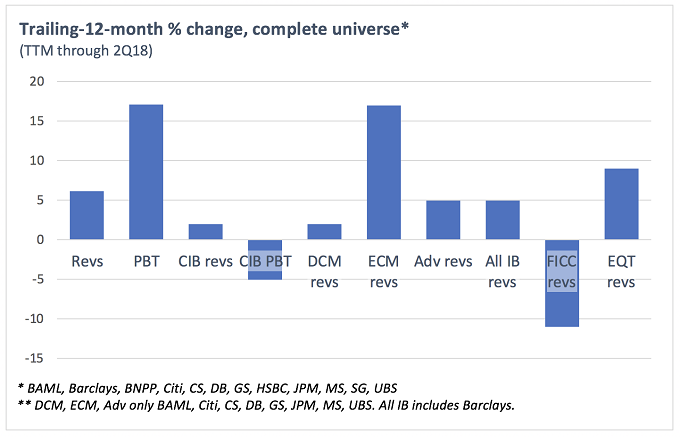

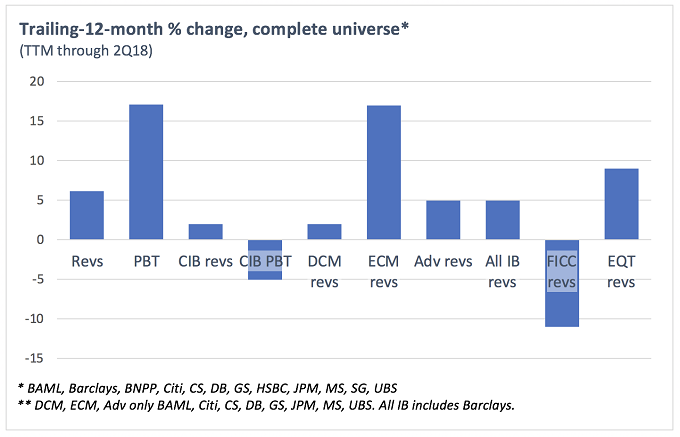

First, a graph. There will be lots of these.

In summary, PBT growth driven by lower costs more than by higher revenues, those costs proving harder to cut in CIB divisions than elsewhere, DCM sort of flat, advisory up a bit, ECM looking great, FICC having a shocker and equities building nicely.

Now for the breakdown – and the usual disclaimers. Numbers are unadjusted wherever possible. Banks’ percentage change figures reflect reporting currency; aggregate changes reflect US dollars.

Access intelligence that drives action

To unlock this research, enter your email to log in or enquire about access