“The record keeping and reporting was done on an old Univac – a tape and drum system – and down the hallway in our office on Park Avenue in a 40×40 room was a huge mainframe computer that had to be kept at 45 degrees to keep it cool,” reminisces Robert Elliott, who joined Bessemer Trust in 1975, working there until 2011.

“The cost was probably 15% to 20% of our budget. Now of course you can do three times what that computer could do on an iPad.”

Advances in technology have helped the wealth management industry become more efficient; now it reaches larger numbers of clients, who can be onboarded and shown their portfolio performance on (indeed) an iPad.

That evolution, it seemed, was leading us to a wealth management landscape that would be operating entirely online. But, almost a decade after the first robo-advisers emerged, was the early enthusiasm misplaced – can human interaction ever be replaced by robots and, indeed, do clients want that to happen?

In the case of linear upward-moving markets, maybe people are OK to just check their portfolios online, but when there is volatility, then everything changes – Alessandro Foti, FinecoBank

When robo-advisers began, it was largely assumed they would target retail and mass-affluent clients with simple investment needs, filling an obvious gap. It had been far too costly a proposition to offer human advisers for people with $1 million and below, but now technology allowed fintech firms, such as Moneyfarm, Vaamo, Nutmeg, Wealthfront and Betterment, to reach the masses, charging 25 basis points for digital investment portfolios determined by online profiles.

It was expected the audience would be chiefly millennials, who were more accustomed to using digital devices to conduct business. The emergence of robo-advisers was seen as a threat, therefore, only to retail banks’ mass-affluent businesses and to online banks rather than wealth managers. Those with more than $5 million in assets would still require a more high-touch service.

However, over the last few years it has become clear that the business could not be divided so easily into black and white.

Joe Ziemer, vice-president of communications and policy at Betterment, says his firm has many clients with more than $10 million in assets. It also has customers who open an account with just $50, making its average account size about $40,000 (up from $12,000 when it first started in 2010).

Another surprise has been the age range of customers. More than a third of Betterment’s customers are aged 50 and above – some are in their 90s.

Joe Ziemer, vice-president of communications and policy at Betterment

“I don’t think older generations get enough credit for their use of technology,” says Ziemer, who points out that his 88-year-old grandmother uses an iPad.

But perhaps the biggest surprise for robo-advisers – and the banks that tried to emulate them with their own platforms – was that while their customers clearly were opting for a digital investment platform, they also wanted human interaction.

This discovery led Betterment to introduce a tiered level of service. For 40bp, customers have unlimited access to a certified financial planner (CFP), who can talk to them about their retirement plans, for example. And, for a one-off $399 cost, newlywed couples can receive advice from a CFP about merging finances.

“Or, if you want to speak with a traditional adviser, we can set you up with one of the advisers who use our platform,” says Ziemer.

Some 500 advisory firms, typically small, with only one or two advisers, use Betterment as a tool for their own clients.

Personal relationship

It is not just Betterment that has gone from a pure digital offering to one that has more humans. Nutmeg in the UK has also started to introduce people.

Wiwi Gutmannsbauer, COO of UBS Asia Pacific, points out that even wealthy fintech clients at his firm want a personal relationship, such is the human need to be able to interact around money.

There is one digital provider that recognized long ago that there would need to be a mix of high-tech and human touch in wealth management – FinecoBank in Italy (and more recently in the UK).

|

|

|

Alessandro Foti CEO of FinecoBank |

The firm started as mix of both human and digital wealth in 2000, one year after it was born in 1999 – indeed, chief executive, Alessandro Foti refers to Fineco as a technology company.

It is the largest European online broker in terms of the number of executed trades. At the end of 2018, it had 1.28 million customers and €69.3 billion in assets. The firm is ranked best in technology in Italy in Euromoney’s Private Banking and Wealth Management survey 2019.

“The real world is multi-channel, and clients use whatever is most appropriate for their needs,” says Foti. “Therefore, why say clients under a certain wealth level behave one way and those above it need more interaction? It’s not as straightforward as that. The secret we knew from the outset was that we would have to have both.”

Fineco’s algorithms build and rebalance portfolios, as well as automatically selecting the best funds and solutions from an open platform, but the firm also has financial planners that manage the needs and goals of clients. Human interaction will never go away, says Foti.

“As an example, in the case of linear upward-moving markets, maybe people are OK to just check their portfolios online, but when there is volatility, then everything changes. It then becomes uncomfortable for a client to be in relationship with a device.”

Victor Matarranz, global chief executive of Santander Private Bank, adds that the speed of information makes that knee-jerk reaction by customers even sharper and that human interaction is necessary. His firm is integrating robo-advisory with adviser interaction.

“We have gone from a world where customers looked once a quarter at their investments when they got the statement in the mail,” he says. “Now they can see on an hourly basis what is happening. A bad market day wouldn’t impact a client back then, but today if you have a bad week, every customer will call you. You need someone there to respond.”

It is something Betterment has thought about, says Ziemer: if markets increase in volatility, can independent robo-advisers without a brand that has withstood former recessions, or that do not have a human element, survive?

Ziemer is confident his firm can – even suggesting that robo-advisory can help quell customer panic in choppy markets, as well as help customers make better long-term decisions about their money.

“We’ve put guard rails in place for times when there is volatility, so that when customers feel nervous about markets and want to withdraw their money, we introduced an alert that tells them about the tax impact of cashing out of investments,” he says.

It is something that few customers understand: that it may be better to stay invested and weather the storm.

Ziemer says when Betterment introduced the alert three years ago, volatility of withdrawals in difficult markets dropped by 65%. He adds that there is a further opportunity to develop technology that takes a proactive route when large corrections in markets occur.

