|

|

| Illustration: Matthew Hollings |

One day next year, Stuart Gulliver will leave his office for the last time and no longer be an employee of HSBC. How will he feel?

“I’ll be sad,” he tells Euromoney. “But I will be proud.”

Gulliver has devoted his entire working life to HSBC. At the age of 58, he feels it is time to hand the baton of leadership to someone else. That successor will benefit enormously from the legacy that Gulliver and his long-time colleague as chairman, Douglas Flint, leave behind. Over the last six and a half years, under their leadership HSBC has gone through a fundamental restructuring.

That transformation has been under-appreciated and in some quarters barely noticed. The headline numbers certainly do not tell the story. Gulliver became chief executive in 2011. In the financial year before that, HSBC’s share price was around 700p, its return on equity 9.5%, and its underlying profits a little over $18 billion – and the banking industry was still feeling the full force of the financial crisis. The share price, return on equity and underlying profits are largely the same today.

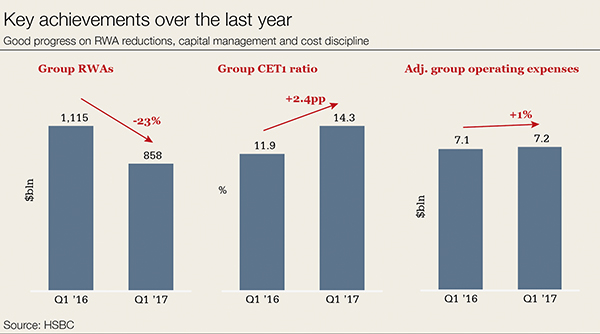

Here instead are the numbers to focus on. Since 2011, HSBC has shed $290 billion of risk-weighted assets, the equivalent of a bank the size of Standard Chartered. It has exited 97 businesses and folded its tents in 20 countries, continuing to serve customers in 68 countries today, down from 88 at the peak. A balance sheet that reached nearly $2.7 trillion in 2013 had come down to $1.9 trillion at the end of 2016.

This is not some half-baked attempt at shrinking to grow. It is a bank which, in the years preceding this restructuring, had managed to add $4 billion of annual costs with no revenue growth, that is finally getting a grip on its biggest financial problem, while at the same time controlling the defining threat to its continued existence: being used by criminals, tax evaders and worse.

Having set itself a target to cut annual operating expenses by between $4.5 billion and $5 billion, it is on target to achieve $6 billion to $7 billion of annual cost saves, even after investing at the rate of over $1 billion each year since 2014 in new safeguards against financial crime.

In 2012 the bank had 1,200 full time employees in compliance. Today it has 8,300, accounting for 3% of its entire staff.

Meanwhile, the total number of full-time employees has fallen, from around 300,000 in 2011 to just above 235,000 today.

HSBC, which did not take a penny in state aid during the financial crisis and which has always been conservatively funded as well as strongly capitalized, has bolstered these signature strengths to new heights.

It may have struggled to deliver its target 10% return on equity to shareholders (although it reported a 9% return on tangible equity in the most recent quarter), but as well as being a low-risk bank it has always been a profitable one, in every quarter.

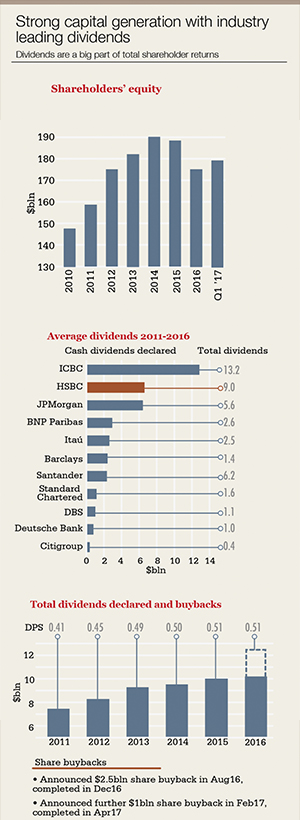

While other large global banks that were saved by taxpayers, and many that were not, cut or suspended dividends in recent years, HSBC maintained its own. It has paid out $56 billion of dividends since 2011 – more even than JPMorgan – while retaining sufficient earnings to boost its common equity tier-1 ratio to 14.3% and its leverage ratio to 5.5%. And since 2011, it has generated $20 billion in shareholders’ equity from retained earnings.

