A research report put out by Credit Suisse yesterday takes another look at the increasing Target2 liabilities – the payment system used by eurozone central banks – of the Spanish and Italian central banks, throwing into sharp relief the high levels of capital flight in these economies.

First, here’s a refresher of what the eurozone accounting malarkey known as Target2 is correlated with:

|

““Rising TARGET2 liabilities are indicative of: |

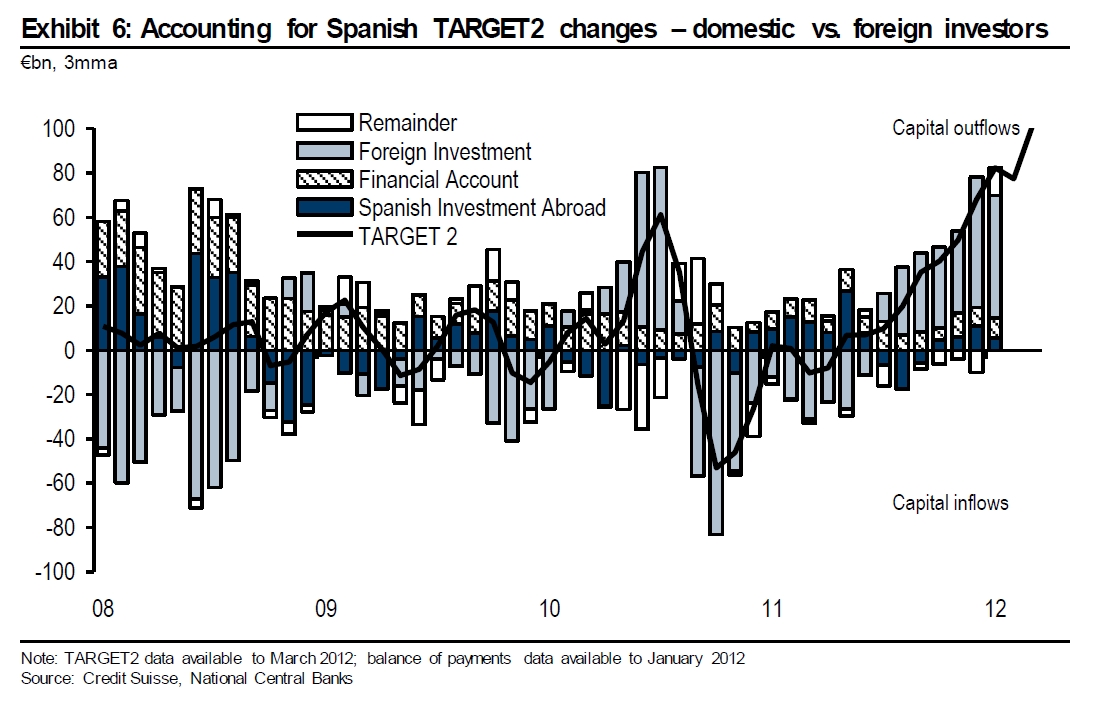

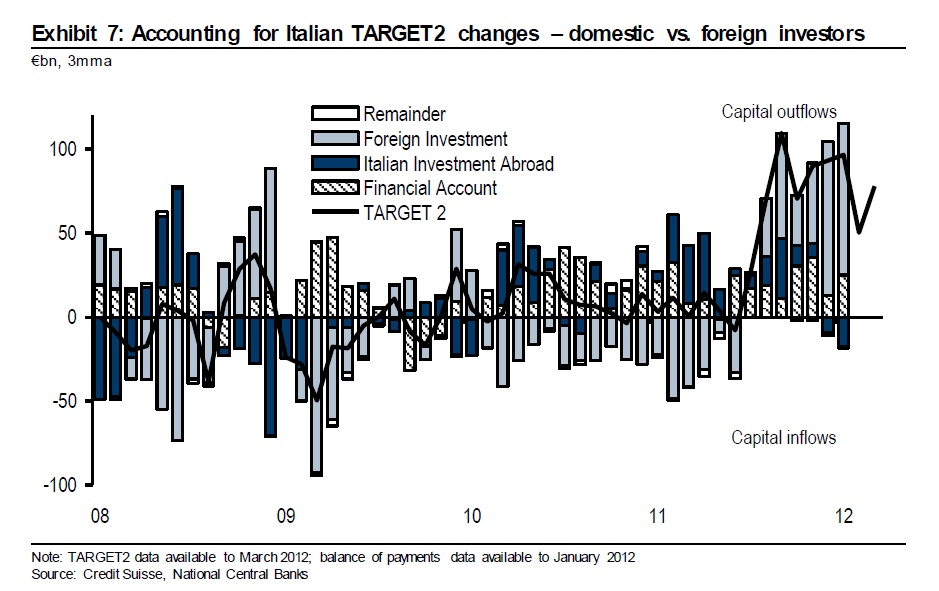

This chart shows a pretty clear correlation between Target2 liabilities and capital outflows:

Almost all of the outflows are due to foreign investors withdrawing funds rather than domestic investors channeling funds out, according to Credit Suisse. While this means that financial repression could be effective in buttressing domestic government bond markets in Italy and Spain, it also means that in a worst-case scenario deleveraging could become much larger.

Still, today’s eurozone bank lending survey from the European Central Bank (ECB) provides some quantum of solace: a net 7% of participating banks reckon demand for loan will rise in the second quarter of the year.