“Instead of advisers having to call their clients in that moment, which is what would happen outside of the robo-advisory model, we could send an alert or advice to every client in just a fraction of the time,” he says.

Costs

This convergence of digital and human seems to be where the wealth management industry is moving, having recognized the power and efficiency of the former but the appetite for the latter. However, costs have to be factored in: can robo-advisers still be profitable with humans in the mix, when they are already struggling to make money?

UBS, for example, tried to run a stand-alone, purely robo-advisory in the UK called Smartwealth that served customers with more than £15,000 in investible assets. After a year, the technology was sold to US robo-adviser, SigFig, in which the bank has a stake.

Gutmannsbauer says robo-advisory cannot be compared to wealth management in terms of average asset size and it is not enough for clients who need to discuss complex issues, but he admits that UBS has an “advanced technology” platform that works for the bank’s client advisers on asset allocation and investment selection, rather than being client facing.

That frees up the client adviser to discuss more complex issues such as legacy planning, personal values on sustainability or responsibility and risk appetite, he says.

“There are limitations to technology that maybe will be looked at over the decade ahead,” he says. “For example, a client may say one thing [in conversation] when they really mean something else. An adviser can sense that, ask the right questions and expand on the conversation. Given they are using a robo-adviser on the portfolio side, it means he or she now has time to have those lengthier, more-nuanced conversations.”

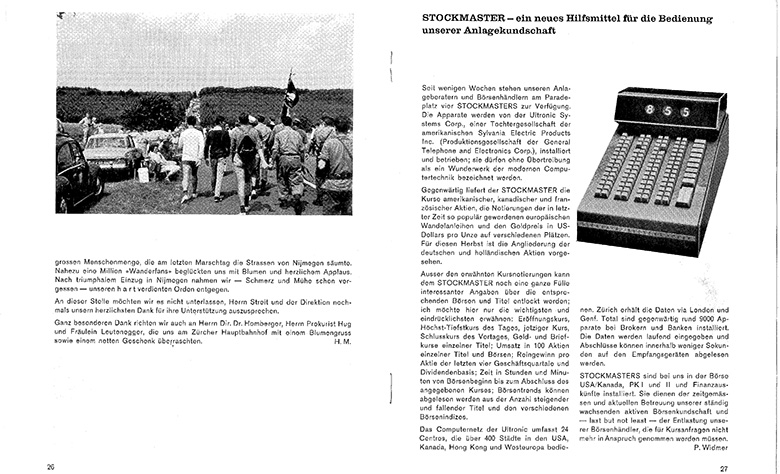

Robert Sinn, designed the first usable stock quotation system, The Stockmaster, in the early 1960s. By 1970 more than 10,000 had been sold in 20 countries on six continents, revolutionizing the entire brokerage industry. Before moving into fintech, he had built a programmable digital computer complex to do the accounting for the US Army principal warehouse depot, and spent 18 months in Tule, Greenland, to help to set up a ballistic missile early warning system

Greater efficiency of advisers is also an outcome.

“The pressure on margins is only going to continue, so wealth managers will need to improve the productivity of advisers,” says Foti. “A robotized offering does that.”

He points to the growth in assets under management per client adviser at Fineco as an example of how efficiency is growing without compromising service.

At Fineco, AuM rose 10% for the first three quarters of 2018, compared with the first three quarters of 2017; assets under its advanced advisory solutions rose 20% year on year. Advisers with more than €20 million of assets now represent 44% of the total, up from 39% in September 2017.

Betterment’s Ziemer says that the emerging model across wealth management businesses is that of the “bionic adviser” or the “tech-driven adviser” – an adviser that can be more productive because of having a robo-adviser platform.

“Client onboarding, know-your-customer, linking up accounts, pulling client deposit data – we can do all that digitally, in addition to optimizing portfolios, and we can also collect the fee on the advisers’ behalf,” he says.

The aim is to make the lives of the adviser simpler, says Foti.

“In the years ahead, the focus will be about how to 100% digitalize the relationship between the adviser and the bank, so that advisers never have to waste time in admin or back-office duties. That means restructuring the processes within the bank and how it is organized internally.”

Gutmannsbauer agrees.

“Getting the whole back-office digitalized is where we need to be headed,” he says.

Client experience

In addition to bringing technology to bear more fully on the back end, there is still plenty of room for innovation around client experience in the coming decade.

|

|

Patrick Odier, senior managing partner at Lombard Odier, which already provides technology back-office platforms to third-party financial institutions, says he expects one challenge for the next decade will be better tailoring information to clients.

“Firms have to know what the pertinent information is and then whether it is suitable for a client,” he says. “And can the adviser have this knowledge before even sitting down with the client? The industry has a long way to go in taking data and applying it more personally.”

Sim S Lim, group head of wealth management and consumer banking at DBS, agrees that tailoring data is going to be the next challenge.

“Fully harnessing technologies like artificial intelligence and big data for data-driven insights, such as predictive analytics, could enable banks to provide personalized, algorithm-driven financial advice,” he says.

Providing clients with greater choice around their portfolio management is also going to become a standard in the years ahead.

Société Générale Private Banking recently launched ‘Synoe’, a digital investment advisory service that allows clients to keep control of their portfolio management around the clock by delivering personalized investment recommendations and live financial market alerts.

Every month, or when there are important market movements, clients receive market information and individualized proposals for the reallocation of their assets.

They can opt to accept the proposals or to discuss them further with an investment adviser before making their decision.

“The human interaction is offered, along with a digital service,” says Jean-François Mazaud, chief executive of Société Générale Private Banking. “The most important thing is that customers have a choice.”

In the battle of humans versus robots, it seems like people will be putting up a good fight for many years to come.