It has managed all this even though the very low ratio of loan advances to customer deposits – now at 68% and which the bank once talked of possibly capping at around 80% – which frees it from liquidity risk and shows it as still the destination of choice for customers to protect their savings, has become a drag on returns.

When interest rates stood at 3%, HSBC’s $1.3 trillion of deposits might bring in around $5 billion of revenue. Recently they have brought in next to nothing. The bank has been flying with one large revenue engine shut down.

Gulliver, Flint and their colleagues have achieved all of this under the cloud of a US deferred prosecution agreement (DPA) stemming from a period before they took control. The DPA has had an impact not just on morale, but also on the bank’s ability to win new business.

Most importantly, Gulliver has transformed the way this global bank is run. What was once a federation of 88 separate country businesses has become a much more coherent entity, with four global business groups, 11 properly resourced support functions and five regional divisions reporting to the chief executive and to the holding company board.

As that transformation now moves towards fruition, as the underlying earnings power of core businesses re-emerges, as investors regain faith in the value of the franchise, as its customers give HSBC more business, as the bank repositions for growth in Asia and sticks to its mission of financing cross-border capital flows and trade in a more protectionist world, HSBC is in a great place.

It remains to be seen how students of the bank’s history will eventually judge him, but it strikes Euromoney that much of Gulliver’s time at the very top will have been spent sorting out a mess of other people’s making: a banking group that had grown into a series of franchises, growing costs faster than revenues, with disjointed processes and systems that made it vulnerable to internal and external bad actors using it to avoid tax and move the proceeds of crime. And that he will probably never get the credit for what he did.

“The way I rationalize it is that I am privileged to have the stewardship of HSBC for seven or eight years. I may have joined this bank when I was 21 years old, but I didn’t found it. My family don’t own a big stake in it. I pick up the hand I am dealt and have to play those cards to the best of my ability. My task is to pass HSBC on to my successor in better shape than when I took it on. And I will be doing that, just as Mike Geoghegan handed it on in better shape to me than when he became CEO,” says Gulliver.

Does he in any way regret taking on the job?

“If I had known that the job was going to be this tough, I would still have taken it because this job needed doing and it fell to my generation of leaders to transform HSBC. I never lost my resolve that we were going about things in the right way. I’ve given my life to this company. I know its DNA. I know that 99% of people coming to work every day at HSBC come to do the right things by their customers and their colleagues. I have had some frustrations that we didn’t get much recognition for it. But I knew that I could transform HSBC without stalling it.”

Why? “Because I was sort of the ‘insider outsider,’” says Gulliver. “I had spent most of my career in global banking and markets.”

Biggest restructuring in 150 years

On the bright June day in London when Euromoney sits down with Gulliver, who has been at HSBC for 37 years, to discuss the shape of one of the small handful of truly global banks still left standing, his sense of history appears attenuated. He tells Euromoney: “I believe that what the group management board has achieved in the last six years is the biggest restructuring in HSBC’s 150-year history.”

|

|

Stuart Gulliver

|

It may sound a slightly grandiose claim. The business mix, after all, is still largely the same as when Gulliver took over. But the model for running it needed profound change. Gulliver had a ready and steady ally in Flint, who says: “For me the low point in my time here was the realization, which reached a crescendo in 2012 with the US Senate Permanent Subcommittee on Investigations’ report, that we had not understood that we were not being run to acceptable standards in many places around the world.”

Flint, the former group chief financial officer, became chairman of HSBC at the end of 2010 and has worked well with Gulliver, who became chief executive a couple of months later. While Gulliver transformed the running of the bank, the calm, considered and reassuringly Scottish-sounding chairman engaged in the public policy debate about the role of banks and bank regulation.

HSBC was hit by a series of reputational setbacks even after the senate report and the DPA, including revelations that its private bank in Switzerland had helped tax evaders in the mid 2000s. It even got a prominent mention in the Panama papers.

