The 2025 Euromoney Cash Management Survey reached 30,000 corporate treasurers across 123 countries. Between April and June 2025, corporates assessed 486 cash management providers, shared their current priorities and outlook.

Euromoney Cash Management Survey is the most comprehensive benchmarking exercise of the world’s corporate banks, offering authoritative insight into the needs of corporate treasurers and their perceptions of the banks they work with.

The use, distribution or publication of MarketMaps or rankings requires the express permission of Euromoney – please contact Arun Ghudial for additional information. For any queries on methodology, data packages or bespoke benchmarking reports – please contact Ana Voicila.

Top ranked cash management providers for corporates

HSBC retains the top global position in cash management, recognised by corporates for its combination of scale, reach and service responsiveness. Its HSBCnet platform and global-local delivery model make it a preferred partner for corporates managing complex cross-border flows. Standard Chartered is strengthening its role as one of the main trade finance providers and its position in emerging markets, through platform innovation and FX solutions. J.P. Morgan is recognised for technology, automation and its large balance sheet, while Societe Generale, Deutsche Bank and Bank of America all stand out for service quality, system integration and digital platforms. Credit Agricole CIB, Santander, BNP Paribas and BBVA combine strong regional reach with product breadth and competitive pricing, ensuring corporates value them for both domestic and international liquidity needs.

Rankings across large corporates and middle market

Africa’s treasury landscape is marked by sharp contrasts: high inflation, chronic FX shortages and the rapid spread of mobile money. For corporates, this means costly local borrowing, volatile currencies and the need for careful liquidity planning. Citi leads the rankings as the top choice of corporates, combining exceptional client service with advanced technology. Standard Chartered is highly valued for international connectivity, while Standard Bank stands out for local presence, product strength and top-rated client service. Access, Absa and Ecobank also feature prominently, reflecting regional reach and digital innovation, while Société Générale, BNP Paribas and Attijariwafa dominate in francophone markets.

Treasurers face persistent challenges. Inflation and currency depreciation force corporates to rethink their liquidity strategy. East Africa showcases digital leapfrogging through mobile money integration and expanding instant payments. Initiatives like PAPSS are reshaping cross-border flows, promising lower reliance on dollars. The outlook is cautiously improving, but treasurers remain focused on FX access, liquidity buffers and working capital discipline.

National and territorial rankings

To see all rankings, please navigate across the pages of the table.

Asia-Pacific’s treasury landscape reflects divergent monetary cycles, rapid digitisation and rising RMB internationalisation. China’s easing policy and property-sector headwinds push corporates to focus on liquidity preservation, while Japan’s rate hikes reshape cash strategies amid a weak yen. India benefits from growth and UPI’s transformation of payments, while Southeast Asia drives instant payment interoperability through ASEAN linkages.

Regional leaders include DBS, HSBC, J.P. Morgan and Bank of America, all positioned at the forefront of API, real-time and mobile-first cash management. HSBC is recognised at regional level as #1 choice for Client Service, while DBS leads from a Product & Technology perspective. Domestic banks such as ICBC, Bank of China and Japan’s megabanks remain critical for local liquidity. The region’s outlook is cautiously optimistic, with India and ASEAN driving growth, China as the swing factor, and treasurers maintaining precautionary buffers amid FX volatility.

National and territorial rankings

To see all rankings, please navigate across the pages of the table.

Europe’s treasury environment in 2025 is shaped by regulatory transformation, particularly the EU Instant Payments Regulation mandating universal SEPA instant payments. Treasurers gain efficiency but face challenges around intraday liquidity and 24/7 cycles. Open banking, digital euro pilots and CSRD sustainability reporting add to the structural shifts.

ING leads the rankings, noted for pan-European innovation and service. Citi is recognised by the corporates as #1 provider in the region for products. Deutsche Bank, HSBC and BNP Paribas provide global integration with regional depth, while UniCredit, Raiffeisen and local champions such as Santander, Intesa and Erste are essential in their home markets.

National and territorial rankings

To see all rankings, please navigate across the pages of the table.

Latin America’s treasury landscape is a story of contrasts. Brazil offers stability with easing rates and Pix revolutionising real-time collections and payments, while Argentina grapples with hyperinflation and capital controls, forcing corporates into survivalist cash practices. Mexico, Chile, Colombia and Peru lie between these extremes, combining stabilisation with digital transformation.

