bank likely to earn a double-digit return on equity in 2021. No other bank with more than €500 billion of assets will do so, according to analyst consensus compiled by Berenberg. And no other similarly large lender, including UBS and Lloyds, trades above book value.

Even in Scandinavia – a rare bright spot in European banking over the last 10 years – Nordea has been the best-performing bank stock over the last six months.

Many analysts now see Nordea’s first-quarter results, including a 21% rise in revenues, as a sign of what it will achieve as it catches up with smaller and more nationally focused firms, whose profitability Nordea previously trailed.

Under chief executive Frank Vang-Jensen, formerly CEO of Svenska Handelsbanken, Nordea is proving itself capable of more than just cutting costs.

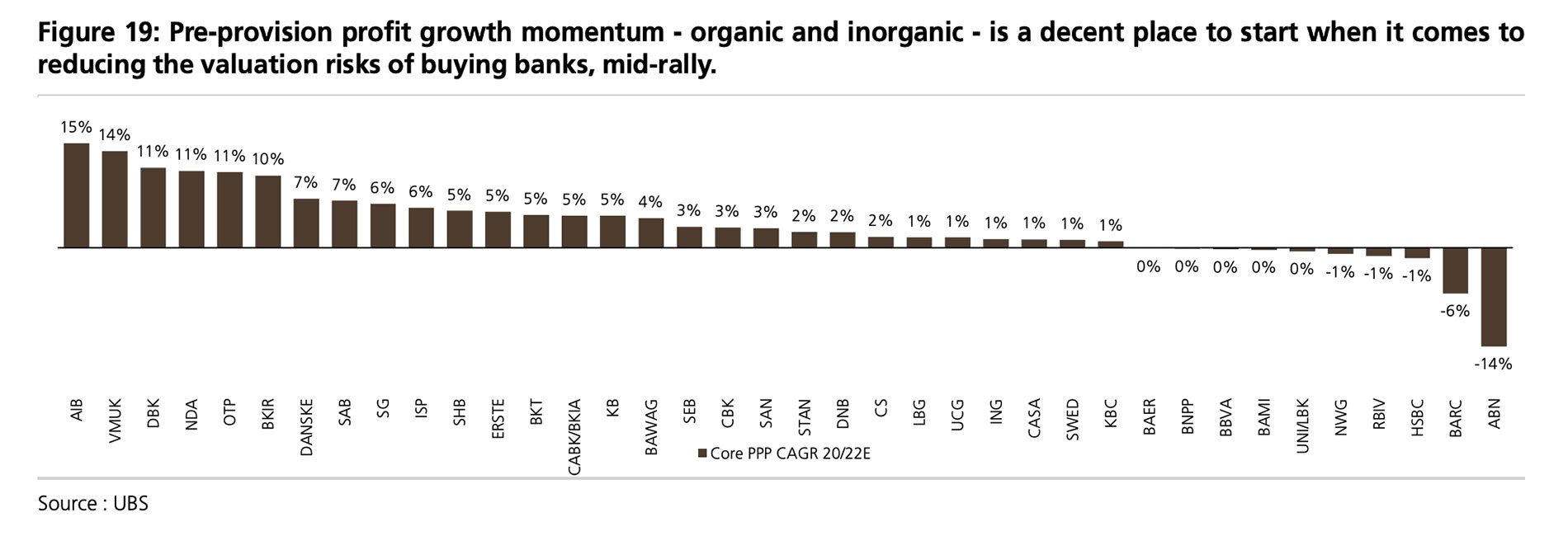

Over the first three years of this decade, UBS predicts that Nordea will show higher pre-provision profit growth than any other Scandinavian bank. This growth, moreover, will be higher than any other European firm of more than €500 million in assets except Deutsche Bank, which is coming back from much deeper trouble.

Attractive numbers

That is all much to the pleasure of Cevian Capital.

The Swedish activist investor took a 4.4% stake in Nordea in late 2018, spurring the 2019 exit of then chief executive Casper von Koskull, previously Goldman Sachs’ head of Scandinavia.

Nordea – the only bank to enjoy top-tier positions across the four main Nordic states – has since come close to surpassing Spain’s Banco Santander as the most cost-efficient big bank in Europe.

Despite negative rates, Nordea reported a 9% year-on-year increase in net interest income in the first quarter of 2021, largely thanks to replacing low-margin corporate loans with high single-digit growth in mortgage and small and medium-sized enterprise lending.

That has led to retail and commercial banking market-share gains across Scandinavia, including in Swedish mortgages, the biggest and most profitable part of Nordic banking.

According to analysts at KBW, the reason is the recent improvement to Nordea’s offering, especially compared with Handelsbanken and Swedbank.

Matti Ahokas, Nordea’s head of investor relations, tells me Nordea’s mortgages are no cheaper.

“In the Nordics, speed is of the essence at the moment,” he says. “We got our act together as the market started to pick up.”

Wealth and asset management is another part of the story. Nordea’s assets under management grew 33% in the year to the end of March – again, largely thanks to more focus on retail.

It has performed particularly well in the Danish fund market, where scandal-hit Danske Bank is languishing, and where all banks are lowering the threshold for imposing negative interest rates on depositors.

Rallies

Can Nordea’s good run continue?

US activist Elliot Management is pressuring Sampo to offload its leading stake in Nordea. Although that is not a comment on the bank, but rather a desire for the market to more correctly value Sampo’s core business, Nordea’s recent share-price rally should surely prompt the insurer to get on with it.

This year, Nordea’s share price has comfortably surpassed the level at which Cevian bought in. But Cevian shows no sign of selling. Nordea’s return on equity, after all, is still only 11%.

The fact that this is the same or slightly higher than pre-Covid shows it is doing better in some respects; even SEB, which is also gaining market share, is less profitable than it was two years ago. Yet Nordea is still a couple of percentage points lower than SEB or Swedbank.

Vang-Jensen has made some sensible decisions – steering away from areas of strategy to which von Koskull was more wedded. He has taken an axe to the corporate and investment bank, especially capital-intensive activities.

The task of making the biggest Nordic bank the one that is also consistently its best performing has only just begun

Organizationally, he has tried to end the committee culture for which Nordea was known, making divisional managers more accountable for performance.

Nevertheless, as new non-bank competitors emerge in Swedish mortgages, it remains to be seen how Nordea will fare once other incumbents regain their mojo, too.

Let’s face it, it is partly because of trouble among these rivals that Nordea would be gaining market share.

The Nordic money-laundering scandals of the late 2010s hit Danske Bank hardest, followed by Swedbank.

Danske separately suffered a mis-selling scandal in its fund management business in Denmark, among other embarrassments. DNB has had to manage the impact of Covid-19 on oil prices, as well as the distraction of a large local M&A deal.

Swedbank, however, previously enjoyed one of Europe’s best reputations for digital banking. Its management is determined to speed up service and regain lost share.

Likewise, Handelsbanken suffered an embarrassing U-turn last autumn when it said it would close almost half its Swedish branches. Its return on equity has fallen markedly behind other Sweden-based banks. But, like Swedbank, it has a much bigger market share in Sweden than Nordea.

Proof

Despite recent progress in rolling out a better pan-Scandinavian digital platform for its front office, Nordea has not yet fundamentally proven how, over the longer term, its multi-country operation can outperform these peers, which all have bigger shares at national level.

A cross-border spread is still most beneficial in corporate and investment banking, but a leading position in Scandinavia is by no means enough to sustain a full-service franchise nowadays.

By focusing more on retail, Nordea has provided some positive surprises lately. The task of making the biggest Nordic bank the one that is also consistently its best performing has only just begun.