“The important thing is that the executive management team committed to fix what needed to be fixed and got on with that, bringing in new people with new talents without diluting the character of that leadership team. For the board, for regulators and policymakers, the key was to be comfortable that HSBC was headed in the right direction, with a management team capable of delivering,” says Flint.

The management matrix dominated by geography, which had served HSBC so well for so long, had left too much up to local subsidiaries. “The bank required more central control to analyze data that might reveal bad actors and needed root and branch reform to achieve that,” says Flint. “It helped that we did not have to redefine HSBC’s core mission, which has always been – and continues to be – to finance cross-border and cross-regional trade and capital flows.”

HSBC remains a global universal bank, one of a dwindling number. It has three main business divisions: a commercial bank (CMB) handling trade finance, cash management and payments for corporate customers and lending to them; a global banking and markets business (GBM) intermediating equity, rates and credit for investors, arranging debt and equity finance for issuers and advising on M&A; and a retail and wealth management division with high-street businesses in 36 countries, most notably the UK, Hong Kong and Mexico.

It also has a private bank, a much smaller global business and one that at times must seem more trouble than it is worth.

|

So, what, Euromoney wonders, is the single biggest and toughest change Gulliver and his management team has had to make?

“The biggest transformation has been moving HSBC from a loose federation of stand-alone businesses in which the country heads were ‘kings’, operating their own franchises, their own IT systems, their own processes for account and credit-card handling, their own internet and digital channels,” says Gulliver, “to a group of four truly global businesses, each consistently overseen and properly controlled from the centre, with far fewer systems, much greater economies of scale and each implementing global standards for financial crime risk management.”

This is no longer the same institution a large number of career HSBC bankers had sought to make their way in. “There was considerable internal resistance to that change,” Gulliver agrees. “But what I have tried to do with the 18-person group managing board that reports to me, is not so much disempower the countries, as to empower the global businesses and the global functions, such as risk, operations and technology, legal, financial crime compliance and so on.”

The HSBC Holding company at the top of the group structure used to sit above this diffuse portfolio of banking franchises like a passive investor, with just a handful of staff in the central legal and financing departments, rather than a fully engaged command centre exercising strategic and operational control.

“The chief financial officer of The HongKong and Shanghai Banking Corporation Limited did not, in reality, report to the chief financial officer of HSBC Holdings,” says Gulliver. “He used to report to the chairman of The HongKong and Shanghai Banking Corporation Limited and periodically submit financial information as necessary to the bank’s 100% shareholder.”

It was a structure born in the bank’s early decades – when a smart chap might be sent to run the bank in Malaysia, receiving letters from head office every three or four months by packet steamer. It was like something out of Joseph Conrad. And it had survived too long.

Today, the group leadership team is much expanded, with 80% of group general managers being new appointments since 2011.

Gulliver’s aim has been to keep his direct reports – four business, five regional and then the function heads – focused together on a shared mission of transforming the bank. They all know what each other gets paid. It is in a fairly tight range; the only outlier being the head of global banking and markets, reflecting the different pay levels of that particular business.

If the country heads do not report directly to the group CEO, they each report to a regional head who does report to Gulliver.

Samir Assaf, chief executive of global banking and markets at HSBC, says: “It’s important to recognize that the country heads still have a very important role. Their job is not only to ensure compliance with global standards on financial crime and to work with local regulators, but absolutely to execute also the whole strategy by building relationships with companies. “You need business people as country heads, and today it is likely that the country head will come from one of the global businesses, either GBM or CMB.”

Travelling Gulliver

|

Gulliver joined the bank in 1980 as a member of its famous group of international officers, ready to go anywhere in the world and take on any job at short notice, often living in bachelor messes where they developed a keen esprit de corps.

He worked his way up in treasury and capital markets in Tokyo and London, with stints in the Middle East and Malaysia, before rising to run the Asian and treasury capital markets desks from Hong Kong in the mid 1990s. It was an extraordinarily happy time. “It was such fun that I almost ran into work every morning,” Gulliver recalls.

