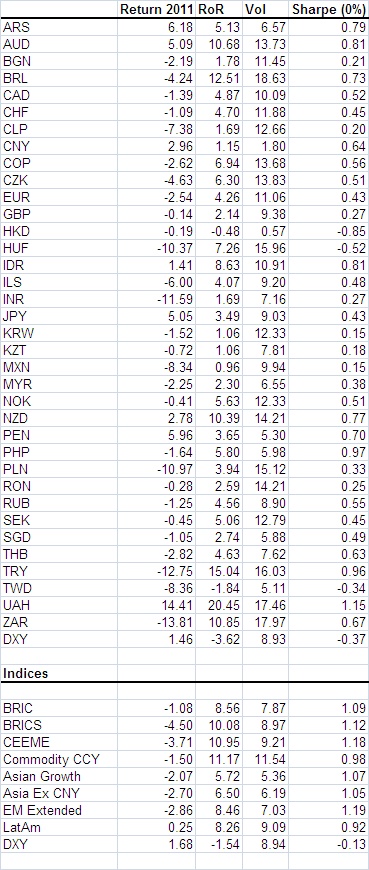

The passive, fully funded currency indexes provided to EuromoneyFXNews show the LatAm index was the only one to produce a positive return, 0.25%, at a time when investors have sought safe havens amid the European sovereign debt crisis and fears of a global double dip recession. Indeed, the IntercontinentalExchange’s DXY dollar index was the best performer, finishing the year with a return of 1.68%.

The Bric Index, which includes the South African rand, was the worst performer, delivering a negative return of -4.50% for the year, closely followed by the Central Eastern European and Middle Eastern currency index with -3.71%. Meanwhile, the Commodity Currencies Index generated -1.5% in returns.

September represented the biggest losing month, where the dollar rose against a broad basket of emerging market currencies by about 10%, as investors fled the emerging markets, and sought safe haven currencies.

The Swiss National Bank was forced to intervene in the currency markets to protect its economy from its overvalued currency. Excluding September, the Bric Index was the best performer, with a positive return of 6.46%, followed by the Commodity Currencies Index, with a return of 7.71%.

In terms of single currencies, ZAR, TRY, INR, PLN and HUF were the worst performers, with the South African rand the worst performer with a -13.81 return. Meanwhile, the Ukraine hryvnia (UAH) and the Argentine peso were the best performers, returning 14.4% and 6.18% respectively.

EM currency indexes continue to outperform emerging market equities on a reward-to-volatility basis. The average Sharpe ratio, which measures excess return per unit of deviation, for the EM currency indexes was 1.08, double the average for MSCI EM World, Asia and DJIA equity indexes during the same period.

|

Currency returns 2011 |

|