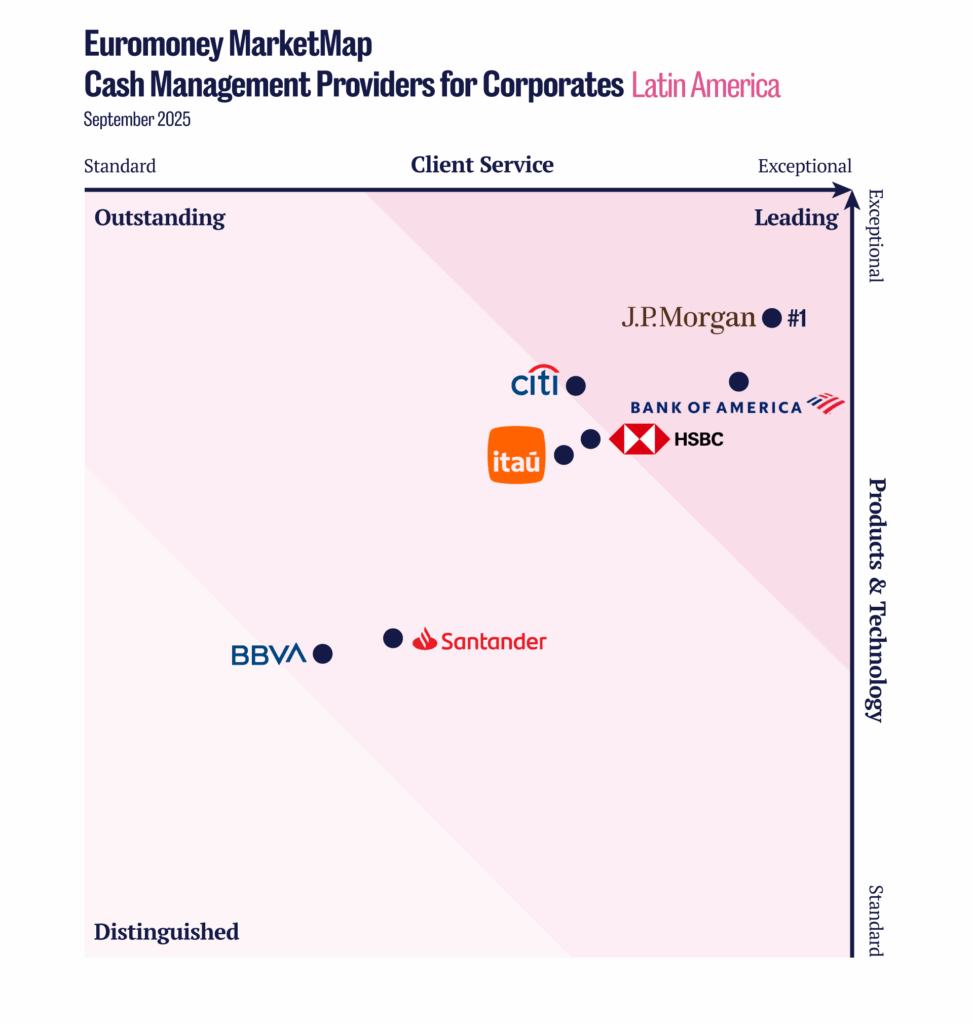

J.P. Morgan leads regional rankings, valued for product breadth and integration. Bank of America, HSBC and Citi are strong for multinationals, while Itaú commands deep loyalty in Brazil, leveraging Pix innovation, APIs and client-centric design. Santander and BBVA extend their Iberian strengths into Spanish- and Portuguese-speaking markets. With easing cycles expected, treasurers will continue balancing defensive liquidity strategies with opportunities in instant payments and fintech partnerships.

National and territorial rankings

To see all rankings, please navigate across the pages of the table.

Mashreq leads the region with technology-driven platforms and responsive service, while HSBC and Citi remain trusted global partners integrating GCC cash flows with international structures. Emirates NBD and Standard Chartered bridge international networks with strong local coverage, and FAB, ADIB, Arab Bank and Ahli United Bank provide relationship-driven liquidity solutions.

Payments innovation is accelerating through Saudi Arabia’s sarie, the UAE’s IPP and regional RTGS integration. Looking ahead, a potential GCC digital currency could transform cross-border liquidity and settlement efficiency.

National and territorial rankings

To see all rankings, please navigate across the pages of the table.

Note: The North America sample is primarily composed of respondents based in the United States.

North American treasuries balance the impact of high funding costs, the legacy of the 2023 regional banking crisis, and new opportunities from instant payments. Deposit diversification into MMFs increased, while FedNow and RTP adoption offer just-in-time settlement and faster receivables, though reconciliation challenges remain.

Deutsche Bank ranks #1 in corporates’ preferences, recognised for its Product offering in the region and Client Service. J.P. Morgan leads in Technology, while Bank of America’s CashPro platform and Citi’s global network are widely valued. HSBC, a leading provider, is recognised by corporates as a strong cross-border partners. BNP Paribas brings its European perspective to U.S.-based treasurers, while Canadian players complete the top ranking. The region’s treasury outlook is one of adaptation: embracing instant payments, maintaining diversification and navigating a higher-rate world.

Liquidity in focus: adapting to a 24/7 treasury

Treasurers worldwide are reinventing liquidity.

Euromoney’s 2025 Cash Management Survey reveals how corporates adapt to real-time payments, tighter money and digital transformation, highlighting shifting priorities, sector insights and the banks setting new benchmarks for excellence in liquidity management.

55% respondents are expecting increase in their cash management flows in the next 12-18 months, with liquidity solutions being the prime beneficiary.