The bank kept throwing more businesses at him to run – including bonds and equities – and for the first time it dawned on him that he might one day rise to the very top. “I imagined that running the whole firm would be just like this, only much bigger and so presumably even more fun.

“It turned out slightly differently,” Gulliver admits.

He at least came into the top job equipped with a full understanding of the bank.

Working in treasury made him familiar with the underlying flows derived from a commercial bank handling cash for customers, the foreign exchange needs thrown off by their trade payments and receivables, as well as with managing the bank’s own mismatch between surplus deposits and delayed redeployment into funded loan assets.

He did not grow up understanding how to create the impression of scarcity in an equity capital markets deal, but rather steeped in short-term money market interest rates and currency movements.

While long-serving CEO William Purves was a remote figure, whom Gulliver hugely respects but with whom he had little contact, he learned in the dealing room at the feet of John Gray, the man who wrote the book on balance-sheet management at HSBC, on conservation of liquidity and managing deposits always ahead of loans and who played a key role in the currency board that pegged the Hong Kong dollar.

Euromoney first came to know Gulliver in the 1990s in Hong Kong when reporting on the Asian crisis. In the first frantic weeks after the devaluation of the Thai baht, as markets sank into dysfunction and the much-heralded Asian miracle appeared to implode, Gulliver traded the bank’s and customers’ risk positions through stress that no one had seen before.

On Friday evenings in those hectic weeks, traders would often gather to swap war stories in the tiny Captain’s Bar at the Mandarin Oriental hotel. Gulliver always showed, stood with his schooner, usually with an ironic smile and a pithy joke. He nodded sympathetically as Euromoney rehearsed the end-of-the-world anguish of the bankers we had interviewed that week. “That’s right,” he assured us, “we’re all going to be much better people for having lived through this.”

What he was there to do, of course, was not to console Euromoney but rather to send an important message to the markets. This may be tough and unpleasant, but while the chief trader of HSBC, a more important institution than the Hong Kong Monetary Authority itself, can still come for a beer, it is not the end of the world.

The smart sources were already tipping Gulliver back then to head the whole bank one day, calling him one of the smartest bankers of his generation. It was in the years up to this point that he had first conceived the same ambition. Sadly however, decisions above him were now being taken that would mean his time at the top would be devoted to clearing up.

Gulliver soon gained experience and insight into running a global business, as head of markets for the whole group in the first years after the Asian crisis, later as sole head of global and banking markets after his higher-ups had insisted on the toe-curling experiment of him co-heading the division with ex-Morgan Stanley investment banker John Studzinski, who was brought in amid huge fanfare to build an M&A business… and who soon left.

It was that time in charge of running HSBC’s then only truly global business that made Gulliver the insider outsider.

|

| Stuart Gulliver |

Now in London as the sub-prime crisis broke, his team was able to re-run the entire playbook that had kept HSBC safe during the Asian crisis – get very liquid, very quickly; pull in lines; be vigilant of anyone trying suddenly to fully draw down half-forgotten commitments in obscure geographies or businesses. A battle-tested team kept it safe, despite the losses at Household, the dithering of the Bank of England and HSBC’s own unwise steps into conduits and structured investment vehicles, which it could at least preserve and fund on balance sheet when some other banks cut theirs loose after the asset-backed commercial paper market froze. As CEO, Gulliver arrived determined to move the whole bank away from the franchise model with the country head as king as soon as he could. “Internally, we had a reputation for being very strict on cost control,” he recalls, “and yet we had a very high cost base.” Gulliver used to joke in investor presentations about the limits of expense savings that could be achieved from further restricting the number of shirts and socks HSBC bankers could put through the hotel laundry on business trips.

It went down well with HSBC bankers, though probably over the heads of some more earnest buy-side analysts wondering if this laundry thing was an accrual item they should somehow integrate into their earnings models.

“It is only now, running businesses as single global verticals, that you can negotiate your procurement in ways that derive full economies of scale,” Gulliver says. “We used to have countless separate contracts with IT companies, with the people managing our properties, with every supplier in fact.”

It was not just inefficient though. Costs ran out of control because the industrial logic had been lost.

Meetings with institutional investors were, he recalls, not easy at first. “You needed to book about two days to explain the bank,” Gulliver says, “because it had become a higgledy-piggledy collection of businesses. I would be saying: ‘Well in Argentina we do a lot of car loans and also lend to very large companies. Then in the US, we make a lot of sub-prime loans to people.’ And investors would be asking: ‘What are the common themes? Where are the systems synergies? Where are the risk synergies? What is the logic? You could see them thinking: ‘No wonder this thing trades at a conglomerate discount.’”

John Bond, as group chairman from 1998 when Purves finally retired, and Stephen Green, as CEO, along with the board of HSBC, decided in the wake of the Asian financial crisis that this famously emerging-market focused bank, which had always run itself conservatively on the basis that in many of the Asian countries where it operated no sovereign or central bank would be big enough to bail it out if it got into trouble, needed more exposure to developed markets and a more balanced exposure to emerging markets.

It sought to reduce its dependence on Asia, its traditional home. This probably seemed like a shrewd continuation of the strategy to hedge against the handover of Hong Kong to China in 1997 by buying Midland Bank in the UK in 1992 and making London its global headquarters.

HSBC became an acquisition machine, hoovering up banks like Credit Commercial de France, Republic National Bank of New York. And most notoriously of all, Household International, justifying the latter on the eye-raising grounds that the sub-prime lender brought it both welcome exposure to the US, as well as invaluable expertise in lending to residents of US trailer parks that the bank could deploy in Asia and the Middle East – where it in fact banked the ruling families of the Middle East and Hong Kong’s tycoons.

This was a big mistake. It was the earnings warning from Household at the end of 2006 that signalled the start of a far larger panic than the Asian financial crisis, the sub-prime debacle that cost HSBC shareholders heavily, led to the launch of a £12.5 billion ($15.8 billion) rights issue in 2009, and that it might have avoided.

In the years after the Asian crisis, HSBC grew from a bank with 136,000 staff and a $472 billion balance sheet, to close to 330,000 staff and a $2.4 trillion balance sheet by the time the sub-prime crisis hit. Even now, just looking at those figures, thinking of a conservatively run bank growing its balance sheet five times over in a decade requires a double take.

There are a few examples of good buys, of course: CCF for one, which gives it a banking entity in France and now a hedge against a post-Brexit loss of passporting for UK-based bankers selling to European clients. Ping An proved to be a smart financial investment. HSBC did almost no business with it and Gulliver sold it off during the so-called ‘six-filter review’ of the business portfolio because it had no strategic connection to the rest of the group. But at least that crystallized substantial value.

However, many of these now look like the wrong acquisitions made at the wrong time and for the wrong price. Worse than that, and unlike the better US bank consolidators rolling up regional banks across the country in the 1990s, such as Banc One, HSBC simply did not have the people, the bed-rock systems or the know-how even to attempt post-acquisition integration.

The world’s local bank – a marketing slogan that Gulliver swiftly dispatched – had become, in fact, a good description of where HSBC had gone wrong.

|

Good company

Gulliver can be very entertaining company. He talks through the de-layering of management at HSBC with a sardonic smile forever tugging at the edge of his mouth. The plan, he says, was that “there should never be more than eight layers of management between me and the most junior revenue producer, and each manager should have at least eight people reporting to them.”

What he found was “there were places where the bank had grown to 17 layers of management. There were managers who had no one reporting to them. And there were managers that basically reported to themselves.”

He pauses to let that one sink in. “Their appraisals were always fantastic.”

It has not all been jolly though. It has often been more like trench warfare.

Fixing a bank is less fun than addressing its strategic challenges – or at least diverting attention away from them – with a supposedly visionary M&A deal or even a break up.

Gulliver’s task has been to transform the running of HSBC while staff at the coal face keep doing a good job for clients, to convince shareholders that there was more value to be had in getting the network to work together than in breaking it up, and to assure regulators that it was not too complex to be managed.

For much of his time as chief executive, a sword of Damocles has hung over him in the DPA with the US Department of Justice, after the $1.9 billion fine at the end of 2012 to settle the laundering of money for Mexican drug dealers and for dealing with other sanctioned entities.

If it were ever to lose its licences to clear dollars as a US bank, that would be game over for HSBC in its current form. Everybody who works there knows that, not least the chief executive, who also knows that the very global network that is its defining differentiator puts HSBC at risk. It needs to operate in a permanent state of heightened alert.

A terrorist looking to move money from the Middle East, say, to fund an outrage in the US or Europe, is more likely to use a global bank to do it than the local community bank or building society in the target country.

This is where the joke about managers writing their own appraisals stops being funny. Its experiences in Mexico show how HSBC’s old structure allowed employees who did not share its governing principles of, for want of a better phrase, British decency, to avoid detection or oversight. Such bad actors tend not to self-report.

“The deferred prosecution agreement hugely hurt the self-esteem of every single person at HSBC,” says Gulliver. “People became almost embarrassed to be associated with the bank, and our staff were ashamed, in particular when asked by their families about the organization they worked for.

“By the time the results of the US Senate Permanent Subcommittee on Investigations were reported, we had already exited a number of high-risk countries. We have striven relentlessly to instil new global standards for fighting financial crime. Although we absolutely deserved it, working with a monitor has been tough and made customer acquisition difficult. People are extremely concerned about doing anything that might raise even the slightest risk of breaching the DPA.

“The good news,” Gulliver says, “is that by better serving our existing clients, we now have the chance to transfer rising revenues direct to the bottom line at limited additional cost.”

There is no point feeling sorry for yourself. The buying spree HSBC went on after 1998, to pivot away from Asia and increase exposure to developed markets, had taken it from employing 136,000 people in 1998 to 330,000 in 2007. It had already diluted its famous culture.

The three key challenges – to get a grip on financial crime risk, to improve returns for shareholders and to demonstrate to regulators that HSBC is not too big or too complex to manage – all pointed HSBC in the same direction. The deferred prosecution agreement just added urgency.

Six filter strategy

|

| Andy Maguire |

Some investors have criticized HSBC for not pressing home its advantage in having a good financial crisis by picking up stricken rivals on the cheap and expanding market share. It still lacks scale in the biggest investment banking and capital markets fee pool of all: the US. Did it miss the chance to buy, say, Morgan Stanley?

The truth is that HSBC was already struggling to cope with a litany of purchases it made in the years before the crisis.

In the run-up to becoming chief executive, Gulliver had urged a more systematic approach to assessing the strategic fit of new acquisitions to the existing HSBC portfolio. Applied to the putative acquisition of Nedbank in South Africa from Old Mutual, this led HSBC to walk away from that deal in 2010. Refined into the so-called ‘six filters’, it then backstopped the 97 disposals and country exits Gulliver has overseen since 2011, a process now mostly complete.

Management still had to deliver on the notion first sketched out by Gulliver’s predecessor as chief executive, Geoghegan, to join up the group into one HSBC.

“The first thing we had to do was switch to running global businesses,” says Gulliver. “Then we said: ‘This group now processes credit cards in three ways, not 300. And sorry, no you can’t customize that for your country.’ Then we lifted that processing into the lowest-cost place to do it.”

Gulliver appointed Andy Maguire, a former Lloyds banker and managing partner at Boston Consulting, as chief operating officer of HSBC in 2014 to take charge of operations and IT.

“I was giving so much business to Andy’s team at Boston Consulting that I decided it made more sense just to hire him,” Gulliver says. “With common processes set around the globe, operations and IT have been the biggest single source of cost savings. Andy has done a fantastic job, and one which regulators, who had previously struggled to attach precise responsibilities to executives within HSBC, have also appreciated.”

It does not do, however, to declare victory either on IT or the linked issue of financial crime standards.

|

| Douglas Flint |

“For all industries providing critical public infrastructure as banks do, the nightmare is that systems fail and deny customer access or even worse become corrupted and have amounts extracted,” says Flint. “We are doing everything we can conceive of to ensure our systems are strong and that we can respond robustly if there is a problem. The conundrum for the whole banking industry, however, is that when systems were much more siloed, in the days before they were designed for greater customer interaction, they were probably more robust and secure than now when customers want to transact at the touch of a smartphone screen. “That is why HSBC set up a tech advisory board this year to advise us on whether we are on the right track, how we benchmark against our industry and what technology challenges may be looming in the years ahead.”

Similarly, imposing effective group-wide financial crime standards is a never-ending task.

“You can’t just put a ribbon round the box and say: ‘Job done. As long as we carry on doing this, we will be safe,’” says Flint. “Bad actors will seek new ways to disguise payments, and while our ability to analyze large quantities of data, search for suspicious patterns and go out and identify wrong-doing is now much greater, we can only search our own data. Bad actors will often break up transactions across multiple parties and jurisdictions. The banking industry needs unique digital identifiers for everyone engaging with banks; a mandatory, comprehensive and robust register of beneficial ownership that is open to scrutiny; a way to share public and private data; then a way to apply to all this human intelligence that understands how bad actors think.

“Individual banks and the entire system still have much work to do.”

Don’t turn deposits away

Some questions continue to dog senior management, and probably will do so for Gulliver and Flint’s successors. For example, should HSBC deploy that excess of deposit funding more aggressively into higher-risk assets through the period of low loan growth and suppressed rates, or wait for normalization in the term value of money to boost returns?

“People have criticized us for keeping advances too low and deposits too high,” says Gulliver. “When we could only park them in the UK for zero at the Bank of England and so set deposits rates at zero, customers still gave us more because they saw that as an indication of strength. But I won’t turn deposits away. I don’t ever want to tell customers: ‘We don’t want your money this week: come back next week, we might want it then.’”

And having fought to survive the Asian crisis and the sub-prime crisis, the bank’s top management is in no mood to listen to outsiders urging a relaxation of underwriting standards. Its loan impairment charges have stayed low, at around 0.4% of total loans last year, against 1.2% on average for peer global banks.

It has recently begun to grow loan volumes modestly, notably in commercial banking in Hong Kong and the UK. But more than any other large bank Euromoney can think of, HSBC is geared to benefit if rates continue to rise in the US, as the Fed suggests, and to pick up in response to robust European growth.

While HSBC still lives in the shadow of the DPA, bank regulators are now sufficiently comfortable with HSBC’s exposure to operational, credit and market risk to allow it to return capital to shareholders.

Last year marked HSBC’s first share buy-back since its foundation in 1865. The stock price had sunk as low as £4.30 in mid 2016, with short-sellers converging amid continuing concerns about a hard landing in China after the currency and stock market falls of 2015 and worries over sustainability of the dividend.

Today, the share price stands at £6.88, with the stock trading roughly at book value, indeed at a premium of 1.2 times tangible book value per share.

Taking a 10-year view of the volatility of pre-tax profit, investors see stability at HSBC, with a range of 0.9 times, compared to 3.6 times on average across a group of global peers including Citi, JPMorgan, Standard Chartered, BNP Paribas, Deutsche Bank and Santander.

The bank reported weak numbers for the whole of 2016, after taking accounting hits for writing off goodwill on the private banking operations of Republic National Bank it acquired back in 1999, on currency translation effects from selling its Brazilian retail businesses to Bradesco and on adjustments to the value of its own debt as HSBC’s credit spreads improved. But these are the necessary continuing costs that obscure the culmination of a hugely impressive restructuring.

Beneath the headline numbers, good things are happening.

Take, for example, the global banking and markets division, essentially the corporate and investment bank of HSBC. Investment banking earnings across the industry are notoriously volatile and, as such, rightly valued at a discount by investors. But 70% of HSBC’s GBM revenues are derived from managing clients’ global liquidity and cash management, from financing their trade and receivables, and from FX: all businesses in which it ranks in the top three in the world. This transaction banking revenue has been very stable, even while the 30% derived from event businesses, like M&A and equity capital markets, as well as from trading in equities, credit and rates, has fluctuated.

HSBC bankers have learned to cross sell. Two thirds of GBM clients use it for more than four products; one quarter use it for six or more, which has a big multiplier effect on revenues. And the number of GBM clients in this category has shown a compound annual growth rate of 8% since 2014, while the number using it for just one has fallen at -6% compound.

There is also a bit of a moat around this business. Half of GBM’s revenues come from clients that deal with it in four or more regions of the world. Having quit countries that do not trade much, that operate closed economies or raise concerns about financial crime risk, HSBC’s slightly shrunken network across Asia, Europe, Middle East and Africa, North America and Latin America still covers 90% of world trade and capital flows.

Only Citi competes at this breadth; maybe BNP Paribas; JPMorgan and Bank of America, not so much. That is a big chunk of revenues simply not available for most of the world’s other big banks.

Gulliver’s restructuring efforts have been focused on preserving this network, the bank’s historic legacy as the trade financier of the British empire, what insiders sometimes refer to in shorthand as “1865 and all that”.

Resisting calls to break up what had begun to look like an unmanageable conglomerate was vital. Gulliver has fought to reset investor expectations for HSBC to emphasize the value of the network coming through most obviously in market share gains, profits and returns in CMB and GBM, and to imply that any break up now would likely come at a discount rather than a premium.

There is much work still to do. HSBC confirmed a 10% return on equity target back in 2015, modelled on a CET1 ratio of 12% to 13%. That is a return that the group has not met, while running a CET1 of 14.3% with no clarity yet on final regulatory requirements for the size and composition of the capital stack.

The bank will not reach the 2017 profitability target for the US laid out in 2015, but has made progress there and in Mexico. And it is ahead of most of the big 2015 promises on risk-weighted assets and cost reduction, looking set to leave 2017 with the same cost base as 2014, on a more logical and connected portfolio of businesses, even after investing heavily in financial crime standards and the digital transformation of the group.

That share buyback shows the bank using every lever at its disposal on capital management. Supposedly trapped capital in the US has started to dividend its way back to the holding company.

The stock is now a core component of the income portfolios of many active real money managers as well as of the trackers.

Time to go

Gulliver will leave HSBC some time in 2018: early in the year, presumably, if the incoming chairman from AIA, Mark Tucker, and the board appoint an internal candidate to succeed him; later in the year if the next chief executive comes from outside HSBC.

It is Gulliver’s choice to leave, following Flint who departs as chairman at the end of September this year.

As a board director of HSBC, Gulliver will have some limited say in the succession process. He refuses point blank to be drawn on whether it should be an external or internal candidate, but he will be taking a close interest. Much of his wealth will be tied up in HSBC stock for up to seven years after his time at the top is over.

“It’s entirely appropriate that stock compensation should be structured only to pay out years after senior executives leave because this aligns senior executives’ compensation to the long-term success of the companies they run,” he says.

Recent experience at HSBC and many other banks shows bad actions can remain hidden for a very long time before they, and their consequences, finally emerge.

So, to the final question, which has to be: with the bank in good shape, why leave now? Gulliver will, after all, only be 59 in 2018.

“I want to work until I am 75 to 80, because I think the best way to stay healthy is to stay busy, and I would like to find what next by the time I am 60,” says Gulliver. “It will certainly be in financial services, probably working across Asia, the Middle East and maybe Europe where my contacts are best. But I can’t see myself working at another large, publicly listed bank having already done that here. It will probably be something that involves private capital.”

Hanging around does not make sense to Gulliver. “I can hardly run HSBC for 28 years. I told the board when I was appointed CEO that I saw it as a five- to eight-year job, and it will be seven years at the start of 2018.

“When you look around the banking industry and consider its history, there are examples of chief executives who remained in situ far too long, after all the potential replacements among their own generation had left and they became rather isolated, semi-deified figures, with people 10 to 15 years younger reporting to them that want the top job but don’t dare to challenge the incumbent on any decision.

“There is a danger that unchallenged leadership becomes narcissistic. And that’s when bad decisions get made. I have tried to surround myself with the smartest people I can find. There’s an element of rough and tumble on the group management board. People certainly challenge me.”

Euromoney might argue that that sense of stewardship is more likely to be keenly felt among the internal candidates to replace Gulliver. But it is no call of anyone but the board.

And perhaps even more important than picking the right individual is making sure the next person in the chief executive’s office does not try to make a mark by squandering this transformation on ambitious, ill-judged and capital destructive acquisitions.